*Solve it by using EXCEL

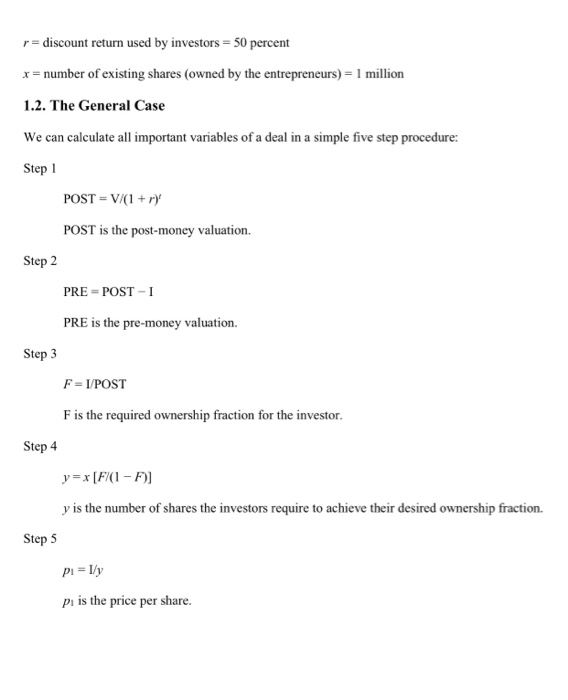

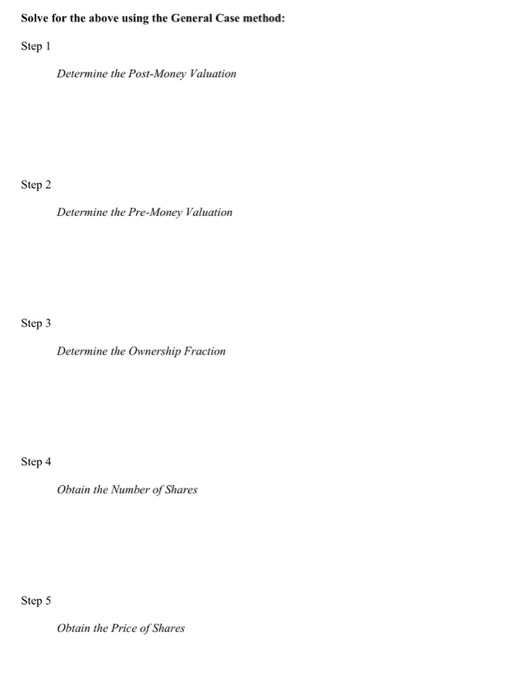

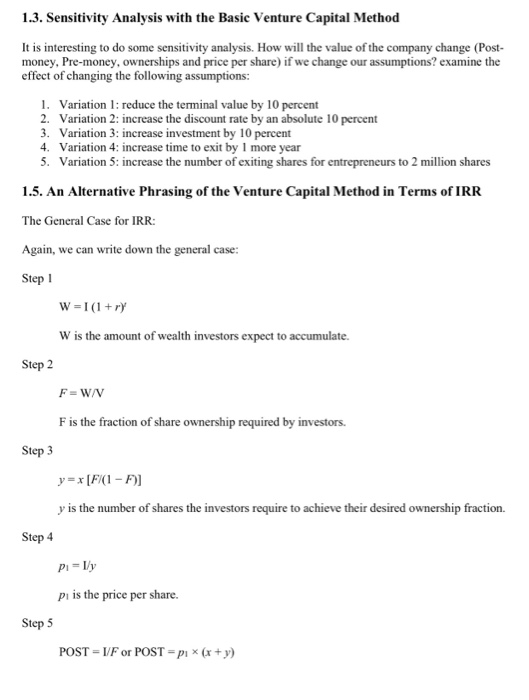

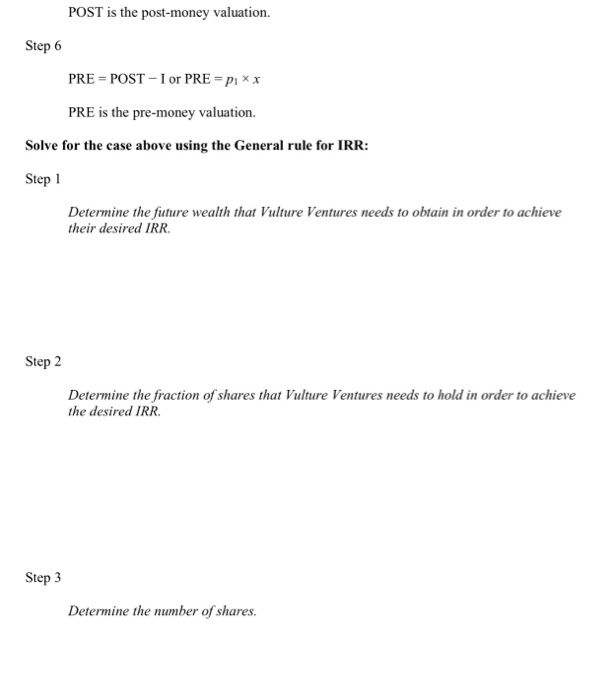

Appendix: A Note on Valuation of Venture Capital Deals This note was prepared by Thomas Hellmann, Assistant Professor of Strategic Management, Stanford University, as the basis for class discussion rather than to illustrate either effective or ineffective handling of an administrative situation. A Note on Valuation of Venture Capital Deals," by Thomas Hellmann, revised April 20, 2006. Copyright 2001 by the Board of Trustees of Leland Stanford Junior University. All rights reserved. Used with permission from the Stanford University Graduate School of Business When times are mysterious serious numbers are eager to please. - Musician, Paul Simon, in the lyrics to his song When Numbers Get Serious In this note, I discuss some of the fundamental issues of valuation in venture capital deals. The topics discussed are not necessarily limited to venture capital-backed companies, but they frequently surface in entrepreneurial companies that are financed either by venture capitalists or other private equity investors. 1. The Basic Venture Capital Method 1.1. An Example There exists a simple approach to valuation that is sometimes referred to as the venture capital method. The method is sometimes explained in the language of internal rates of retum (IRR) and sometimes in terms of NPV. Since most of you have been more exposed to the NPV framework, I will use that language, we will then show that it is in fact identical to the IRR framework. To illustrate the method we will use a fictional start-up company called "Spiffy Calc," which is seeking financing from a venture capital fund by the name of "Vulture Ventures. Studying their crystal ball, the founders of SpiffyCalc expect to be able to sell the company for $25 million in four years. At this point they need to raise $3 million. Vulture Ventures considers this a risky business and wants to apply a discount rate of 50 percent to be adequately compensated for the risk they will bear. The entrepreneurs also decided that whatever valuation they would get, they wanted to own 1 million shares, which they thought would be a cool number to brag about It is useful to define variables for the key assumptions we have made. V-terminal value (at time of exit) = $25 million (in four years) 1 time to exit event - 4 years 1 - amount of investment = $3 million r=discount return used by investors = 50 percent x= number of existing shares (owned by the entrepreneurs) = 1 million 1.2. The General Case We can calculate all important variables of a deal in a simple five step procedure: Step 1 POST = V/(1+r) POST is the post-money valuation. Step 2 PRE-POST-1 PRE is the pre-money valuation. Step 3 F = I/POST F is the required ownership fraction for the investor. Step 4 y=x[F/(1-F)] y is the number of shares the investors require to achieve their desired ownership fraction. Step 5 pi= 1/y pi is the price per share. Solve for the above using the General Case method: Step 1 Determine the Post-Money Valuation Step 2 Determine the Pre-Money Valuation Step 3 Determine the Ownership Fraction Step 4 Obtain the Number of Shares Step 5 Obtain the Price of Shares 1.3. Sensitivity Analysis with the Basic Venture Capital Method It is interesting to do some sensitivity analysis. How will the value of the company change (Post- money, Pre-money, ownerships and price per share) if we change our assumptions? examine the effect of changing the following assumptions: 1 Variation 1: reduce the terminal value by 10 percent 2. Variation 2: increase the discount rate by an absolute 10 percent 3. Variation 3: increase investment by 10 percent 4. Variation 4: increase time to exit by I more year 5. Variation 5: increase the number of exiting shares for entrepreneurs to 2 million shares 1.5. An Alternative Phrasing of the Venture Capital Method in Terms of IRR The General Case for IRR: Again, we can write down the general case: Step 1 W-I (1 + ry W is the amount of wealth investors expect to accumulate. Step 2 F-W/V F is the fraction of share ownership required by investors. Step 3 y=x[F/(1-F)] y is the number of shares the investors require to achieve their desired ownership fraction. Step 4 Pilly Pi is the price per share. Step 5 POST-VF or POST - Pix(x + y) POST is the post-money valuation. Step 6 PRE=POST-I or PRE=Pixx PRE is the pre-money valuation. Solve for the case above using the General rule for IRR: Step 1 Determine the future wealth that Vulture Ventures needs to obtain in order to achieve their desired IRR Step 2 Determine the fraction of shares that Vulture Ventures needs to hold in order to achieve the desired IRR Step 3 Determine the number of shares. Step 4 Determine the price of shares. Step 5 Determine post-money valuation. Step 6 Determine pre-money valuation