Answered step by step

Verified Expert Solution

Question

1 Approved Answer

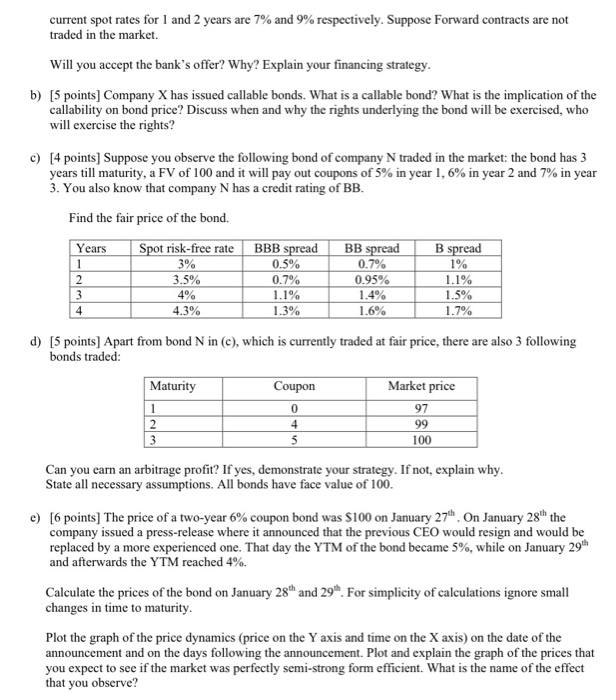

solve only d) and e) please solve only d) and e) point, no other questions a) [5 points) Your company is developing a project for

solve only d) and e) please

solve only d) and e) point, no other questions

a) [5 points) Your company is developing a project for which it will need to obtain a one-year $100k loan in one year. The bank has just offered to extend you loan such a loan and you will be required to pay an 11,5% interest rate on it. You are also provided with the following information about the current market: current spot rates for 1 and 2 years are 7% and 9% respectively. Suppose Forward contracts are not traded in the market. Will you accept the bank's offer? Why? Explain your financing strategy b) [5 points] Company X has issued callable bonds. What is a callable bond? What is the implication of the callability on bond price? Discuss when and why the rights underlying the bond will be exercised, who will exercise the rights? c) [4 points] Suppose you observe the following bond of company N traded in the market: the bond has 3 years till maturity, a FV of 100 and it will pay out coupons of 5% in year 1, 6% in year 2 and 7% in year 3. You also know that company N has a credit rating of BB. Find the fair price of the bond. Years Spot risk-free rate 3% 3.5% 4% 4.3% BBB spread 0.5% 0.7% 1.1% 1.3% BB spread 0.7% 0.95% 1.4% 1.6% B spread 1% 1.1% 1.5% 1.7% d) [5 points] Apart from bond N in (c), which is currently traded at fair price, there are also 3 following bonds traded: Maturity Coupon 0 Market price 97 99 4 100 Can you earn an arbitrage profit? If yes, demonstrate your strategy. If not, explain why. State all necessary assumptions. All bonds have face value of 100. e) [6 points) The price of a two-year 6% coupon bond was $100 on January 27th. On January 28 the company issued a press-release where it announced that the previous CEO would resign and would be replaced by a more experienced one. That day the YTM of the bond became 5%, while on January 29 and afterwards the YTM reached 4%. Calculate the prices of the bond on January 28 and 29. For simplicity of calculations ignore small changes in time to maturity. Plot the graph of the price dynamics (price on the Y axis and time on the X axis) on the date of the announcement and on the days following the announcement. Plot and explain the graph of the prices that you expect to see if the market was perfectly semi-strong form efficient. What is the name of the effect that you observe? a) [5 points) Your company is developing a project for which it will need to obtain a one-year $100k loan in one year. The bank has just offered to extend you loan such a loan and you will be required to pay an 11,5% interest rate on it. You are also provided with the following information about the current market: current spot rates for 1 and 2 years are 7% and 9% respectively. Suppose Forward contracts are not traded in the market. Will you accept the bank's offer? Why? Explain your financing strategy b) [5 points] Company X has issued callable bonds. What is a callable bond? What is the implication of the callability on bond price? Discuss when and why the rights underlying the bond will be exercised, who will exercise the rights? c) [4 points] Suppose you observe the following bond of company N traded in the market: the bond has 3 years till maturity, a FV of 100 and it will pay out coupons of 5% in year 1, 6% in year 2 and 7% in year 3. You also know that company N has a credit rating of BB. Find the fair price of the bond. Years Spot risk-free rate 3% 3.5% 4% 4.3% BBB spread 0.5% 0.7% 1.1% 1.3% BB spread 0.7% 0.95% 1.4% 1.6% B spread 1% 1.1% 1.5% 1.7% d) [5 points] Apart from bond N in (c), which is currently traded at fair price, there are also 3 following bonds traded: Maturity Coupon 0 Market price 97 99 4 100 Can you earn an arbitrage profit? If yes, demonstrate your strategy. If not, explain why. State all necessary assumptions. All bonds have face value of 100. e) [6 points) The price of a two-year 6% coupon bond was $100 on January 27th. On January 28 the company issued a press-release where it announced that the previous CEO would resign and would be replaced by a more experienced one. That day the YTM of the bond became 5%, while on January 29 and afterwards the YTM reached 4%. Calculate the prices of the bond on January 28 and 29. For simplicity of calculations ignore small changes in time to maturity. Plot the graph of the price dynamics (price on the Y axis and time on the X axis) on the date of the announcement and on the days following the announcement. Plot and explain the graph of the prices that you expect to see if the market was perfectly semi-strong form efficient. What is the name of the effect that you observe Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Global Corporate Finance A Focused Approach

Authors: Suk Hi Kim, Kenneth A Kim

2nd Edition

9814618004, 9789814618007