Answered step by step

Verified Expert Solution

Question

1 Approved Answer

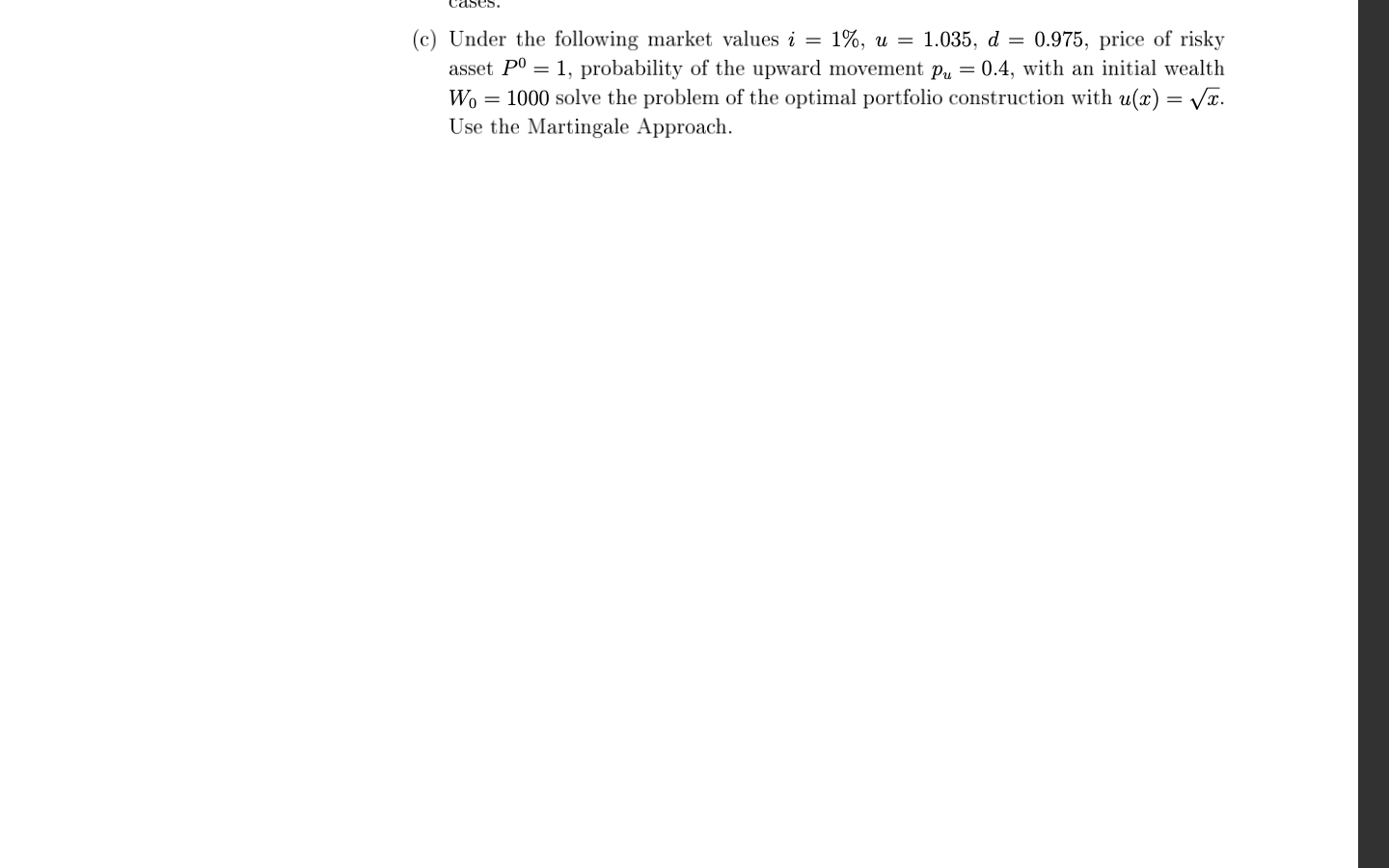

Solve step by step showing computations (c) Under the following market values i=1%,u=1.035,d=0.975, price of risky asset P0=1, probability of the upward movement pu=0.4, with

Solve step by step showing computations

(c) Under the following market values i=1%,u=1.035,d=0.975, price of risky asset P0=1, probability of the upward movement pu=0.4, with an initial wealth W0=1000 solve the problem of the optimal portfolio construction with u(x)=x. Use the Martingale ApproachStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance In Theory And Practice

Authors: Richard Abel Musgrave, Peggy B. Muscrave

5th Edition

0070441278, 978-0070441279