Solve the questions below;

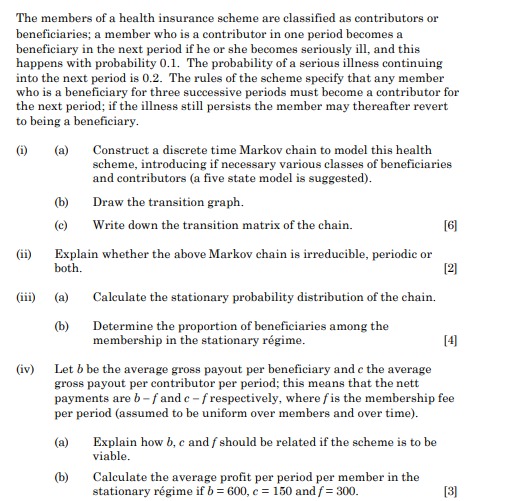

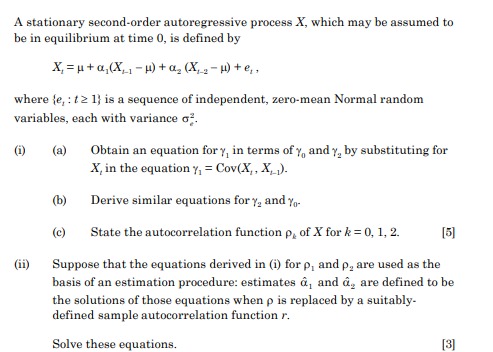

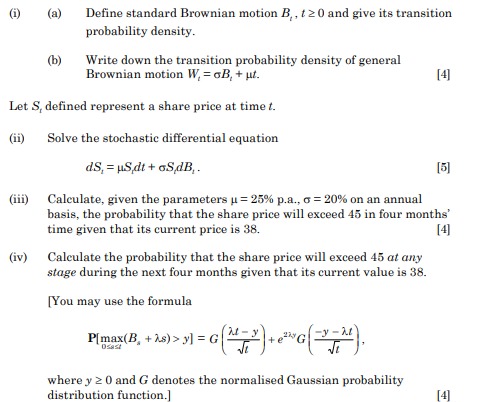

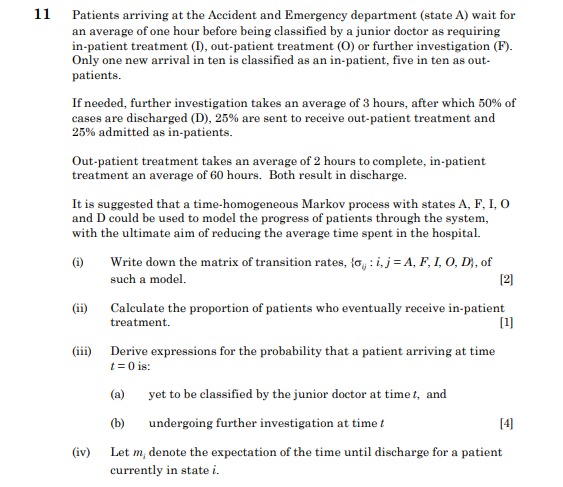

The members of a health insurance scheme are classified as contributors or beneficiaries; a member who is a contributor in one period becomes a beneficiary in the next period if he or she becomes seriously ill, and this happens with probability 0.1. The probability of a serious illness continuing into the next period is 0.2. The rules of the scheme specify that any member who is a beneficiary for three successive periods must become a contributor for the next period; if the illness still persists the member may thereafter revert to being a beneficiary. (i) (a) Construct a discrete time Markov chain to model this health scheme, introducing if necessary various classes of beneficiaries and contributors (a five state model is suggested). (b) Draw the transition graph. (c) Write down the transition matrix of the chain. [6] (ii) Explain whether the above Markov chain is irreducible, periodic or both. [2] (iii) Calculate the stationary probability distribution of the chain. (b) Determine the proportion of beneficiaries among the membership in the stationary regime. [4] (iv) Let b be the average gross payout per beneficiary and c the average gross payout per contributor per period; this means that the nett payments are b -f and c - f respectively, where f is the membership fee per period (assumed to be uniform over members and over time). (a) Explain how b, c and / should be related if the scheme is to be viable. (b) Calculate the average profit per period per member in the stationary regime if b = 600, c = 150 and f = 300. [3]A stationary second-order autoregressive process X, which may be assumed to be in equilibrium at time 0, is defined by X, =u+a, (X_ , - H) +a. ( X,,- l)+e, , where {e, : 12 1) is a sequence of independent, zero-mean Normal random variables, each with variance oz. (i) (a) Obtain an equation for y in terms of y, and y, by substituting for X, in the equation y, = Cov(X, , X, j). (b) Derive similar equations for y, and Y- (c) State the autocorrelation function p, of X for # = 0, 1, 2. (ii) Suppose that the equations derived in (i) for p, and p, are used as the basis of an estimation procedure: estimates a, and , are defined to be the solutions of those equations when p is replaced by a suitably- defined sample autocorrelation function r. Solve these equations.(1) (a) Define standard Brownian motion B, / 20 and give its transition probability density. (b) Write down the transition probability density of general Brownian motion W = GB, + ut. [4] Let S, defined represent a share price at time . (ii) Solve the stochastic differential equation dS, = US,dt + oSdB, . [5] (iii) Calculate, given the parameters u = 25% p.a., o = 20% on an annual basis, the probability that the share price will exceed 45 in four months" time given that its current price is 38. [4] (iv) Calculate the probability that the share price will exceed 45 at any stage during the next four months given that its current value is 38. [You may use the formula P[max(B, + As) > >] = G where y 2 0 and G denotes the normalised Gaussian probability distribution function.] [4]11 Patients arriving at the Accident and Emergency department (state A) wait for an average of one hour before being classified by a junior doctor as requiring in-patient treatment (I), out-patient treatment (O) or further investigation (F). Only one new arrival in ten is classified as an in-patient, five in ten as out- patients. If needed, further investigation takes an average of 3 hours, after which 50% of cases are discharged (D), 25% are sent to receive out-patient treatment and 25% admitted as in-patients. Out-patient treatment takes an average of 2 hours to complete, in-patient treatment an average of 60 hours. Both result in discharge. It is suggested that a time-homogeneous Markov process with states A, F, I, O and D could be used to model the progress of patients through the system, with the ultimate aim of reducing the average time spent in the hospital. Write down the matrix of transition rates, (o, : i, j = A, F, I, O, D), of such a model. [2] (ii) Calculate the proportion of patients who eventually receive in-patient treatment. [1] (iii) Derive expressions for the probability that a patient arriving at time { =0 is: (a) yet to be classified by the junior doctor at time t, and (b) undergoing further investigation at time / [4] (iv) Let m, denote the expectation of the time until discharge for a patient currently in state i.(a) Explain in words why m satisfies the following equation: m= where A = > o, - (b) Hence calculate the expectation of the total time until discharge for a newly-arrived patient. [4] (v) State the distribution of the time spent in each state visited according to this model. ] The average times listed above may be assumed to be the sample mean waiting times derived from tracking a large sample of patients through the system. (vi) Describe briefly what additional feature of the data might be used to check that this simple model matches the situation being modelled. [2](vii) The hospital management committee believes that replacing the junior doctor with a more senior doctor will save resources by reducing the proportion of cases sent for further investigation. Alternatively, the same resources could go towards reducing out-patient treatment time. (a) Outline briefly the calculations that would need to be performed to compare the options. (b) Discuss whether the current model is suitable as a basis for making decisions of this nature. [4]