Answered step by step

Verified Expert Solution

Question

1 Approved Answer

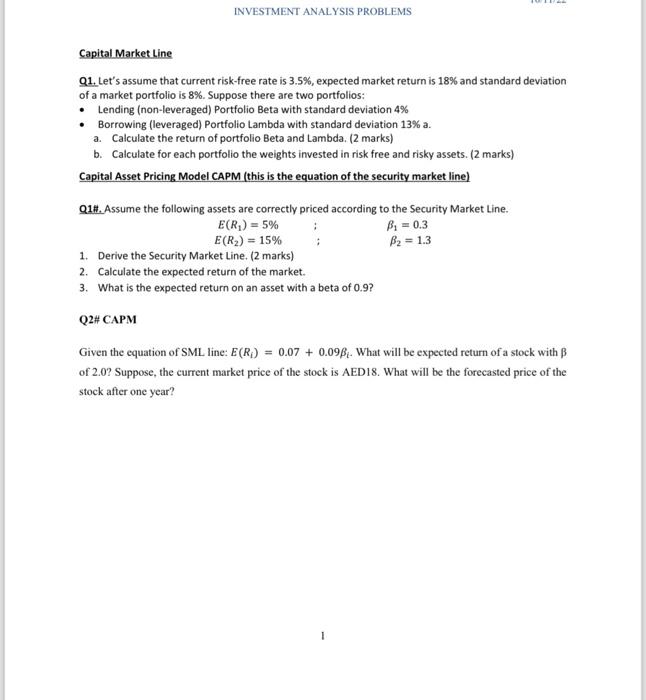

solve them all don't use tables write them Capital Market Line Q1.Let's assume that current risk-free rate is 3.5%, expected market return is 18% and

solve them all don't use tables write them

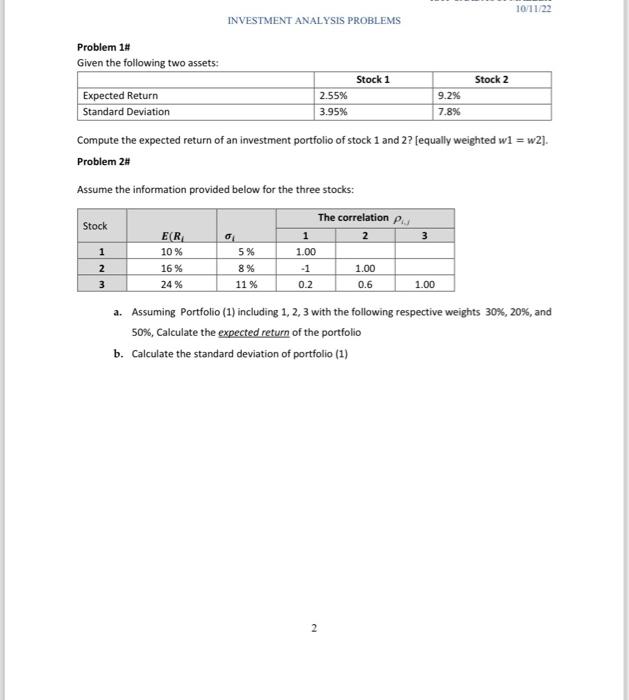

Capital Market Line Q1.Let's assume that current risk-free rate is 3.5%, expected market return is 18% and standard deviation of a market portfolio is 8%. Suppose there are two portfolios: - Lending (non-leveraged) Portfolio Beta with standard deviation 4% - Borrowing (leveraged) Portfolio Lambda with standard deviation 13% a. a. Calculate the return of portfolio Beta and Lambda. (2 marks) b. Calculate for each portfolio the weights invested in risk free and risky assets. (2 marks) Capital Asset Pricing Model CAPM (this is the equation of the security market line) Q1H. Assume the following assets are correctly priced according to the Security Market Line. E(R1)=5%E(R2)=15%;;1=0.32=1.3 1. Derive the Security Market Line. ( 2 marks) 2. Calculate the expected return of the market. 3. What is the expected return on an asset with a beta of 0.9 ? Q2\# CAPM Given the equation of SML line: E(Ri)=0.07+0.09i. What will be expected return of a stock with of 2.0 ? Suppose, the current market price of the stock is AED18. What will be the forecasted price of the stock after one year? Problem 1\# Given the following two assets: Compute the expected return of an investment portfolio of stock 1 and 2 ? [equally weighted w1=w2 ]. Problem 2\# Assume the information provided below for the three stocks: a. Assuming Portfolio (1) including 1, 2, 3 with the following respective weights 30%,20%, and 50%, Calculate the expected return of the portfolio b. Calculate the standard deviation of portfolio (1) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Structured Finance

Authors: Arnaud De Servigny, Norbert Jobst

1st Edition

0071468641, 978-0071468640