Answered step by step

Verified Expert Solution

Question

1 Approved Answer

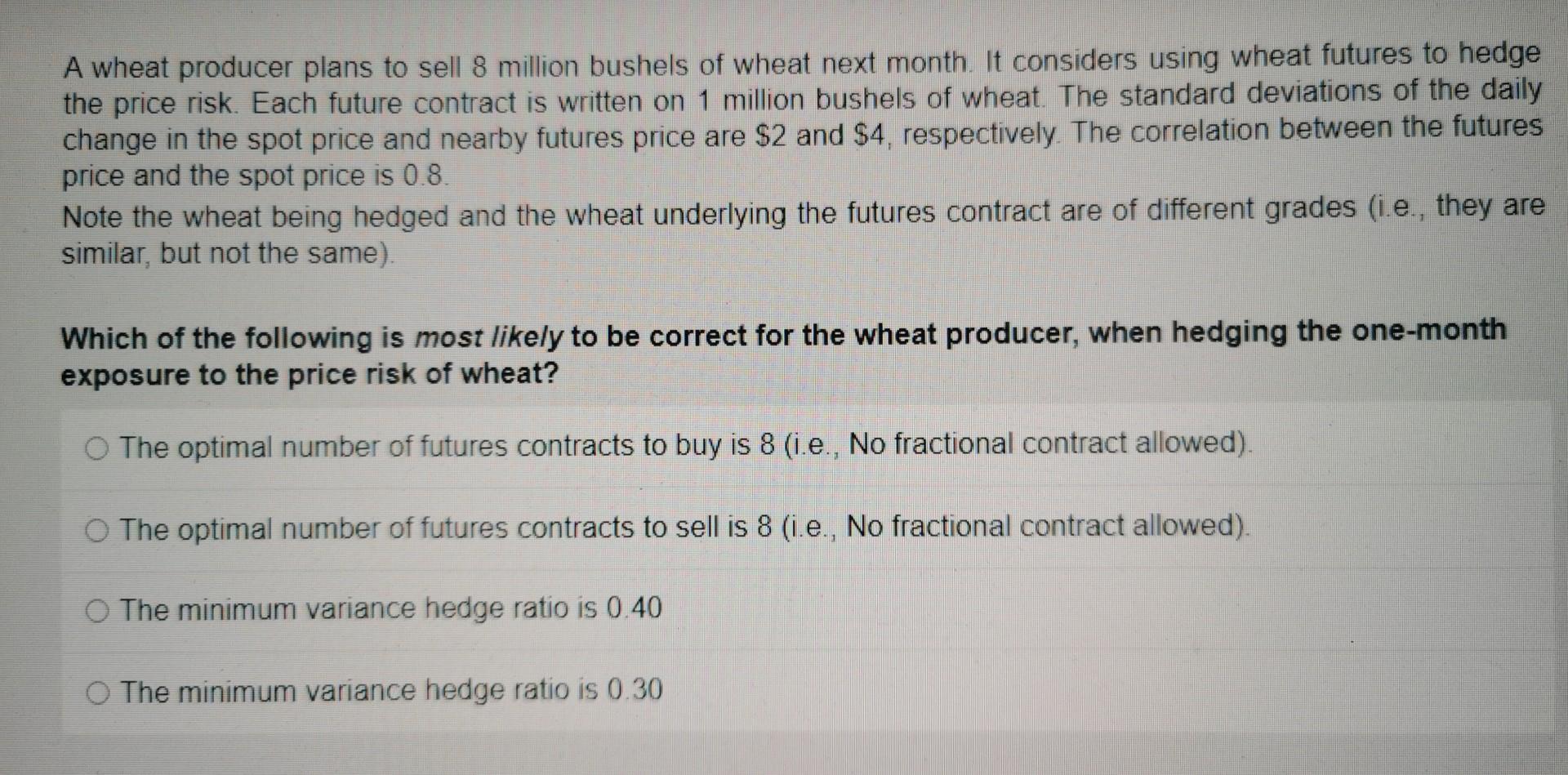

Solve this hedging question A wheat producer plans to sell 8 million bushels of wheat next month. It considers using wheat futures to hedge the

Solve this hedging question

A wheat producer plans to sell 8 million bushels of wheat next month. It considers using wheat futures to hedge the price risk. Each future contract is written on 1 million bushels of wheat. The standard deviations of the daily change in the spot price and nearby futures price are $2 and $4, respectively. The correlation between the futures price and the spot price is 0.8 Note the wheat being hedged and the wheat underlying the futures contract are of different grades (i.e., they are similar, but not the same). Which of the following is most likely to be correct for the wheat producer, when hedging the one-month exposure to the price risk of wheat? The optimal number of futures contracts to buy is 8 (i.e., No fractional contract allowed). The optimal number of futures contracts to sell is 8 (i.e., No fractional contract allowed). The minimum variance hedge ratio is 0.40 The minimum variance hedge ratio is 0.30Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Making Sense Of School Finance

Authors: Clinton Born

1st Edition

1475856652, 978-1475856651