Some of these questions require you to answer specically based on the information provided for Chesapeake Energy and others are based on more general issues.

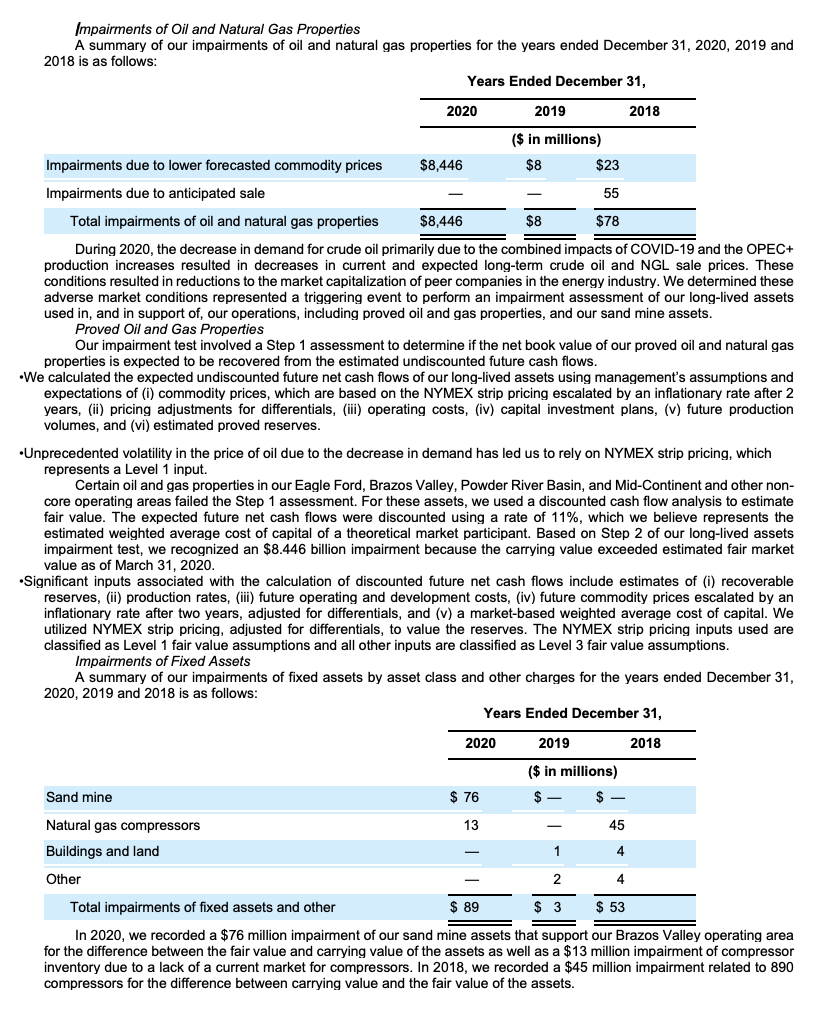

Some of these questions require you to answer specically based on the information provided for Chesapeake Energy and others are based on more general issues. 1. What is the real cost of finding a barrel of oil? In particular should exploration costs be capitalized or expensed? 2. Should the costs of exploration costs on unproved properties be treated differently from those on properties where an oil well is already productive (proved properties). 3. In articular sh_o_uld the cost of drilling an exploratory well on an oil-bearing property that does not lead to a find (a.k.a dry hole) be capitalized? What did Chesapeake do with these costs? 4. What was the capitalized cost of oil properties of Chesapeake on their balance sheet in 2019 and 2020'? What was the depletion and amortization of these costs in 2019 and 2020'? Based on this information, what can you infer about the oil properties of Chesapeake? 5. Do you think that Chesapeake was doing exploration in 2019 and 2020? Can an oil company survive without such expenditures? Impairment Testing Impairment Testing is a complex process. I summarize the steps so you can understand and read Chesapeake's Impairment footnote First, there has to be a triggering event that makes a firm suspect that their asset is impaired. In the case of Chesapeake, it was the onset of Wand increase in OPEC+ production. The next step in impairment testing (Called Step 1) requires the firm to project out the cash ows from the asset and sum up these cash ows (undiscounted). If the sum of undiscounted cash ows is less than the NBV of the asset, Step 2 is triggered In Step 2, the firm needs to calculate the discounted cashowsfmm the mm! and book an impairment for the difference between the NBV of the asset (here in 2019) and the new value of the asset (in 2020). In doing Step 2, the firm may use Level 1 inputs (observable in the market), Level 2 inputs (comparable to market observables} or Level 3 inputs (rm's judgment). In Chesapeake's case, Level 1 and Level 3 were used. The numbers do not add up neatly because Chesapeake did some acquisitions and divestimres. Do not worry about that. Questions on Impairment . Why did Chesapeake need to use the WOH price in doing the impairment calculation? (Hint: How would you calculate the value of the lOil to be extracted from the property)? . Chesapeake uses 11% as the rate for calculating their asset value. What do you think of this assumption? . In view of the Oil price in 2022, what do you feel about Chesapeake's impairment? Impairments of Oil and Natural Gas Properties A summary of our impairments of oil and natural gas properties for the years ended December 31, 2020, 2019 and 2018 is as follows: Years Ended December 31, 2020 2019 2018 ($ in millions) Impairments due to lower forecasted commodity prices $8,446 $8 $23 Impairments due to anticipated sale 55 Total impairments of oil and natural gas properties $8,446 $8 $78 During 2020, the decrease in demand for crude oil primarily due to the combined impacts of COVID-19 and the OPEC+ production increases resulted in decreases in current and expected long-term crude oil and NGL sale prices. These conditions resulted in reductions to the market capitalization of peer companies in the energy industry. We determined these adverse market conditions represented a triggering event to perform an impairment assessment of our long-lived assets used in, and in support of, our operations, including proved oil and gas properties, and our sand mine assets. Proved Oil and Gas Properties Our impairment test involved a Step 1 assessment to determine if the net book value of our proved oil and natural gas properties is expected to be recovered from the estimated undiscounted future cash flows. .We calculated the expected undiscounted future net cash flows of our long-lived assets using management's assumptions and expectations of (i) commodity prices, which are based on the NYMEX strip pricing escalated by an inflationary rate after 2 years, (ii) pricing adjustments for differentials, (iii) operating costs, (iv) capital investment plans, (v) future production volumes, and (vi) estimated proved reserves. .Unprecedented volatility in the price of oil due to the decrease in demand has led us to rely on NYMEX strip pricing, which represents a Level 1 input. Certain oil and gas properties in our Eagle Ford, Brazos Valley, Powder River Basin, and Mid-Continent and other non- core operating areas failed the Step 1 assessment. For these assets, we used a discounted cash flow analysis to estimate fair value. The expected future net cash flows were discounted using a rate of 11%, which we believe represents the estimated weighted average cost of capital of a theoretical market participant. Based on Step 2 of our long-lived assets impairment test, we recognized an $8.446 billion impairment because the carrying value exceeded estimated fair market value as of March 31, 2020. .Significant inputs associated with the calculation of discounted future net cash flows include estimates of (i) recoverable reserves, (ii) production rates, (iii) future operating and development costs, (iv) future commodity prices escalated by an inflationary rate after two years, adjusted for differentials, and (v) a market-based weighted average cost of capital. We utilized NYMEX strip pricing, adjusted for differentials, to value the reserves. The NYMEX strip pricing inputs used are classified as Level 1 fair value assumptions and all other inputs are classified as Level 3 fair value assumptions. Impairments of Fixed Assets A summary of our impairments of fixed assets by asset class and other charges for the years ended December 31, 2020, 2019 and 2018 is as follows: Years Ended December 31, 2020 201 2018 ($ in millions) Sand mine $ 76 $ Natural gas compressors 13 45 Buildings and land 1 4 Other 2 4 Total impairments of fixed assets and other $ 89 $ 3 $ 53 In 2020, we recorded a $76 million impairment of our sand mine assets that support our Brazos Valley operating area for the difference between the fair value and carrying value of the assets as well as a $13 million impairment of compressor inventory due to a lack of a current market for compressors. In 2018, we recorded a $45 million impairment related to 890 compressors for the difference between carrying value and the fair value of the assets

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance