Answered step by step

Verified Expert Solution

Question

1 Approved Answer

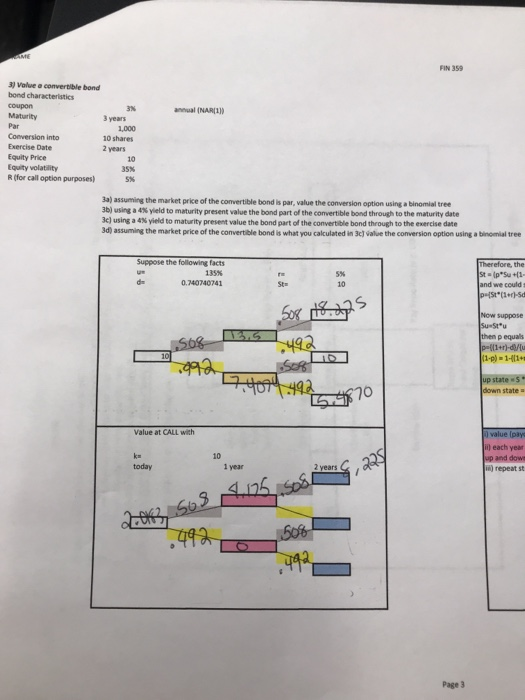

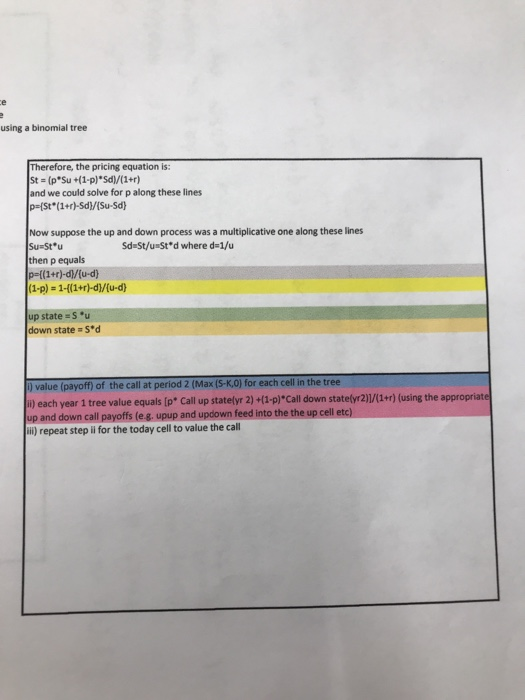

Someone please let me know if this is correct IN 359 3) Value a convertible bond annual (NAR(1 s years Par Coeversion into Exercise Date

Someone please let me know if this is correct

Someone please let me know if this is correct Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials Of Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

6th Edition

0073226386, 978-0073226385