Question

SPARK PUBLISHING AND PRINTING HOUSE: SHORT-RUN MANAGERIAL DECISION RAISES A HAMLET-LIKE DILEMMA It was a sunny Monday morning in March 2014. Sameer Sheth, the young

SPARK PUBLISHING AND PRINTING HOUSE: SHORT-RUN MANAGERIAL DECISION RAISES A HAMLET-LIKE DILEMMA

It was a sunny Monday morning in March 2014. Sameer Sheth, the young and dynamic proprietor of Spark Publishing and Printing House, was engrossed in the proposal his management team had put before him. He was oblivious to both the rising temperature outside and the serene coolness of his spacious, tastefully designed office. This was the first major decision he had been required to make after taking over the reins of the family business from his father in January, barely two months ago. He knew that all eyes would be on him. Apart from the expectations of his employees, he also had the legacy of his father and grandfather to consider. He did not want to fail either.

THE BACKGROUND Spark Publishing and Printing House had very humble beginnings. Inspired by the Indian independence movement led by Mahatma Gandhi in the late 1930s, Narottamdas Sheth established Spark Printing Press, a small operation, near his mansion in Ahmadabad, in the western Indian state of Gujarat. Though he had a degree in English Literature from England, the political environment in India prompted him to start a Gujarati daily, NavoAwaj. After independence, Narottamdas continued publishing the daily and also introduced an English monthly magazine called Spark. His untimely death forced his only son, Sudhir Sheth, to quit his studies in England and take on the responsibilities of the business. Sudhir had inherited his fathers business acumen. He ventured into publishing, and Spark Printing Press became Spark Publishing and Printing House (SPPH). The business expanded as SPPH began publishing academic literature, technical manuals, religious publications and books by reputed authors. In the publishing world, SPPH became a well-known name. Sudhir had one regret that he had to discontinue the daily and the magazine his father had started as both had become uneconomical in the new business model. Sudhir divided the business into two departments, one of which was Publishing and the other, Printing and Distribution. The Publishing Department handled negotiations, editorial responsibilities and design while the Printing and Distribution Department (P&D) dealt with the printing, binding and distribution of published material. He had modernized the printing department with the acquisition of a state-of-the-art printing machine at a cost of INR 2,000,000. When his son Sameer returned from the United States with a management degree from a prestigious institute, Sudhir decided to hand over the reins of the business to him. After a long and successful business career, Sudhir intended to devote more time to his family and rediscover long neglected hobbies. Bowing to his fathers wishes, Sameer took over the business in January 2014. Over the next two months, he tracked the trends and rapid changes in the publishing industry. The 21st century had brought in a number of radical technological changes and innovations in publishing. With the advent of digital information systems and the Internet, the scope of publishing had expanded to include electronic resources such as e-books, micro-publishing, websites, blogs and video game publishing, among others. On the printing front, many small companies providing specialized printing and distribution facilities had emerged.

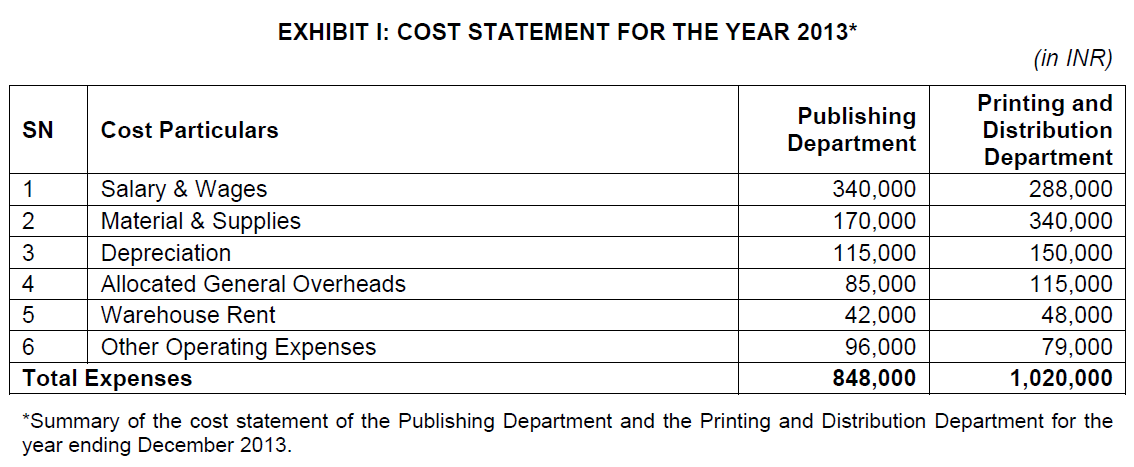

THE PROPOSAL The proposal the company was now considering was from Fine Printing Press (FPP), which offered to handle all of SPPHs printing and distribution work for a monthly payment of INR 75,000. The initial contract period was for one year, after which it could be renewed with mutual consent. Sameer had always been more interested in the publishing side of the business, which he regarded as creative, than the printing side. This proposal gave him the opportunity to discontinue the P&D Department and concentrate entirely on publishing. Sameer learned that another printing press had made a similar proposal to SPPH in the past and that his father had rejected it. Sudhirs reasoning at the time was that the printing press in which he had invested had not fully depreciated. Further, the overheads allocated to the P&D Department were considerable and would have to be dumped on the Publishing Department. He was also reluctant to lay off Printing Department staff, some of whom had been appointed by his father, Narottamdas. Now, as he reviewed FPPs proposal, Sameer decided to rethink his options. On the face of it, the proposal looked very attractive. The total cost of running the P&D department was INR 85,000 per month (see Exhibit 1); whereas if SPPH outsourced printing and distribution to FPP, it would be required to pay only INR 75,000 per month. However, Sameer had studied the concept of relevant cost and knew that the correct way to evaluate the proposal was to make a relevant cost analysis for and against closing down the P&D Department. Unlike his father, he was not worried about the cost of the machine or overheads allocated to the department as he knew that past costs and non-differential costs were irrelevant in managerial decisions and must be ignored. But he was concerned about the retrenchment of staff, especially those who had spent their entire working life serving the firm. He decided to work out some acceptable arrangement so that the proposal could be analyzed purely from a financial perspective. Sameer was sure of one thing. If he decided to outsource the printing function after the analysis was completed, he would have to be sure of the quality and efficiency of the printing and distribution services offered by FPP. In the publishing business, SPPH commanded a lot of respect and he did not wish to do anything that could tarnish its image. Sameer called for the previous years financial performance data (see Exhibit 1). With the required figures at his disposal, he began analyzing the likely effect of the proposal on the financials of the firm. He also had to consider the following information in making any decision on the possible closure of the P&D Department: 1. From the P&D staff, Manek and Hiralal had been with the firm for almost 35 years. They were due for retirement and would be entitled to collect on the firms Employee Pension Plan in two years. If he decided in favor of closing the department, Sameer intended to give each of them a pension equivalent to their present salary of INR 2,000 per month until they became eligible for their pension. Two specialist staff of the P&D department would have to be retained at their present salary of INR 4,000 per month in order to coordinate the work with FPP. 2. The position of Publishing Department manager was likely to fall vacant. Sameer decided to appoint Ashwin, the manager of the P&D Department, to that post. Though Ashwin had not formally accepted the position, Sameer believed he would not oppose the transfer as the manager of the Publishing Department was earning INR 6,500 per month, which was more than Ashwins current salary of INR 6,000 per month. 3. The rest of the staff would have to be laid off. They were all contractual appointments. According to the terms of their contracts, the firm would have to pay them 15 months salary as retrenchment compensation. 4. The P&D Department had a stock of printing material worth INR 90,000. FPP was prepared to purchase the stock for INR 88,000. For the rest of the material it required, SPPH had entered into an agreement with the supplier to ensure uninterrupted delivery. The agreement included a cancellation penalty equivalent to 10% of the value of supplies cancelled. 5. Depreciation expense included depreciation on machinery with an original cost of INR 2,000,000. The machine had been purchased 18 years earlier and had an economic life of 20 years; depreciation had been calculated on straight line method (SLM) basis. It could be sold at scrap value, resulting in a loss of INR 75,000. 6. Depreciation on a distribution vehicle owned by the P&D Department was calculated on written down value (WDV) basis. The written down value of the vehicle was INR 200,000. FPP was prepared to pay INR 100,000 for the vehicle but Sameer was more inclined to hold on to it for the companys general use. 7. General overhead costs were head office costs allocated on the basis of the area occupied by each department. Closing the P&D Department would make it possible to rent out the space it occupied for INR 5,000 per month. 8. The P&D department had a five-year lease on a warehouse, with three years left on the lease. Since it was not possible to cancel the lease, Sameer was left with two options if he decided to close the department. He could use the P&D warehouse for the Publishing Department and terminate its lease on the warehouse it was currently using. Since the warehouse being used by the Publishing Department was rented on a yearly basis, the firm could save on the rent of that warehouse. The other option was to sublease the P&D warehouse for INR 3,000 per month. 9. Other operating expenses included the administration and selling costs of the department. In case of a temporary closure, expenses worth INR 15,000 would be unavoidable, but the firm would not incur the rest of the expenses. Sameer had asked FPP to give him a week to think about their proposal. Privately, he wanted to outsource the P&D Department for one year but he knew that his final decision would depend on the relevant cost analysis and the figures it showed.

Questions

1. Determine the period of evaluation.

2. Determine the alternatives available for evaluation.

3. Prepare the relevant cost analysis based on future differential cash flows for each alternative.

4. Determine the least cost alternative to conclude whether the outsourcing proposal should be accepted or rejected.

Assuming that no additional information is available and considering the proposal from a purely financial perspective, would you, in Sameers position, accept FPPs proposal and close down the P&D Department for one year?

EXHIBIT I: COST STATEMENT FOR THE YEAR 2013* (in INR) SN Cost Particulars Publishing Department WN Salary & Wages Material & Supplies Depreciation 4 Allocated General Overheads 5 Warehouse Rent 6 Other Operating Expenses Total Expenses 340,000 170,000 115,000 85,000 42,000 96,000 848,000 Printing and Distribution Department 288,000 340,000 150,000 115,000 48,000 79,000 1,020.000 *Summary of the cost statement of the Publishing Department and the Printing and Distribution Department for the year ending December 2013. EXHIBIT I: COST STATEMENT FOR THE YEAR 2013* (in INR) SN Cost Particulars Publishing Department WN Salary & Wages Material & Supplies Depreciation 4 Allocated General Overheads 5 Warehouse Rent 6 Other Operating Expenses Total Expenses 340,000 170,000 115,000 85,000 42,000 96,000 848,000 Printing and Distribution Department 288,000 340,000 150,000 115,000 48,000 79,000 1,020.000 *Summary of the cost statement of the Publishing Department and the Printing and Distribution Department for the year ending December 2013Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started