Answered step by step

Verified Expert Solution

Question

1 Approved Answer

specific type of product to suit his needs. The job costing system is applicable in the case of a Single item or batch. It is

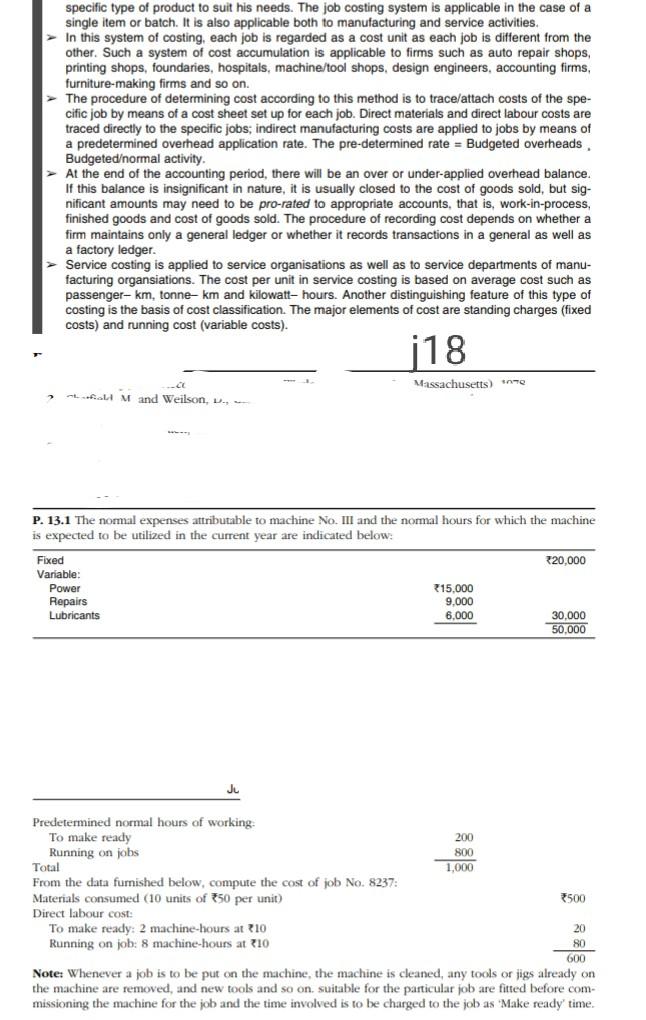

specific type of product to suit his needs. The job costing system is applicable in the case of a Single item or batch. It is also applicable both to manufacturing and service activities, In this system of costing, each job is regarded as a cost unit as each job is different from the other. Such a system of cost accumulation is applicable to firms such as auto repair shops, printing shops, foundaries, hospitals, machine/tool shops, design engineers, accounting firms, furniture-making firms and so on. The procedure of determining cost according to this method is to trace/attach costs of the spe- cific job by means of a cost sheet set up for each job. Direct materials and direct labour costs are traced directly to the specific jobs; indirect manufacturing costs are applied to jobs by means of a predetermined overhead application rate. The pre-determined rate = Budgeted overheads Budgetedormal activity. > At the end of the accounting period, there will be an over or under-applied overhead balance. If this balance is insignificant in nature, it is usually closed to the cost of goods sold, but sig. nificant amounts may need to be pro-rated to appropriate accounts, that is, work-in-process, finished goods and cost of goods sold. The procedure of recording cost depends on whether a firm maintains only a general ledger or whether it records transactions in a general as well as a factory ledger. Service costing is applied to service organisations as well as to service departments of manu- facturing organsiations. The cost per unit in service costing is based on average cost such as passenger- km, tonne-km and kilowatt-hours. Another distinguishing feature of this type of costing is the basis of cost classification. The major elements of cost are standing charges (fixed costs) and running cost (variable costs). 118 Massachusetts) ne Mad Weilson, D. P. 13.1 The normal expenses attributable to machine No. III and the normal hours for which the machine is expected to be utilized in the current year are indicated below: 320,000 Fixed Variable: Power Repairs Lubricants 215,000 9.000 6.000 30.000 50.000 Predetermined normal hours of working To make ready 200 Running on jobs 800 Total 1,000 From the data furnished below, compute the cost of job No. 8237: Materials consumed (10 units of 50 per unit) 3500 Direct labour cost: To make ready: 2 machine-hours at 10 20 Running on job: 8 machine-hours at 10 80 600 Note: Whenever a job is to be put on the machine, the machine is cleaned, any tools or jigs already on the machine are removed, and new tools and so on. suitable for the particular job are fitted before com- missioning the machine for the job and the time involved is to be charged to the job as "Make ready' time

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modern Auditing

Authors: Graham Cosserat

2nd Edition

0470863226, 978-0470863220