Answered step by step

Verified Expert Solution

Question

1 Approved Answer

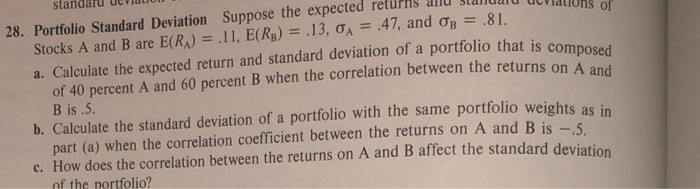

stand OS 01 28. Portfolio Standard Deviation Suppose the expected .47, and ob = .81. Stocks A and B are E(R) = .11, E(Rp) =

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Investing

Authors: Scott B. Smart, Lawrence J. Gitman, Michael D. Joehnk

12th edition

ISBN: 978-0133075403, 133075354, 9780133423938, 133075400, 013342393X, 978-0133075359