Answered step by step

Verified Expert Solution

Question

1 Approved Answer

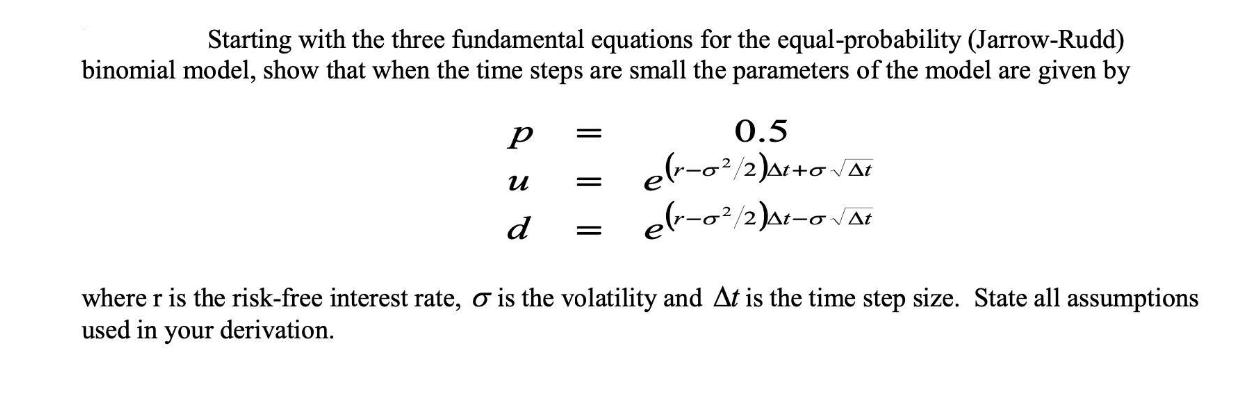

Starting with the three fundamental equations for the equal-probability (Jarrow-Rudd) binomial model, show that when the time steps are small the parameters of the

Starting with the three fundamental equations for the equal-probability (Jarrow-Rudd) binomial model, show that when the time steps are small the parameters of the model are given by U d = = = 0.5 er-0/2)41+0 At (r-0/2)M-0-AL where r is the risk-free interest rate, o is the volatility and At is the time step size. State all assumptions used in your derivation.

Step by Step Solution

★★★★★

3.39 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

The three fundamental equations for the equalprobability JarrowRudd binomial model are 1 The probability of a stock price increasing by a factor of 1 ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Elements Of Chemical Reaction Engineering

Authors: H. Fogler

6th Edition

013548622X, 978-0135486221