Answered step by step

Verified Expert Solution

Question

1 Approved Answer

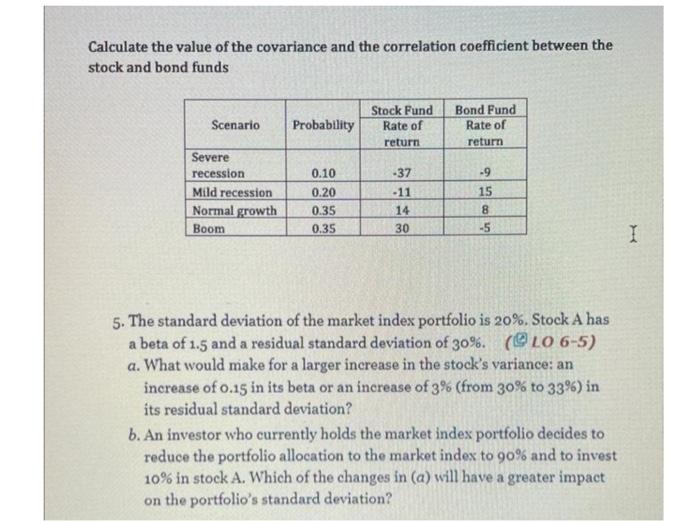

step by step in details Calculate the value of the covariance and the correlation coefficient between the stock and bond funds 5. The standard deviation

step by step in details

Calculate the value of the covariance and the correlation coefficient between the stock and bond funds 5. The standard deviation of the market index portfolio is 20%. Stock A has a beta of 1.5 and a residual standard deviation of 30%. ( LO65 ) a. What would make for a larger increase in the stock's variance: an increase of 0.15 in its beta or an increase of 3% (from 30% to 33% ) in its residual standard deviation? b. An investor who currently holds the market indes portfolio decides to reduce the portfolio allocation to the market index to 90% and to invest 10% in stock A. Which of the changes in (a) will have a greater impact on the portfolio's standard deviation Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cases In Healthcare Finance

Authors: Louis C. Gapenski

2nd Edition

1567932002, 978-1567932003