Answered step by step

Verified Expert Solution

Question

1 Approved Answer

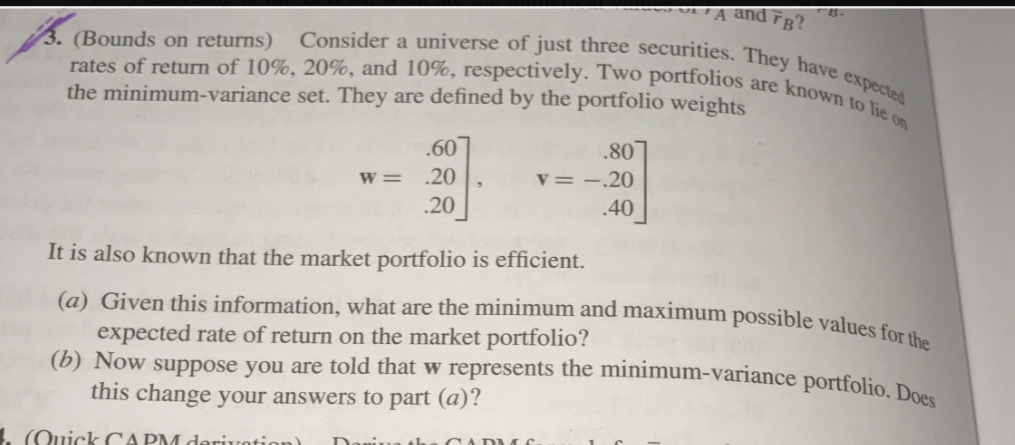

Step by Step Please include formulas. Please !! Thank You!! A and FB? (Bounds on returns) Consider a universe of just three securities rates of

Step by Step Please include formulas.

Please !!

Thank You!!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ISE Fundamentals Of Cost Accounting

Authors: William N. Lanen, Shannon Anderson, Michael W. Maher

7th Edition

1265117705, 9781265117702