Answered step by step

Verified Expert Solution

Question

1 Approved Answer

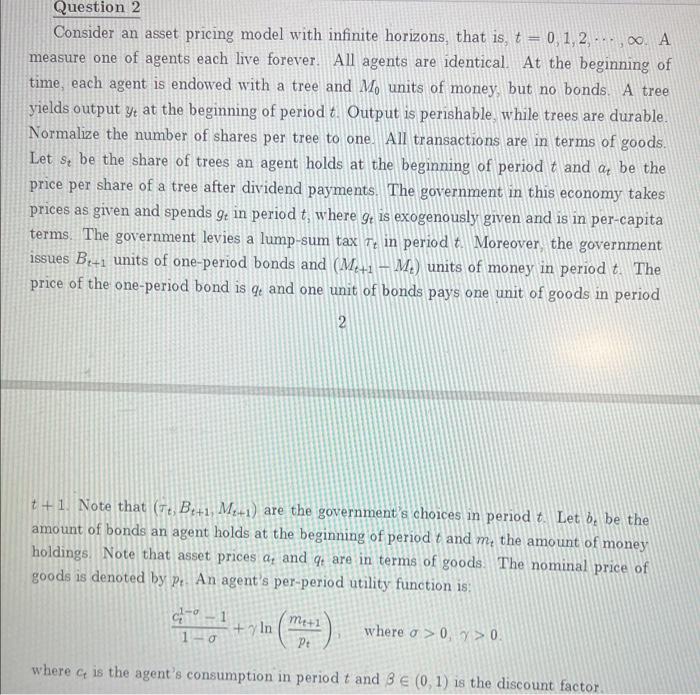

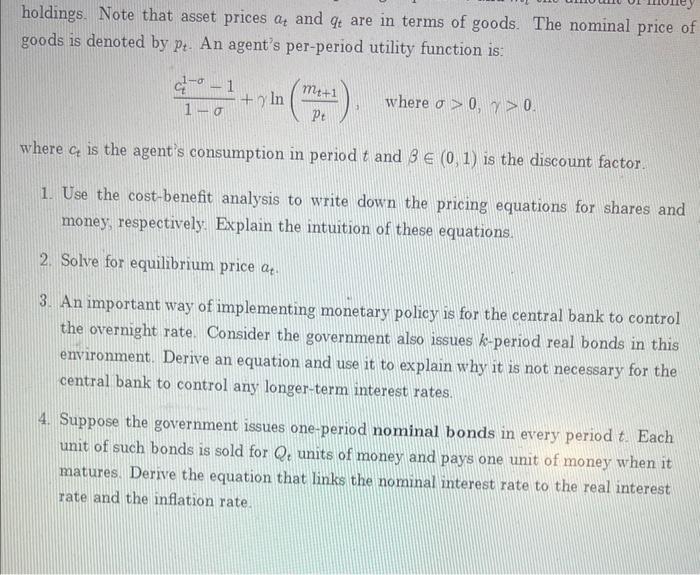

steps pls Consider an asset pricing model with infinite horizons, that is, t=0,1,2,,.A measure one of agents each live forever. All agents are identical. At

steps pls

Consider an asset pricing model with infinite horizons, that is, t=0,1,2,,.A measure one of agents each live forever. All agents are identical. At the beginning of time, each agent is endowed with a tree and M0 units of money, but no bonds. A tree yields output yt at the beginning of period t. Output is perishable, while trees are durable. Normalize the number of shares per tree to one. All transactions are in terms of goods. Let st be the share of trees an agent holds at the beginning of period t and at be the price per share of a tree after dividend payments. The government in this economy takes prices as given and spends gt in period t, where gt is exogenously given and is in per-capita terms. The government levies a lump-sum tax t in period t. Moreover, the government issues Bt+1 units of one-period bonds and (Mt+1Mt) units of money in period t. The price of the one-period bond is qt and one unit of bonds pays one unit of goods in period 2 t+1. Note that (t,Bt+1,Mt+1) are the government's choices in period t. Let bt be the amount of bonds an agent holds at the beginning of period t and mt the amount of money holdings. Note that asset prices at and qt are in terms of goods The nominal price of goods is denoted by pt. An agent's per-period utility function is: 1ct11+ln(ptmt+1)where>0,>0. where ct is the agent's consumption in period t and (0,1) is the discount factor. holdings. Note that asset prices at and qt are in terms of goods. The nominal price of goods is denoted by pt. An agent's per-period utility function is: 1ct11+ln(ptmt+1),where>0,>0. where ct is the agent's consumption in period t and (0,1) is the discount factor. 1. Use the cost-benefit analysis to write down the pricing equations for shares and money, respectively: Explain the intuition of these equations. 2. Solve for equilibrium price at. 3. An important way of implementing monetary policy is for the central bank to control the overnight rate. Consider the government also issues k-period real bonds in this environment. Derive an equation and use it to explain why it is not necessary for the central bank to control any longer-term interest rates. 4. Suppose the government issues one-period nominal bonds in every period t. Each unit of such bonds is sold for Qt units of money and pays one unit of money when it matures. Derive the equation that links the nominal interest rate to the real interest. rate and the inflation rate. Consider an asset pricing model with infinite horizons, that is, t=0,1,2,,.A measure one of agents each live forever. All agents are identical. At the beginning of time, each agent is endowed with a tree and M0 units of money, but no bonds. A tree yields output yt at the beginning of period t. Output is perishable, while trees are durable. Normalize the number of shares per tree to one. All transactions are in terms of goods. Let st be the share of trees an agent holds at the beginning of period t and at be the price per share of a tree after dividend payments. The government in this economy takes prices as given and spends gt in period t, where gt is exogenously given and is in per-capita terms. The government levies a lump-sum tax t in period t. Moreover, the government issues Bt+1 units of one-period bonds and (Mt+1Mt) units of money in period t. The price of the one-period bond is qt and one unit of bonds pays one unit of goods in period 2 t+1. Note that (t,Bt+1,Mt+1) are the government's choices in period t. Let bt be the amount of bonds an agent holds at the beginning of period t and mt the amount of money holdings. Note that asset prices at and qt are in terms of goods The nominal price of goods is denoted by pt. An agent's per-period utility function is: 1ct11+ln(ptmt+1)where>0,>0. where ct is the agent's consumption in period t and (0,1) is the discount factor. holdings. Note that asset prices at and qt are in terms of goods. The nominal price of goods is denoted by pt. An agent's per-period utility function is: 1ct11+ln(ptmt+1),where>0,>0. where ct is the agent's consumption in period t and (0,1) is the discount factor. 1. Use the cost-benefit analysis to write down the pricing equations for shares and money, respectively: Explain the intuition of these equations. 2. Solve for equilibrium price at. 3. An important way of implementing monetary policy is for the central bank to control the overnight rate. Consider the government also issues k-period real bonds in this environment. Derive an equation and use it to explain why it is not necessary for the central bank to control any longer-term interest rates. 4. Suppose the government issues one-period nominal bonds in every period t. Each unit of such bonds is sold for Qt units of money and pays one unit of money when it matures. Derive the equation that links the nominal interest rate to the real interest. rate and the inflation rate Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Finance

Authors: M. J. Alhabeeb

1st Edition

1118691512, 978-1118691519