Answered step by step

Verified Expert Solution

Question

1 Approved Answer

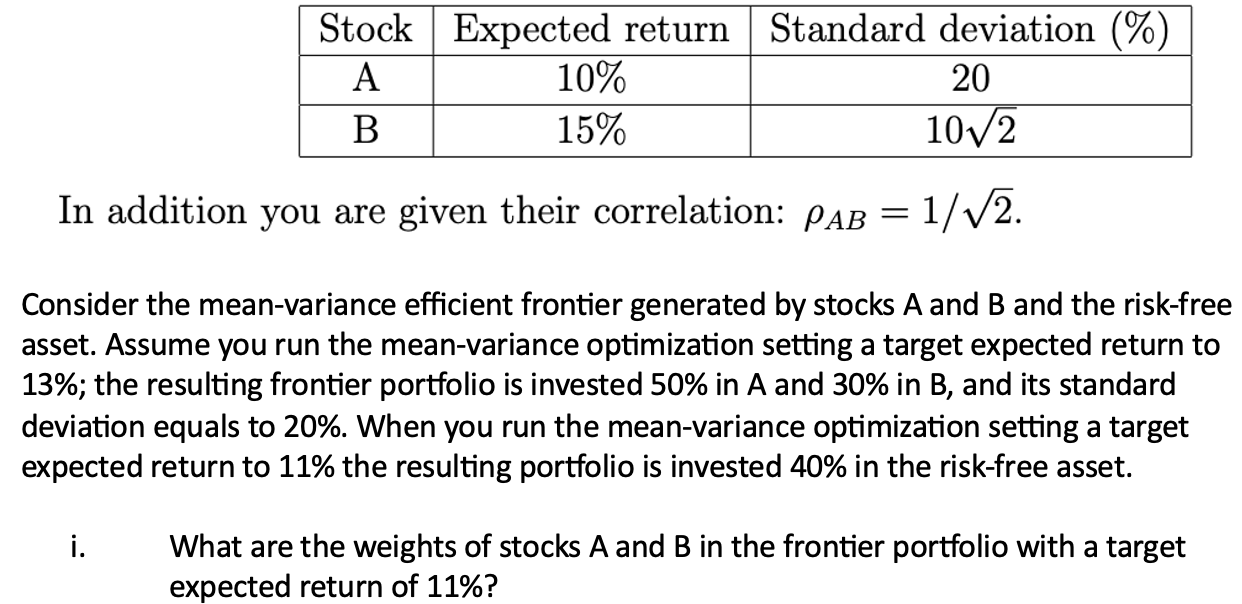

Stock Expected return Standard deviation (%) A B 10% 15% 20 102 In addition you are given their correlation: PAB = 1/2. Consider the

Stock Expected return Standard deviation (%) A B 10% 15% 20 102 In addition you are given their correlation: PAB = 1/2. Consider the mean-variance efficient frontier generated by stocks A and B and the risk-free asset. Assume you run the mean-variance optimization setting a target expected return to 13%; the resulting frontier portfolio is invested 50% in A and 30% in B, and its standard deviation equals to 20%. When you run the mean-variance optimization setting a target expected return to 11% the resulting portfolio is invested 40% in the risk-free asset. . What are the weights of stocks A and B in the frontier portfolio with a target expected return of 11%?

Step by Step Solution

★★★★★

3.41 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

To find the weights of stocks A and B in the frontier portfolio with a target expected return of 11 ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham

Concise 9th Edition

1305635937, 1305635930, 978-1305635937