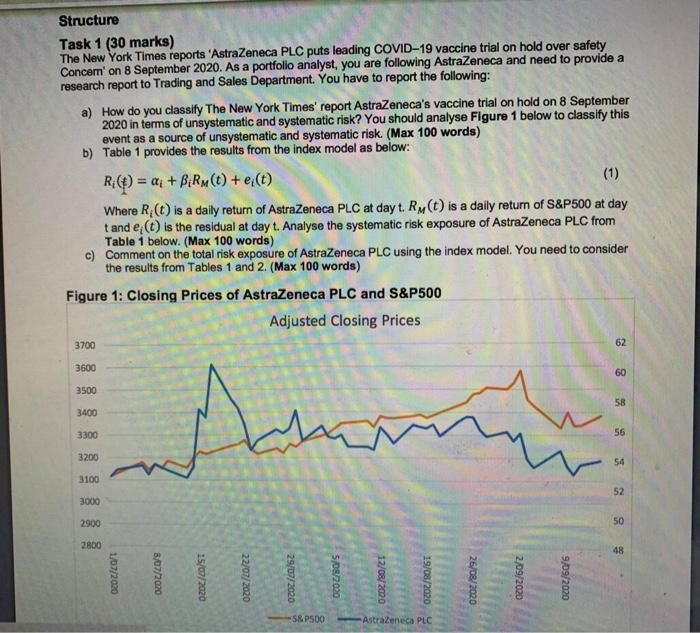

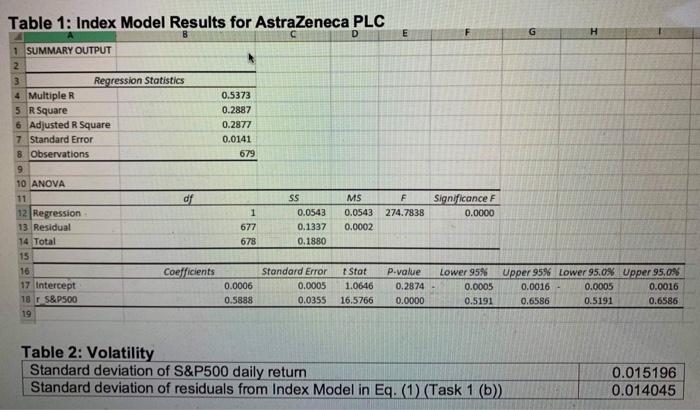

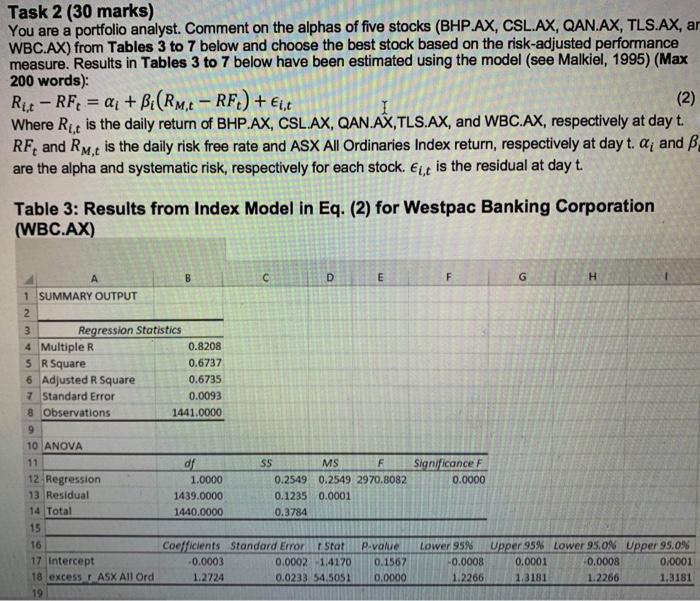

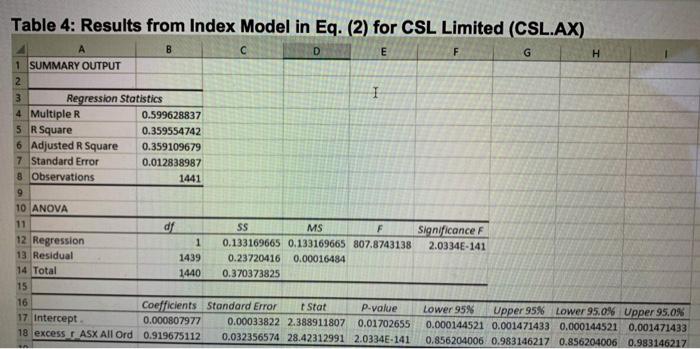

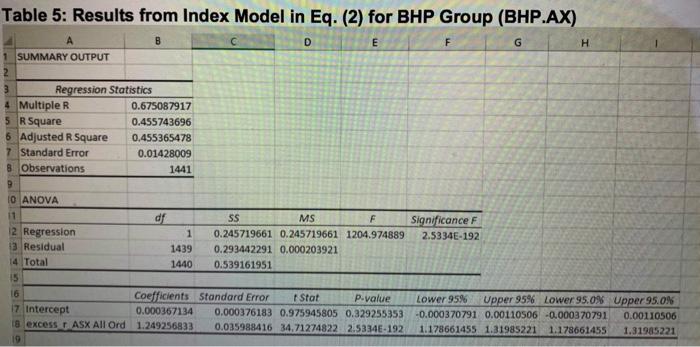

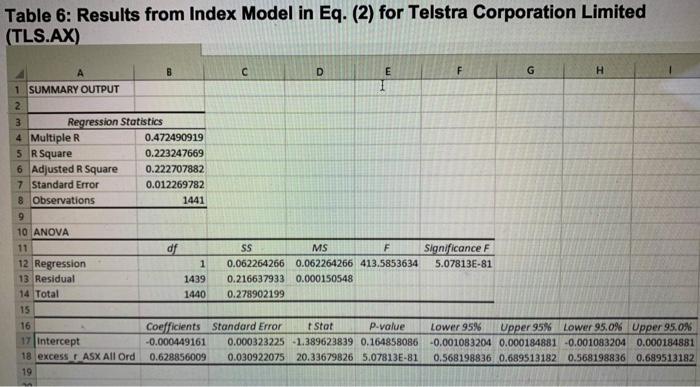

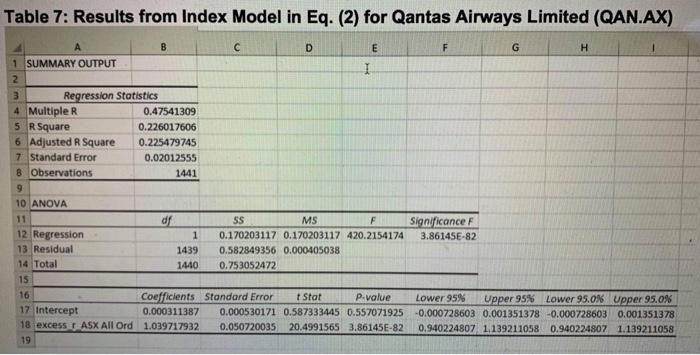

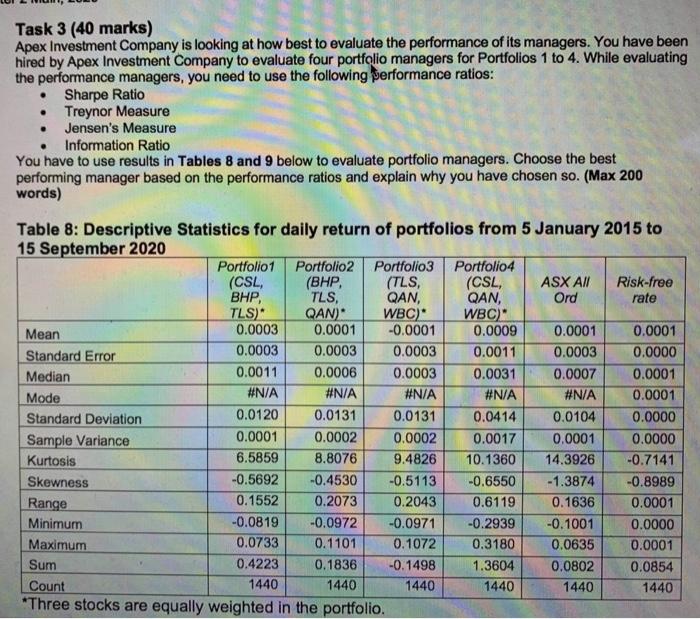

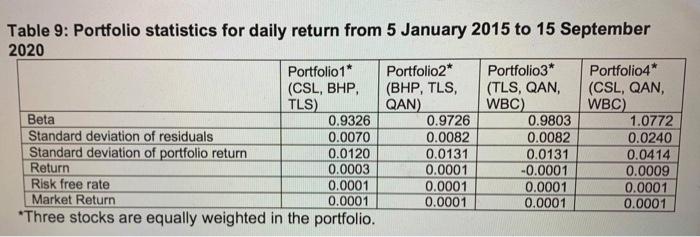

Structure Task 1 (30 marks) The New York Times reports AstraZeneca PLC puts leading COVID-19 vaccine trial on hold over safety Concer' on 8 September 2020. As a portfolio analyst, you are following AstraZeneca and need to provide a research report to Trading and Sales Department. You have to report the following: a) How do you classify The New York Times' report AstraZeneca's vaccine trial on hold on 8 September 2020 in terms of unsystematic and systematic risk? You should analyse Figure 1 below to classify this event as a source of unsystematic and systematic risk. (Max 100 words) b) Table 1 provides the results from the index model as below: RC) = ai + BiRu(t) + e(t) (1) Where R) is a daily return of AstraZeneca PLC at day t. Ry(t) is a daily return of S&P500 at day t and e(t) is the residual at day t. Analyse the systematic risk exposure of AstraZeneca PLC from Table 1 below. (Max 100 words) c) Comment on the total risk exposure of AstraZeneca PLC using the index model. You need to consider the results from Tables 1 and 2. (Max 100 words) Figure 1: Closing Prices of AstraZeneca PLC and S&P500 Adjusted Closing Prices 3700 62 3600 60 3500 58 3400 Amm 3300 56 3200 54 3100 52 3000 2900 50 2800 48 1/07/2020 8/07/2020 15/07/2020 22/07/2020 SRP500 AstraZeneca PLC Table 1: Index Model Results for AstraZeneca PLC E G H 1 SUMMARY OUTPUT 2 3 Regression Statistics 4. Multiple R 0.5373 5 R Square 0.2887 6 Adjusted R Square 0.2877 7 Standard Error 0.0141 8 Observations 679 9 10 ANOVA df SS 12 Regression 1 0.0543 13 Residual 677 0.1337 14 Total 678 0.1880 15 16 Coefficients Standard Error 17 Intercept 0.0006 0.0005 18 S&P500 0.5888 0.0355 19 F MS 0.0543 0.0002 Significance F 0.0000 274.7838 Stat 1.0646 16.5766 p.value 0.2874 0.0000 Lower 95% 0.0005 0.5191 Upper 95% Lower 95.0% Upper 95.0% 0.0016 0.0005 0.0016 0.6586 0.5191 0.6586 Table 2: Volatility Standard deviation of S&P500 daily return Standard deviation of residuals from Index Model in Eq. (1) (Task 1 (b)) 0.015196 0.014045 Task 2 (30 marks) You are a portfolio analyst. Comment on the alphas of five stocks (BHP.AX, CSL.AX, QAN.AX, TLS.AX, ar WBC.AX) from Tables 3 to 7 below and choose the best stock based on the risk-adjusted performance measure. Results in Tables 3 to 7 below have been estimated using the model (see Malkiel, 1995) (Max 200 words): Rit - RF, = ai + Bi(RM,t - RF.) +1.t (2) Where Ric is the daily return of BHP.AX, CSL.AX, QAN.AX,TLS.AX, and WBC.AX, respectively at day t. RF, and Rm, is the daily risk free rate and ASX All Ordinaries Index return, respectively at day t. a; and B. are the alpha and systematic risk, respectively for each stock. Ei,t is the residual at day t. store Table 3: Results from Index Model in Eq. (2) for Westpac Banking Corporation (WBC.AX) F G H C D E 1 SUMMARY OUTPUT 2 3 Regression Statistics 4 Multiple R 0.8208 5 R Square 0.6737 6 Adjusted R Square 0.6735 7 Standard Error 0.0093 8 Observations 1441.0000 9 10 ANOVA 11 df SS MS F 12 Regression 1.0000 0.2549 0.2549 2970.8082 13 Residual 1439.0000 0.1235 0.0001 14 Total 1440.0000 0.3784 15 16 Coefficients Standard Error Stat P.value 17 Intercept -0.0003 0.0002 1.4170 0.1567 18 excess ASX All Ord 1.2724 0.0233 54.5051 0.0000 19 Significance F 0.0000 Lower 95% Upper 95% Lower 95.0% Upper 95.0% -0.0008 0.0001 0.0008 0.0001 1.2266 1.3181 1.2266 1.3181 Table 4: Results from Index Model in Eq. (2) for CSL Limited (CSL.AX) F G H C D E 1 SUMMARY OUTPUT 2 1 3 Regression Statistics 4 Multiple R 0.599628837 5 R Square 0.359554742 6 Adjusted R Square 0.359109679 7 Standard Error 0.012838987 8 Observations 1441 9 10 ANOVA SS MS F 12 Regression 1 0.133169665 0.133169665 807.8743138 13 Residual 1439 0.23720416 0.00016484 14 Total 1440 0.370373825 15 16 Coefficients Standard Error Stat P-value 17 Intercept 0.000807977 0.00033822 2.388911807 0.01702655 18 excess ASX All Ord 0.919675112 0.032356574 28.42312991 2.0334E-141 Significance F 2.0334E-141 Lower 95% Upper 95% Lower 95.0% Upper 95.0% 0.000144521 0.001471433 0.000144521 0.001471433 0.856204006 0.983146217 0.856204006 0.983146217 Table 5: Results from Index Model in Eq. (2) for BHP Group (BHP.AX) D E G H 1 SUMMARY OUTPUT 2 3 Regression Statistics 4 Multiple R 0.675087917 5 RSquare 0.455743696 6 Adjusted R Square 0.455365478 7 Standard Error 0.01428009 8. Observations 1441 9 10 ANOVA 11 df SS MS F Significance F 2 Regression 1 0.245719661 0.245719661 1204.974889 2.5334E-192 13 Residual 1439 0.293442291 0.000203921 14 Total 1440 0.539161951 15 Coefficients Standard Error Stat p.value Lower 95% Upper 95% Lower 95.0% Upper 95.0% 17 Intercept 0.000367134 0.000376183 0.975945805 0.329255353 0.000370791 0.00110506 -0.0003 70791 0.00110506 18 excess ASX All Ord 1.249256833 0.035988416 34.71274822 2.5334E-192 1.178661455 1.31985221 1.178661455 1.31985221 19 Table 6: Results from Index Model in Eq. (2) for Telstra Corporation Limited (TLS.AX) D E F G H 1 SUMMARY OUTPUT 2 3 Regression Statistics 4 Multiple R 0.472490919 5 R Square 0.223247669 6 Adjusted R Square 0.222707882 7 Standard Error 0.012269782 8 Observations 1441 9 10 ANOVA 11 of SS MS F Significance F 12 Regression 1 0.062264266 0.062264266 413.5853634 5.07813E-81 13 Residual 1439 0.216637933 0.000150548 14 Total 1440 0.278902199 15 16 Coefficients Standard Error Stot P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0% 17 Intercept -0.000449161 0.000323225 -1.389623839 0.164858086 -0.001083204 0.000184881 -0.001083204 0.000184881 18 excess ASX All Ord 0.628856009 0.030922075 20.33679826 5.07813E-81 0.568198836 0.689513182 0.568198836 0.689513182 19 Table 7: Results from Index Model in Eq. (2) for Qantas Airways Limited (QAN.AX) F G H D E 1 SUMMARY OUTPUT I 2 Regression Statistics 4 MultipleR 0.47541309 5 RSquare 0.226017606 6 Adjusted R Square 0.225479745 7 Standard Error 0.02012555 8 Observations 1441 9 10 ANOVA 11 df SS MS F 12 Regression 1 0.170203117 0.170203117 420.2154174 13 Residual 1439 0.582849356 0.000405038 14 Total 1440 0.753052472 15 16 Coefficients Standard Error Stat P.value 17 Intercept 0.000311387 0.000530171 0.587333445 0.557071925 18 excess ASX All Ord 1.039717932 0.050720035 20.4991565 3.86145E-82 19 Significance F 3.86145E-82 Lower 95% Upper 95% Lower 95.0% upper 95.0% -0.000728603 0.001351378 -0.000728603 0.001351378 0.940224807 1.139211058 0.940224807 1.139211058 Task 3 (40 marks) Apex Investment Company is looking at how best to evaluate the performance of its managers. You have been hired by Apex Investment Company to evaluate four portfolio managers for Portfolios 1 to 4. While evaluating the performance managers, you need to use the following performance ratios: Sharpe Ratio Treynor Measure Jensen's Measure Information Ratio You have to use results in Tables 8 and 9 below to evaluate portfolio managers. Choose the best performing manager based on the performance ratios and explain why you have chosen so. (Max 200 words) Table 8: Descriptive Statistics for daily return of portfolios from 5 January 2015 to 15 September 2020 Portfolio1 Portfolio2 Portfolio 3 Portfolio 4 (CSL (BHP (TLS, (CSL ASX AII Risk-free BHP, TLS, QAN, QAN, Ord rate TLS) QAN): WBC) WBC) Mean 0.0003 0.0001 -0.0001 0.0009 0.0001 0.0001 Standard Error 0.0003 0.0003 0.0003 0.0011 0.0003 0.0000 Median 0.0011 0.0006 0.0003 0.0031 0.0007 0.0001 Mode #N/A #N/A #N/A #N/A #N/A 0.0001 Standard Deviation 0.0120 0.0131 0.0131 0.0414 0.0104 0.0000 Sample Variance 0.0001 0.0002 0.0002 0.0017 0.0001 0.0000 Kurtosis 6.5859 8.8076 9.4826 10.1360 14.3926 -0.7141 Skewness -0.5692 -0.4530 -0.5113 -0.6550 -1.3874 -0.8989 Range 0.1552 0.2073 0.2043 0.6119 0.1636 0.0001 Minimum -0.0819 -0.0972 -0.0971 -0.2939 -0.1001 0.0000 Maximum 0.0733 0.1101 0.1072 0.3180 0.0635 0.0001 Sum 0.4223 0.1836 -0.1498 1.3604 0.0802 0.0854 Count 1440 1440 1440 1440 1440 1440 *Three stocks are equally weighted in the portfolio. Table 9: Portfolio statistics for daily return from 5 January 2015 to 15 September 2020 Portfolio1" Portfolio 2* Portfolio3* Portfolio4* (CSL, BHP, (BHP, TLS, (TLS, QAN, (CSL, QAN, TLS) QAN) WBC) WBC) Beta 0.9326 0.9726 0.9803 1.0772 Standard deviation of residuals 0.0070 0.0082 0.0082 0.0240 Standard deviation of portfolio return 0.0120 0.0131 0.0131 0.0414 Return 0.0003 0.0001 -0.0001 0.0009 Risk free rate 0.0001 0.0001 0.0001 0.0001 Market Return 0.0001 0.0001 0.0001 0.0001 *Three stocks are equally weighted in the portfolio. Structure Task 1 (30 marks) The New York Times reports AstraZeneca PLC puts leading COVID-19 vaccine trial on hold over safety Concer' on 8 September 2020. As a portfolio analyst, you are following AstraZeneca and need to provide a research report to Trading and Sales Department. You have to report the following: a) How do you classify The New York Times' report AstraZeneca's vaccine trial on hold on 8 September 2020 in terms of unsystematic and systematic risk? You should analyse Figure 1 below to classify this event as a source of unsystematic and systematic risk. (Max 100 words) b) Table 1 provides the results from the index model as below: RC) = ai + BiRu(t) + e(t) (1) Where R) is a daily return of AstraZeneca PLC at day t. Ry(t) is a daily return of S&P500 at day t and e(t) is the residual at day t. Analyse the systematic risk exposure of AstraZeneca PLC from Table 1 below. (Max 100 words) c) Comment on the total risk exposure of AstraZeneca PLC using the index model. You need to consider the results from Tables 1 and 2. (Max 100 words) Figure 1: Closing Prices of AstraZeneca PLC and S&P500 Adjusted Closing Prices 3700 62 3600 60 3500 58 3400 Amm 3300 56 3200 54 3100 52 3000 2900 50 2800 48 1/07/2020 8/07/2020 15/07/2020 22/07/2020 SRP500 AstraZeneca PLC Table 1: Index Model Results for AstraZeneca PLC E G H 1 SUMMARY OUTPUT 2 3 Regression Statistics 4. Multiple R 0.5373 5 R Square 0.2887 6 Adjusted R Square 0.2877 7 Standard Error 0.0141 8 Observations 679 9 10 ANOVA df SS 12 Regression 1 0.0543 13 Residual 677 0.1337 14 Total 678 0.1880 15 16 Coefficients Standard Error 17 Intercept 0.0006 0.0005 18 S&P500 0.5888 0.0355 19 F MS 0.0543 0.0002 Significance F 0.0000 274.7838 Stat 1.0646 16.5766 p.value 0.2874 0.0000 Lower 95% 0.0005 0.5191 Upper 95% Lower 95.0% Upper 95.0% 0.0016 0.0005 0.0016 0.6586 0.5191 0.6586 Table 2: Volatility Standard deviation of S&P500 daily return Standard deviation of residuals from Index Model in Eq. (1) (Task 1 (b)) 0.015196 0.014045 Task 2 (30 marks) You are a portfolio analyst. Comment on the alphas of five stocks (BHP.AX, CSL.AX, QAN.AX, TLS.AX, ar WBC.AX) from Tables 3 to 7 below and choose the best stock based on the risk-adjusted performance measure. Results in Tables 3 to 7 below have been estimated using the model (see Malkiel, 1995) (Max 200 words): Rit - RF, = ai + Bi(RM,t - RF.) +1.t (2) Where Ric is the daily return of BHP.AX, CSL.AX, QAN.AX,TLS.AX, and WBC.AX, respectively at day t. RF, and Rm, is the daily risk free rate and ASX All Ordinaries Index return, respectively at day t. a; and B. are the alpha and systematic risk, respectively for each stock. Ei,t is the residual at day t. store Table 3: Results from Index Model in Eq. (2) for Westpac Banking Corporation (WBC.AX) F G H C D E 1 SUMMARY OUTPUT 2 3 Regression Statistics 4 Multiple R 0.8208 5 R Square 0.6737 6 Adjusted R Square 0.6735 7 Standard Error 0.0093 8 Observations 1441.0000 9 10 ANOVA 11 df SS MS F 12 Regression 1.0000 0.2549 0.2549 2970.8082 13 Residual 1439.0000 0.1235 0.0001 14 Total 1440.0000 0.3784 15 16 Coefficients Standard Error Stat P.value 17 Intercept -0.0003 0.0002 1.4170 0.1567 18 excess ASX All Ord 1.2724 0.0233 54.5051 0.0000 19 Significance F 0.0000 Lower 95% Upper 95% Lower 95.0% Upper 95.0% -0.0008 0.0001 0.0008 0.0001 1.2266 1.3181 1.2266 1.3181 Table 4: Results from Index Model in Eq. (2) for CSL Limited (CSL.AX) F G H C D E 1 SUMMARY OUTPUT 2 1 3 Regression Statistics 4 Multiple R 0.599628837 5 R Square 0.359554742 6 Adjusted R Square 0.359109679 7 Standard Error 0.012838987 8 Observations 1441 9 10 ANOVA SS MS F 12 Regression 1 0.133169665 0.133169665 807.8743138 13 Residual 1439 0.23720416 0.00016484 14 Total 1440 0.370373825 15 16 Coefficients Standard Error Stat P-value 17 Intercept 0.000807977 0.00033822 2.388911807 0.01702655 18 excess ASX All Ord 0.919675112 0.032356574 28.42312991 2.0334E-141 Significance F 2.0334E-141 Lower 95% Upper 95% Lower 95.0% Upper 95.0% 0.000144521 0.001471433 0.000144521 0.001471433 0.856204006 0.983146217 0.856204006 0.983146217 Table 5: Results from Index Model in Eq. (2) for BHP Group (BHP.AX) D E G H 1 SUMMARY OUTPUT 2 3 Regression Statistics 4 Multiple R 0.675087917 5 RSquare 0.455743696 6 Adjusted R Square 0.455365478 7 Standard Error 0.01428009 8. Observations 1441 9 10 ANOVA 11 df SS MS F Significance F 2 Regression 1 0.245719661 0.245719661 1204.974889 2.5334E-192 13 Residual 1439 0.293442291 0.000203921 14 Total 1440 0.539161951 15 Coefficients Standard Error Stat p.value Lower 95% Upper 95% Lower 95.0% Upper 95.0% 17 Intercept 0.000367134 0.000376183 0.975945805 0.329255353 0.000370791 0.00110506 -0.0003 70791 0.00110506 18 excess ASX All Ord 1.249256833 0.035988416 34.71274822 2.5334E-192 1.178661455 1.31985221 1.178661455 1.31985221 19 Table 6: Results from Index Model in Eq. (2) for Telstra Corporation Limited (TLS.AX) D E F G H 1 SUMMARY OUTPUT 2 3 Regression Statistics 4 Multiple R 0.472490919 5 R Square 0.223247669 6 Adjusted R Square 0.222707882 7 Standard Error 0.012269782 8 Observations 1441 9 10 ANOVA 11 of SS MS F Significance F 12 Regression 1 0.062264266 0.062264266 413.5853634 5.07813E-81 13 Residual 1439 0.216637933 0.000150548 14 Total 1440 0.278902199 15 16 Coefficients Standard Error Stot P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0% 17 Intercept -0.000449161 0.000323225 -1.389623839 0.164858086 -0.001083204 0.000184881 -0.001083204 0.000184881 18 excess ASX All Ord 0.628856009 0.030922075 20.33679826 5.07813E-81 0.568198836 0.689513182 0.568198836 0.689513182 19 Table 7: Results from Index Model in Eq. (2) for Qantas Airways Limited (QAN.AX) F G H D E 1 SUMMARY OUTPUT I 2 Regression Statistics 4 MultipleR 0.47541309 5 RSquare 0.226017606 6 Adjusted R Square 0.225479745 7 Standard Error 0.02012555 8 Observations 1441 9 10 ANOVA 11 df SS MS F 12 Regression 1 0.170203117 0.170203117 420.2154174 13 Residual 1439 0.582849356 0.000405038 14 Total 1440 0.753052472 15 16 Coefficients Standard Error Stat P.value 17 Intercept 0.000311387 0.000530171 0.587333445 0.557071925 18 excess ASX All Ord 1.039717932 0.050720035 20.4991565 3.86145E-82 19 Significance F 3.86145E-82 Lower 95% Upper 95% Lower 95.0% upper 95.0% -0.000728603 0.001351378 -0.000728603 0.001351378 0.940224807 1.139211058 0.940224807 1.139211058 Task 3 (40 marks) Apex Investment Company is looking at how best to evaluate the performance of its managers. You have been hired by Apex Investment Company to evaluate four portfolio managers for Portfolios 1 to 4. While evaluating the performance managers, you need to use the following performance ratios: Sharpe Ratio Treynor Measure Jensen's Measure Information Ratio You have to use results in Tables 8 and 9 below to evaluate portfolio managers. Choose the best performing manager based on the performance ratios and explain why you have chosen so. (Max 200 words) Table 8: Descriptive Statistics for daily return of portfolios from 5 January 2015 to 15 September 2020 Portfolio1 Portfolio2 Portfolio 3 Portfolio 4 (CSL (BHP (TLS, (CSL ASX AII Risk-free BHP, TLS, QAN, QAN, Ord rate TLS) QAN): WBC) WBC) Mean 0.0003 0.0001 -0.0001 0.0009 0.0001 0.0001 Standard Error 0.0003 0.0003 0.0003 0.0011 0.0003 0.0000 Median 0.0011 0.0006 0.0003 0.0031 0.0007 0.0001 Mode #N/A #N/A #N/A #N/A #N/A 0.0001 Standard Deviation 0.0120 0.0131 0.0131 0.0414 0.0104 0.0000 Sample Variance 0.0001 0.0002 0.0002 0.0017 0.0001 0.0000 Kurtosis 6.5859 8.8076 9.4826 10.1360 14.3926 -0.7141 Skewness -0.5692 -0.4530 -0.5113 -0.6550 -1.3874 -0.8989 Range 0.1552 0.2073 0.2043 0.6119 0.1636 0.0001 Minimum -0.0819 -0.0972 -0.0971 -0.2939 -0.1001 0.0000 Maximum 0.0733 0.1101 0.1072 0.3180 0.0635 0.0001 Sum 0.4223 0.1836 -0.1498 1.3604 0.0802 0.0854 Count 1440 1440 1440 1440 1440 1440 *Three stocks are equally weighted in the portfolio. Table 9: Portfolio statistics for daily return from 5 January 2015 to 15 September 2020 Portfolio1" Portfolio 2* Portfolio3* Portfolio4* (CSL, BHP, (BHP, TLS, (TLS, QAN, (CSL, QAN, TLS) QAN) WBC) WBC) Beta 0.9326 0.9726 0.9803 1.0772 Standard deviation of residuals 0.0070 0.0082 0.0082 0.0240 Standard deviation of portfolio return 0.0120 0.0131 0.0131 0.0414 Return 0.0003 0.0001 -0.0001 0.0009 Risk free rate 0.0001 0.0001 0.0001 0.0001 Market Return 0.0001 0.0001 0.0001 0.0001 *Three stocks are equally weighted in the portfolio