Question: summarize and raise outstanding issues about managerial accounting in the article Accounting Information for Product Costing - Case Study Suzana Keglevi Kozjak, Tanja estanj-Peri Faculty

summarize and raise outstanding issues about managerial accounting in the article

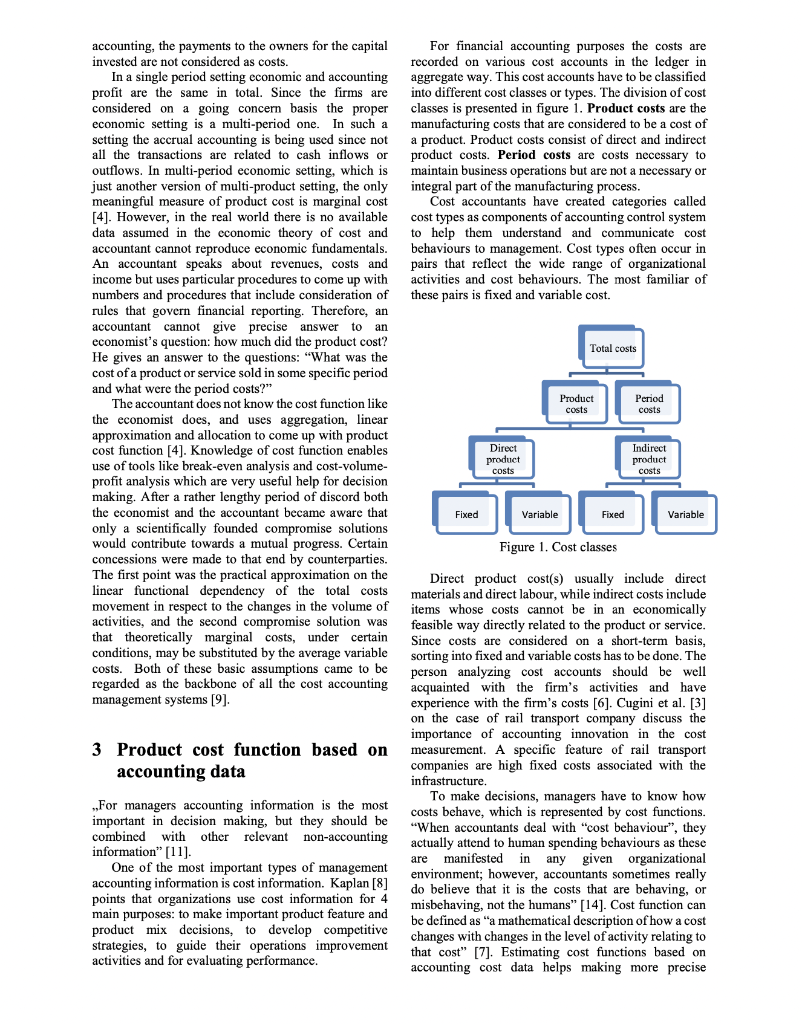

Accounting Information for Product Costing - Case Study Suzana Keglevi Kozjak, Tanja estanj-Peri Faculty of Organization and Informatics University of Zagreb Pavlinska 2, 42000 Varadin, Croatia (skozjak, tperic} @foi.hr showed that majority (84 %) of responding companies. used the same rules and procedures for external and internal reporting purposes. Abstract. Cost management is a process that requires continuous improvement of managers' knowledge. There is economic theory of costs and revenues. However, in practice managers rely on accounting data in making business decisions. The main problem is that economists and accountants do not see the costs the same way. ** dow In this paper we explain the difference between the teachings of economic theory and its practical application in the accounting practices. We show how economic theory can be applied in practice and be a useful tool in the hands of managers. For the case study we use recent accounting data of a transport company. In this paper we start with the economic theory of cost and investigate how economic theory is related to an accountant's approach to product costing. The main research question is: how could accountants in the observed firm use mathematical procedures to come closer to economic cost function which enables improved decision making? In answering the research question we consider two methods: account analysis method and simple regression analysis method. The topic of estimating cost functions is widely elaborated in textbooks yet there difficult to find case studies the relevant journals. The probable reason: that firms. are reluctant to give internal information about their costs. Our paper contributes to the literature since to the best of our knowledge there are no recent case studies available regarding this topic. The topic is especially interesting for countries like Croatia where management accounting practices in firms are less. developed. amcat to Keywords: product costing, accounting, decision making 1 Introduction 2 Economics vs. accounting Accounting is divided into financial and management accounting, where primary goal of financial accounting is producing information for investors and other interested external parties while the goal of management accounting is to produce information for internal purposes, supporting decision making and management control. Managers use information to find out: 1) how much some product or service would cost and 2) to control if something did cost too much. Between financial and managerial accounting there is the some number differences, even though they often rely on the same underlying financial data [10]. Managerial accounting has has a strong future orientation, in contrast to financial accounting which primarily summarizes wan Terms like revenues, costs, income or profit used in accounting originate in economics. In an economist's. world production function of a firm explains the functional relationship between the resources or factor inputs and quantity of output firm produces using production technology. Economists use production function and assumptions about factor and output market prices to get the answers about economic revenues, economic costs, economic income and profit and to come up with the decision how much to produce. It is not necessary to specify the cost function to arrive to the answer but framing the problem in terms of revenues and costs results in the well known condition for optimality of profit maximization problem: marginal revenues should be equal to marginal costs [4]. s not of On the past financial transactions. Financial accounting data should be objective, verifiable and prepared in accordance with rive, with a common set ground rules. On the other hand, managerial accounting should be flexible to provide hotation enough to provide whatever data are relevant for particular decision. Managers set their own rules concerning the content and form of internal reports. Managerial accounting is not mandatory; a manager is completely free to do as much or as little as he wishes. Research that is carried out in this paper is related to the managerial accounting. The research in UK [5] An economist and an accountant do not see the costs the same way. The economist's view of costs includes payments to all factors of production, which are usually simply divided into capital and labour. In Varadin, Croatia September 23-25, 2015 Faculty of Organization and Informatics accounting, the payments to the owners for the capital invested are not considered as costs. In a single period setting economic and accounting profit are the same in total. Since the firms are considered on a going concern basis the proper economic setting is a multi-period one. In such a my setting setting the accrual accounting is being used since not all the transactions are related to cash inflows or outflows. In multi-period economic setting, which is in th www just another version of multi-product setting, the only meaningful measure of product cost is marginal cost [4]. However, in the real world there is no available data assumed in the economic theory of cost and accountant cannot reproduce economic fundamentals. An accountant speaks about revenues, costs and income but uses particular procedures to come up with numbers and procedures that include consideration of rules that govern financial reporting. Therefore, an accountant cannot give precise answer to an economist's question: how much did the product cost? He gives an answer to the questions: "What was the cost of a product or service sold in some specific period and what were the period costs?" The accountant does not know the cost function like the economist does, and uses aggregation, linear approximation and allocation to come up with product cost function [4]. Knowledge of cost function enables use of tools like break-even analysis and cost-volume- ume profit analysis which are very useful help for decision making. After rather lengthy period of discord both And Dou the economist and the accountant became aware that www only a scientifically founded compromise solutions would contributo www.w would contribute towards mutual progress. Certain concessions were made to that end by counterparties. The first point was the practical approximation on the linear functional dependency of the total costs movement in respect to the changes in the volume of activities, and the second compromise solution was that theoretically marginal costs, under certain conditions, may be substituted by the average variable costs. Both of these basic assumptions came regarded as the backbone of all the cost accounting management systems [9]. be 3 Product cost function based on accounting data ,,For managers accounting information is the most important in decision making, but they should be combined with other relevant non-accounting information" [11]. One of the most important types of management accounting information is cost information. Kaplan [8] points that organizations use cost information for main purposes: to make important product feature and product mix decisions, to develop competitive strategies, to guide their operations improvement activities and for evaluating performance. For financial accounting purposes the costs are recorded on various cost accounts in the ledger in aggregate way. This cost accounts have to be classified into different cost classes or types. The division of cost classes is presented in figure 1. Product costs are the manufacturing costs that are considered to be a cost of a product. Product costs consist of direct and indirect product costs. Period costs are costs necessary to maintain business operations but are not a necessary or integral part of the manufacturing process. maintain www Cost accountants have created categories called cost types as components of accounting control system to help them understand and communicate cost behaviours to management. Cost types often occur in pairs that reflect the wide range of organizational activities and cost behaviours. The most familiar of these pairs is fixed and variable cost. Total costs Direct product costs Product costs Period costs Indirect product costs Fixed Variable Fixed Variable Figure 1. Cost classes Direct product cost(s) usually include direct materials and direct labour, while indirect costs include items whose costs cannot be in an economically feasible way directly related to the product or service. Since costs are considered on a short-term basis, sorting into fixed and variable costs has to be done. The www. person analyzing cost accounts should be well acquainted with the firm's activities and have experience with the firm's costs [6]. Cugini et al. [3] on the case of rail transport company discuss the importance of accounting innovation in the cost measurement. A specific feature of rail transport companies are high fixed costs associated with the infrastructure. To make decisions, managers have to know how costs behave, which is represented by cost functions. "When accountants deal with "cost behaviour", they actually attend to human spending behaviours as these are manifested in any given organizational envi ment; however, accountants hetimes really do believe that it is the costs that are behaving, or misbehaving, not the humans" [14]. Cost function can be defined as "a mathematical description of how a cost changes with changes in the level of activity relating t that cost" [7]. Estimating cost functions based on accounting cost data helps making more precise predictions about future costs and therefore facilitates decision making. The method is called Account Analysis Method [7]. Accounting data serve as the basis for Regression Analysis Method where dependent variable is some cost variable. The independent variable(s) is (are) cost driver(s). As Roma'n [13] indicates in his case study of Continental Airlines, regression analysis is a useful tool for understanding cost behaviour and predicting future costs. In his paper Stout [15] emphasizes the importance of extensive coverage of material related to the cost-estimation process including regression analysis in accounting education. "The application of mathematical and statistical methods in the analysis of costs is significant background in management decision making [12]. Radman-Funari and Babler [12] in their paper perform the ordinary least squares method to determine the relationship between total costs and quantity produced. Estimation of cost functions usually is based on two assumptions [1]: total costs of a cost-object vary because of variations in a single cost driver, . cost behaviour is approximated by a linear cost function. These assumptions will be applied on our case study. Since we look at the firm as a whole and the firm operates in road transportation of goods, the only cost object is service of transportation and the single cost driver we use are kilometres done on the firm level. First, we will apply account analysis method and then regression analysis. 4 Case study Account analysis method is done for the case of a medium size transport company from Croatia. The cost accounts summarize data by classes of costs. Total capacity of a firm is constrained by the number of vehicles. Costs accounts are divided into fixed and and variable. Variable cost accounts are: fuel, toll and parking fees, daily allowances for drivers, freight costs, costs of phytopathologist and veterinarians, vehicles maintenance costs and costs of tyres. All of these costs are direct costs since they are directly related to the main business activity of the firm. Fixed cost accounts are: salaries of drivers, salaries of other personnel, amortization of vehicles, amortization of other fixed assets, insurance of vehicles, insurance of other assets, rent costs for vehicles, communication costs, office supplies and marketing costs. Salaries of other personnel, amortization of other fixed assets, insurance of other assets, office supplies and marketing costs are indirect period costs, all the other are product costs. Costs were recorded for a period of one year, month by month. In Table 1, variable, fixed and total costs of the transport company for the period from January to December are shown. Table 1. Costs by months VC FC TC Month kn January kn 1.071.738 1.187.699 1.047.169 2.118.906 1.104.946 2.292.645 February March 1.303.370 1.150.294 2.453.665 April 1.213.245 2.585.248 May 1.139.279 2.627.838 June 9 kilometres 277.525 299.296 333.374 363.329 390.542 380.647 378 789 350.796 430 443 420.537 384.885 427.927 2.009.276 383.539 1.733.979 4.391.186 18.454.134 14.077.645 1.124.453 7.604-747 2,694 742 1.372.002 1.488.558 1.570 289 1.595.673 1.545.412 1.851.441 July 1.110,492 2.706.165 1.105,125 2.650537 1.169,704 KANSLIE 3,021.145 August September October November 1.724.697 1.166406 2.891.103 1.207.587 3.216.864 1.538.944 3.272.923 December Total 32.531.779 Total revenues in the base year were 30.314.804 kn so the firm realized operating loss in the amount of 2.216.975 kn. The firm used the data presented in table 1 as a management report that should have served for management control purposes. However, such report cannot serve for planning or control purposes since it is based only on financial accounting convention for recording revenues or costs. The only divergence from pure financial accounting significance of this numbers is the separation into fixed and variable costs. In order to serve for management control purposes, these numbers should be, for example used to estimate cost function. Indirect period costs can be included in estimation (in 4.1), but further analysis can be done focusing only on product costs (in 4.2). 4.1. Estimating cost function I The simplest, yet useful thing to do would be to calculate monthly cost function based on unit variable cost and monthly fixed cost taking into account all costs that were recorded. The unit variable cost is 4,2025 kn/km, and average fixed cost is 1.173.137 kn per month. Therefore, estimated monthly total cost function is: TC 1.173.137+4,2025-Q (1) If we assume that structure of costs will remain stable in the next period we can use break-even and cost-volume-profit analysis as a useful tool for planning purposes. Based on estimated data we can easily determine the break-even point. Break-even. point (BE) shows the level of activity where revenues equal expenses, and can be calculated as follows: FC BE= p-v (2) where p is the unit price, and v is the unit variable cost. In our example price per kilometre in previous year was 6,9 kn, and BE quantity is 434.898 km. From Table 1, it can be seen that in the base year the company did not realize kilometers to break-even in a single months. If, when planning for new period, we assume that with present business model the BE kilometers cannot be achieved, the major business restructuring is necessary. Operations that generate loss in the long run inevitably lead to bankruptcy. Second analysis is cost-volume-profit analysis. It is necessary to consider whether the price is well set. If there is a possibility, the firm should raise the price per kilometre and see the impact on the break-even point. Before the decision to increase the prices it is important to conduct a market analysis to determine prices of competitors. If the price rises by 0,32 kn/km (about 5%) to 7,22 kn/km (assumed that the price increase will not significantly affect the demand), and the costs remain the same, then BE quantity lowers to 388.788 km per month. BE quantity decreased from the initial equilibrium quantity by approximately 10%. However, how that three mar the table 1 shows that only in three months in previous period (May, September and November), kilometers which would achieve the break-even point were realized. Even with the price increase of 5% the company will not have profit on a yearly basis in the next period if the costs are not reduced. 4.2. Estimating cost function II When estimating cost function, focus can be on product costs. All variable costs in our case are considered. product costs. Since fixed costs in our case consist of product and indirect period costs, we subtracted period costs in calculations. Revised cost data are shown in Table 2. Table 2. Costs by months - revised Q Product Indirect fixed costs (period) Month kilometres (kn) fixed costs VC kn kn kn January 277.525 576.085 471.084 1.071.738 1.647.823 2.118.906 February 299 296 644.929 459.918 1.187.699 1.832.628 2.292.545 March 333.374 631.034 519.361 1.303.370 1.934.404 1.934.404 2.453.765 363.329 658.635 April 554.610 1.372.002 2.030.637 2.585.248 May 390.542 652.618 486.662 1.488.558 2.141.176 2.627.838 June 380.647 605.867 518.586 1.570,289 2.176.156 2.694.742 July 378.789 616,834 493.658 1.595.673 2.212.507 2.706.165 Augest 350.796 654.293 450.832 1.545.412 2.199.705 2.650,537 September 420.537 696.518 473.186 1.851.441 2.547.959 3.021.145 673.018 493.388 1.724.697 2.397.715 2.891.103 November 427.927 713.272 494.315 2.009.276 2.722.548 3.216.864 December 383.539 804.079 734.865 1.733.979 2.538.058 3.272.923 Total 4.391.186 7.927.181 6.150.464 18.454.134 26.381.316 32.531.779 October 384.885 The unit variable cost is again 4,2025 kn/km, and average fixed product cost is 660.598 kn per month. Therefore, estimated monthly total product cost function is: TC = 660.598+4,2025-Q (3) BE quantity now is 244.893 km per month. This was achieved in every month of base period. In average, 365.932 km per month were realized in base period. If we assume that in the next period we can count on that number of km on average, every km above 244.893 contributes to the coverage of indirect (period) fixed costs. With average price of 6,9 kn/km, maximal monthly amount of indirect fixed costs could be IFC = (6,9kn/km - 4,2025 kn/km) 121.039 km (4) which is 326.503 kn monthly. Comparing it with the base year where indirect fixed costs were 512.539 kn monthly, we can see that significant lowering of costs should be done on a monthly basis. 4.3. Possibilities for further analysis We used revised cost data (table 2) and data from table 3 prepared on a monthly basis for regression analysis. Total product costs are the same in tables 2 and 3, but difference is in monthly total costs. In table 3 annual indirect costs were allocated to each month based on kilometers done in that month. Table 3. Costs by months - IFC allocated based on km Product Indirect 0 fixed costs (period) kilometres fixed costs (kn) Total product Total costs VC Month kn kn kn kn January 277.525 576.085 388.712 1.071.738 1.647.823 2.036.535 February 299,296 644.929 419.205 1.187.699 1.832.628 1.832.628 2.251.833 March 333.374 631.034 466.936 1.303.370 1.934.404 2.401-341 April 363.329 658.635 508.893 1.372.002 2.030.637 2.539 530 May 390.542 652.618 547.008 1.488.558 2.141.176 2.688.184 Jane 380.647 605.867 533.149 1.570.289 2.176.156 2.709 305 July 378.789 616.834 530.546 1.595.673 2.212.507 2.743.054 August 350.796 654.293 491.338 1.545.412 2.199.705 2.691.043 September 420,537 696 518 589,020 1.851.441 2.547.959 3.136.979 October 384.885 673.018 539,085 1.724.697 2.397.715 2.936.799 November 427.927 713.272 599.371 2.009.276 2.722.548 3.321.919 December 383.539 804.079 537.199 1.733.979 2.538.058 3.075.257 Total Total 4.391.186 7.927.181 6.150.464 18.454.134 26.381.316 32.531.780 product costs Total costs In all regressions dependent variable was total costs (regressions 1 and 3) or total product costs (regression 2). The independent variable is the cost driver, where one or more cost drivers can be used based on what we distinguish simple and multiple regressions [2]. In our simple regression analysis independent variable was always quantity of kilometers. Results of regressions are presented in table 4 and statistics in table 5. Regressions line fit plots are shown in Figures 2, 3 and 4. Table 4. Results of regressions Standard P-value 0,54 5,71 Coefficients Error t Stat 234.724,81 436.891,88 6,77 1,19 -157.306,78 330.765,42 0,90 -157.306,78 330.765,42 7,84 0,90 -0,48 7,17 -0,48 8,73 Regression Regression 2 Regression 3 Intercept Q Intercept Q Intercept Q 0,60 0,00 0,64 0.00 0,64 0,00 Table 5. Regression statistics Regression Regression 2 Regression Statistics Multiple R R Square Adjusted R Square Standard Error Observations 3.500 3.000 2.500 2.000 1.500 I 0,874681714 0,7650681 0,74157491 176019,6683 12 27628 2.585 2.45 2119 250 270 290 310 330 350 370 390 410 430 450 Thousands TC-Predicted TC Figure 2. Regression 1 - Total costs include monthly indirect fixed costs. 3.000 r 2.723 2.500 2.538 2715 2.2002 2.031 2141 2.000 1645 1.500 250 270 290 310 330 350 370 390 410 430 450 Thousands TPC-Predicted TPC Figure 3. Regression 2 - Total product costs 3.500 3.322 3.000 3.075 295 2007 2349688 2540 2.500 2.401 +252 2.000 2037 1.500 250 270 290 310 330 350 370 390 410 430 450 Thousands TC-Predicted TC Figure 4. Regression 3 - Total costs include indirect fixed costs allocated using km as allocation base R is highest for regression 3, meaning that allocating indirect fixed cost based on km to each month proved useful. T-values for independent variable are higher than 2 in all the regression, with the highest value of t again for regression 3. P-values for independent variable are nearly 0 in all the regression. Significance- F values are lower than 0,05 in all regressions. All of these prove statistical reliability of regressions. The best fit is regression no. 3. M 0,91497913 0,837186808 0.820905489 133262,3069 12 1913 1.9384 Regression 3 0,940228541 0.88402971 0,872432681 133262,3069 12 3.217 3,023 137 The total cost function defined as -153.306,78+7,84-Q (5) can be used for prediction of total costs in the future. Since this formula is the result of regression, the intercept should not be mistaken for fixed costs, like in linear cost functions estimated using account analysis method. Out Our research was limited by the available data. Separate cost functions could be determined for different cost classes. Not every cost class is best determined by the only cost driver considered here, which were kilometres done. For example, the best cost driver for phytosanitary costs is the number of jobs that included need for such an expert. Cost system of a company could measure costs without significant investment more reliably- jobs could be differentiated into domestic, international, those that include special certificates or not etc. Of course the company did not charge the same price for every job, but more precise measuring of costs leads to better pricing decisions. 5 Conclusion In this paper we show that there is a possibility to apply some parts of economic theory for management control purposes. We took a road transport company for our case study. Their cost accounting data are used to calculate cost functions that can be utilized for prediction of future costs and pricing decisions. We de costa firstly applied linear approximation to come up with total cost function. Additionally we applied simple regression. Although limited by available data our case how study shows how useful the application of economic theory in practice can be. With more detailed cost data the results can be significantly more valuable for internal decision making process. References [1] Bhimani, A., Horngren C.T., Datar S.M., Foster G. Management and Cost Accounting. Pearson Education Limited, Harlow, England, 2008. [2] Blocher, E.J., Stout, D.E., Cokins, G., Chen, K.H. Cost Management. McGraw-Hill Irwin, New York, USA, 2008. [3] Cugini, A., Michelon, G., Pilonato, S. Innovating cost accounting practices in rail transport companies, Journal of Applied Accounting Research, Vol. 14 Iss: 2, pp. 147-164, 2013. [4] Demski, J.S. Managerial Uses of Accounting Information. Springer, New York, USA, 2008

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts