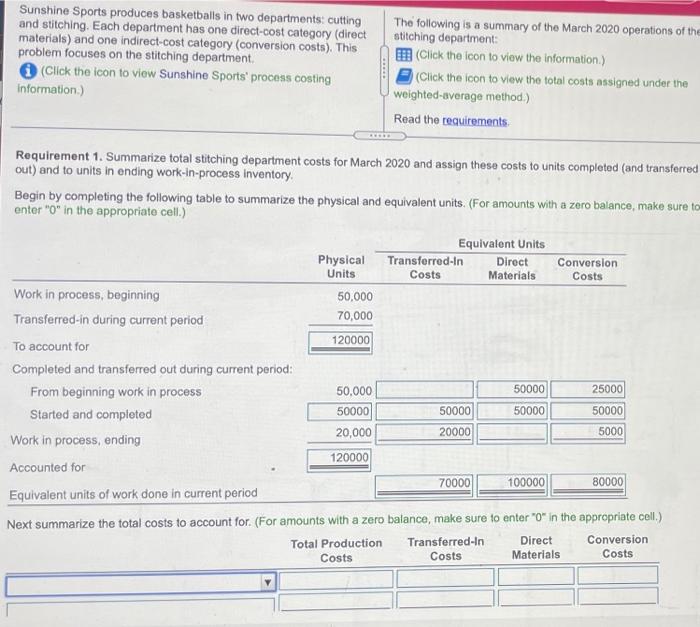

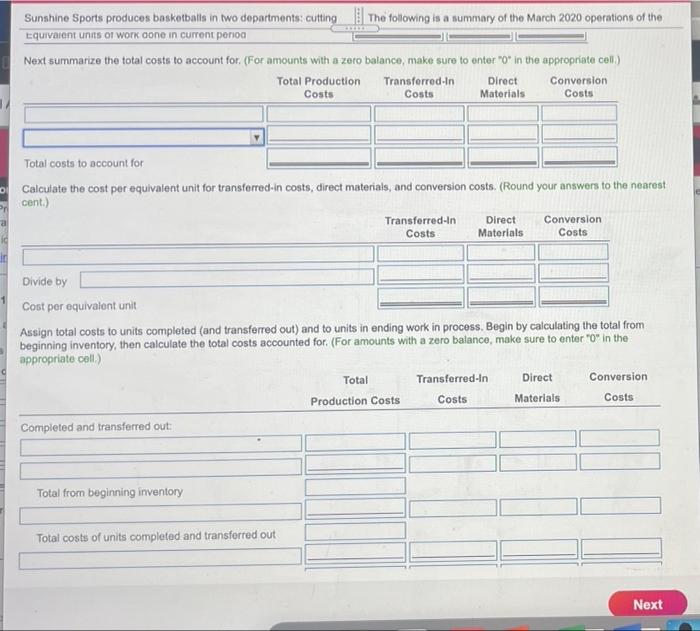

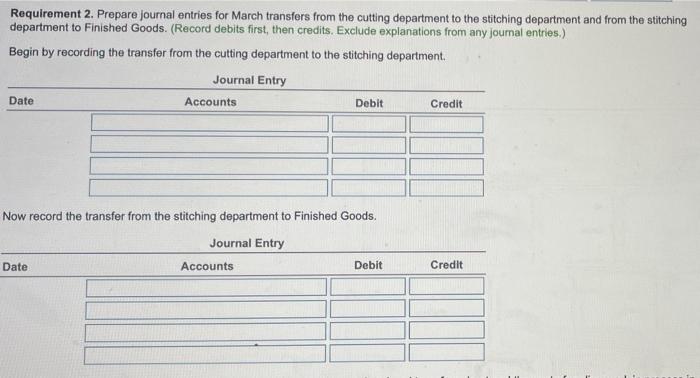

Sunshine Sports produces basketballs in two departments: cutting and stitching. Each department has one direct-cost category (direct materials) and one indirect-cost category (conversion costs). This problem focuses on the stitching department. (Click the icon to view Sunshine Sports process costing Information) The following is a summary of the March 2020 operations of the stitching department: (Click the icon to view the information) (Click the icon to view the total costs assigned under the weighted-average method.) Read the requirements Requirement 1. Summarize total stitching department costs for March 2020 and assign these costs to units completed (and transferred out) and to units in ending work-in-process inventory Begin by completing the following table to summarize the physical and equivalent units. (For amounts with a zero balance, make sure to enter "o" in the appropriate cell.) Equivalent Units Physical Transferred in Direct Conversion Units Costs Materials Costs Work in process, beginning 50,000 Transferred-in during current period 70,000 To account for 120000 Completed and transferred out during current period: From beginning work in process 50,000 50000 25000 Started and completed 50000 50000 50000 50000 20,000 20000 5000 Work in process, ending 120000 Accounted for 70000 100000 80000 Equivalent units of work done in current period Next summarize the total costs to account for. (For amounts with a zero balance, make sure to enter "o" in the appropriate cell.) Total Production Transferred-In Direct Conversion Costs Costs Materials Costs Sunshine Sports produces basketballs in two departments: cutting the following is a summary of the March 2020 operations of the Equivalent units of work done in current perioa Next summarize the total costs to account for. (For amounts with a zero balance, make sure to enter "O" in the appropriate cell) Total Production Transferred-In Direct Conversion Materials Costs Costs Costs D Total costs to account for Calculate the cost per equivalent unit for transferred-in costs, direct materials, and conversion costs. (Round your answers to the nearest cent.) Transferred-In Direct Conversion Costs Materials Costs Divide by Cost per equivalent unit Assign total costs to units completed (and transferred out) and to units in ending work in process. Begin by calculating the total from beginning inventory, then calculate the total costs accounted for. (For amounts with a zero balance, make sure to enter "o" in the appropriate coll.) Total Transferred in Direct Conversion Production Costs Costs Materials Costs Completed and transferred out Total from beginning inventory Total costs of units completed and transferred out Next Requirement 2. Prepare journal entries for March transfers from the cutting department to the stitching department and from the stitching department to Finished Goods. (Record debits first, then credits. Exclude explanations from any journal entries.). Begin by recording the transfer from the cutting department to the stitching department Journal Entry Date Accounts Debit Credit Now record the transfer from the stitching department to Finished Goods. Journal Entry Accounts Date Debit Credit . Total from beginning inventory Total costs of units completed and transferred out Total costs accounted for Requirement 2. Prepare journal entries for March transfers from the cutting departmentt department to Finished Goods. (Record debits first, then credits. Exclude explanations fro Begin by recording the transfer from the cutting department to the stitching department Journal Entry Date Accounts Debit Credi Conversion Costs Now record the t Direct Materials ad Goods. Finished Goods Date Debit Credit Work in ProcessCutting Work in ProcessStitching Completed and transferred out: Costs added to beginning WIP in current period Started and completed Work in process, beginning Work in process, ending e cutting depart Lupurumowrunon vuo. UVUT WURO ICH VUUR. Laclude explanati Begin by recording the transfer from the cutting department to the stitching departn non con co Data table hod) A D 1 Physical Units (basketball) 50,000 D Transferred in Direct Conversion Costa Materials Costs $ 80.000 $ ols 24,000 100% 0% 50% 2. Beginning work in process, March 1 3 Degree of completion, beginning work in process 4. Transferred in during March 2020 5 Completed and transferred out during March 2020 Ending work in process, March 31 7 Degree of completion, anding work in process Total costs added during March 70,000 100,000 20.000 ved out make sur 100% 0% 40,000 $ 25% 60,000 5 210,000 - X Weighted average assignment of costs ut Total Transferred In Direct Conversion Production Costs Costs Materials Costs Assignment of costs Completed and transferred out $ 345,000 $ 225,000 $ 40,000 $ 30,000 49.000 45,000 0 4,000 Ending work in process $ 394,000 $ 270,000 $ 40,000 $ 84,000 Total costs to account for or any jour ansfer og operu artment to the stitching departe try Debit - X More info After cutting, basketballs are immediately transferred to the stitching department, Direct material is added when the stitching process is 85% complete Conversion costs are added evenly during stitching operations. After stitching is completed, basketballs are immediately transferred to Finished Goods. Sunshine Sports uses the FIFO method of process costing Eto Finished Goods