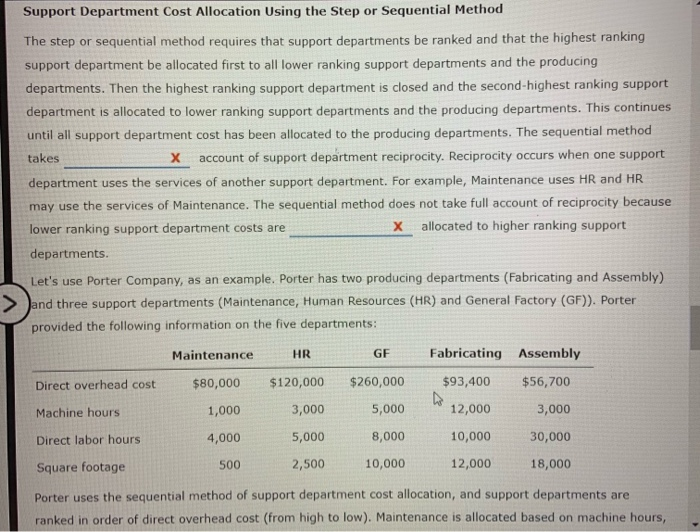

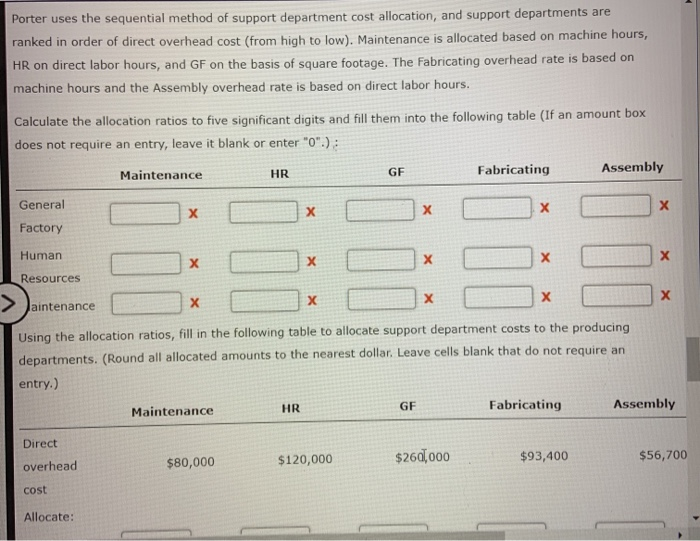

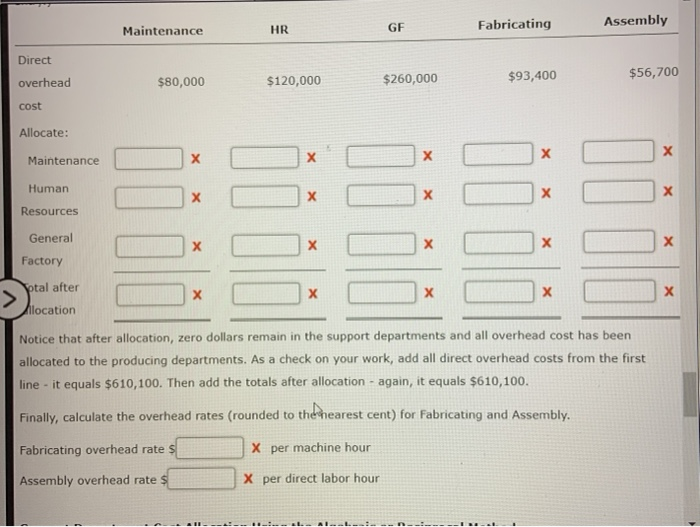

Support Department Cost Allocation Using the Step or Sequential Method The step or sequential method requires that support departments be ranked and that the highest ranking support department be allocated first to all lower ranking support departments and the producing departments. Then the highest ranking support department is closed and the second-highest ranking support department is allocated to lower ranking support departments and the producing departments. This continues until all support department cost has been allocated to the producing departments. The sequential method takes X account of support department reciprocity. Reciprocity occurs when one support department uses the services of another support department. For example, Maintenance uses HR and HR may use the services of Maintenance. The sequential method does not take full account of reciprocity because lower ranking support department costs are x allocated to higher ranking support departments. Let's use Porter Company, as an example. Porter has two producing departments (Fabricating and Assembly) > and three support departments (Maintenance, Human Resources (HR) and General Factory (GF)). Porter provided the following information on the five departments: HR GF Maintenance $80,000 Fabricating Assembly $93,400 $56,700 Direct overhead cost $120,000 $260,000 5,000 Machine hours 1,000 3,000 12,000 3,000 30,000 Direct labor hours 4,000 5,000 8,000 10,000 Square footage 500 2,500 10,000 12,000 18,000 Porter uses the sequential method of support department cost allocation, and support departments are ranked in order of direct overhead cost (from high to low). Maintenance is allocated based on machine hours, Porter uses the sequential method of support department cost allocation, and support departments are ranked in order of direct overhead cost (from high to low). Maintenance is allocated based on machine hours, HR on direct labor hours, and GF on the basis of square footage. The Fabricating overhead rate is based on machine hours and the Assembly overhead rate is based on direct labor hours. Calculate the allocation ratios to five significant digits and fill them into the following table (If an amount box does not require an entry, leave it blank or enter "0".): Maintenance Fabricating Assembly HR GF General X Factory Human Resources >aintenance Using the allocation ratios, fill in the following table to allocate support department costs to the producing departments. (Round all allocated amounts to the nearest dollar. Leave cells blank that do not require an entry) Maintenance HR GE Fabricating Assembly Direct $260,000 $120,000 overhead $80,000 $93,400 $56,700 cost Allocate: Maintenance HR GF Assembly Fabricating Direct overhead $80,000 $56,700 $120,000 $260,000 $93,400 cost Allocate: Maintenance X Human 111 Resources General Factory Sotal after llocation Notice that after allocation, zero dollars remain in the support departments and all overhead cost has been allocated to the producing departments. As a check on your work, add all direct overhead costs from the first line - it equals $610,100. Then add the totals after allocation - again, it equals $610,100. Finally, calculate the overhead rates (rounded to the nearest cent) for Fabricating and Assembly, Fabricating overhead rate s X per machine hour Assembly overhead rate X per direct labor hour --- Al