Answered step by step

Verified Expert Solution

Question

1 Approved Answer

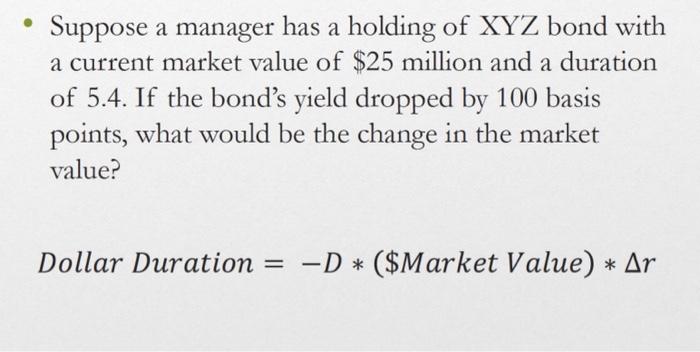

Suppose a manager has a holding of XYZ bond with a current market value of $25 million and a duration of 5.4. If the

Suppose a manager has a holding of XYZ bond with a current market value of $25 million and a duration of 5.4. If the bond's yield dropped by 100 basis points, what would be the change in the market value? Dollar Duration = = -D* ($Market Value) * Ar

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To calculate the change in the market value of the XYZ bond if the ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Vector Mechanics for Engineers Statics and Dynamics

Authors: Ferdinand Beer, E. Russell Johnston Jr., David Mazurek, Phillip Cornwell, Brian Self

11th edition

73398241, 978-0073398242