Answered step by step

Verified Expert Solution

Question

1 Approved Answer

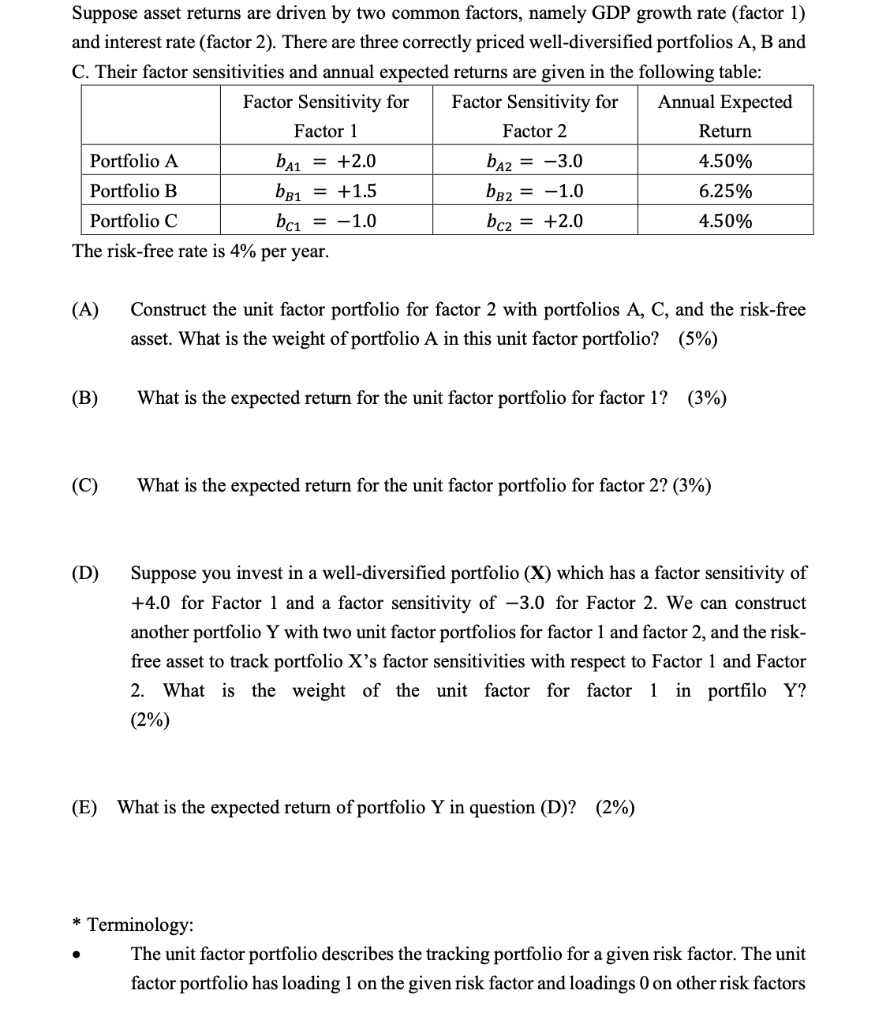

Suppose asset returns are driven by two common factors, namely GDP growth rate (factor 1) and interest rate (factor 2). There are three correctly priced

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance

Authors: Angelico Groppelli, Ehsan Nikbakht

7th Edition

1438010362, 9781438010366