Answered step by step

Verified Expert Solution

Question

1 Approved Answer

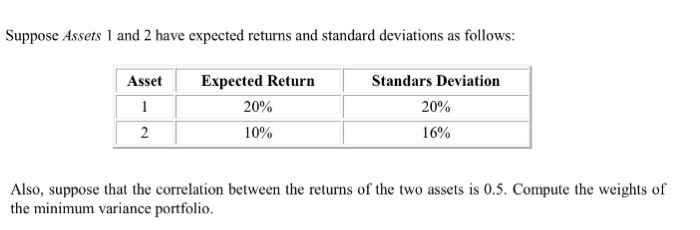

Suppose Assets 1 and 2 have expected returns and standard deviations as follows: Expected Return 20% 10% Standars Deviation 20% 16% Asset Also, suppose that

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Sustainability Proceedings From The Finance And Sustainability Conference Wroclaw 2017

Authors: Agnieszka Bem, Karolina Daszy?ska-?ygad?o , Ta?ána Hajdíková, Péter Juhász

1st Edition