Question

Suppose equity returns can be explained by Fama-French's three-factor model The risk premiums for the three factors are 5.5%, 4.9%, and 4.2%, respectively. If you

Suppose equity returns can be explained by Fama-French's three-factor model

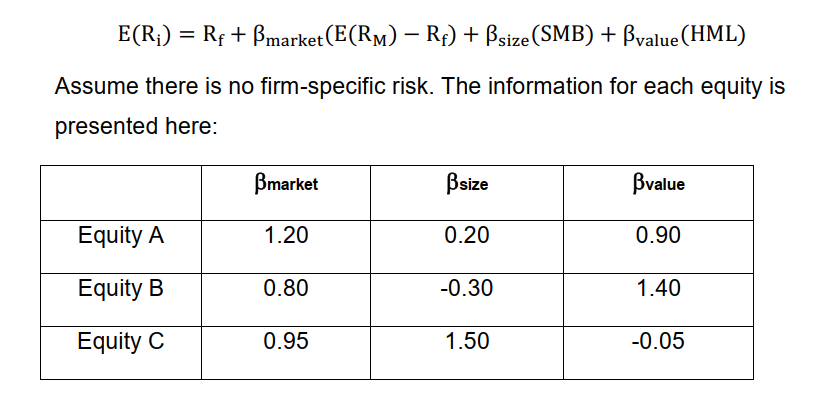

The risk premiums for the three factors are 5.5%, 4.9%, and 4.2%, respectively. If you create a portfolio with 20% invested in A, 20% invested in B, and the remainder in C, what is the expected return of your portfolio? Assume that the risk-free rate is 5%. Show your calculation steps clearly.

E(R;) = Rp + Bmarket (E(RM) Rp) + Bsize(SMB) + Bvalue (HML) = Assume there is no firm-specific risk. The information for each equity is presented here: Bmarket Bsize Bvalue Equity A 1.20 0.20 0.90 Equity B 0.80 -0.30 1.40 Equity C 0.95 1.50 -0.05Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Financial Literacy

Authors: Joan S. Ryan , Christie Ryan

3rd Edition

1337412686,1305980697