Answered step by step

Verified Expert Solution

Question

1 Approved Answer

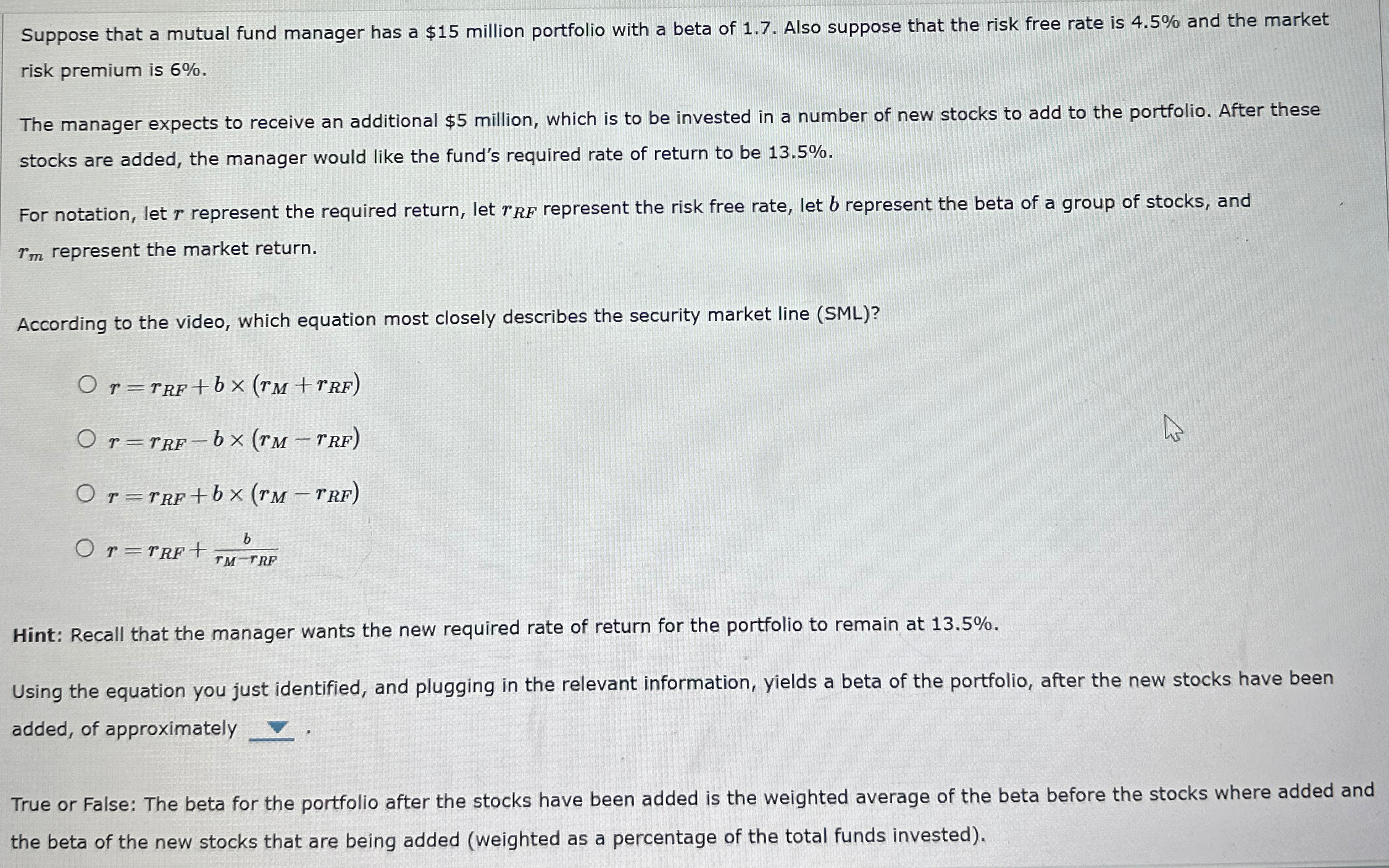

Suppose that a mutual fund manager has a $ 1 5 million portfolio with a beta of 1 . 7 . Also suppose that the

Suppose that a mutual fund manager has a $ million portfolio with a beta of Also suppose that the risk free rate is and the market risk premium is

The manager expects to receive an additional $ million, which is to be invested in a number of new stocks to add to the portfolio. After these stocks are added, the manager would like the fund's required rate of return to be

For notation, let represent the required return, let represent the risk free rate, let represent the beta of a group of stocks, and represent the market return.

According to the video, which equation most closely describes the security market line SML

Hint: Recall that the manager wants the new required rate of return for the portfolio to remain at

Using the equation you just identified, and plugging in the relevant information, yields a beta of the portfolio, after the new stocks have been added, of approximately

True or False: The beta for the portfolio after the stocks have been added is the weighted average of the beta before the stocks where added and the beta of the new stocks that are being added weighted as a percentage of

the total funds investedThe beta of the portfolio after the stocks have been added which you just calculated along with the new total amount of funds invested, implies that the beta of the stocks added to the portfolio must be:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Reporting And Statement Analysis A Strategic Approach

Authors: Clyde P. Stickney, Paul Brown, James M. Wahlen

5th Edition

032418638X, 978-0324186383