Answered step by step

Verified Expert Solution

Question

1 Approved Answer

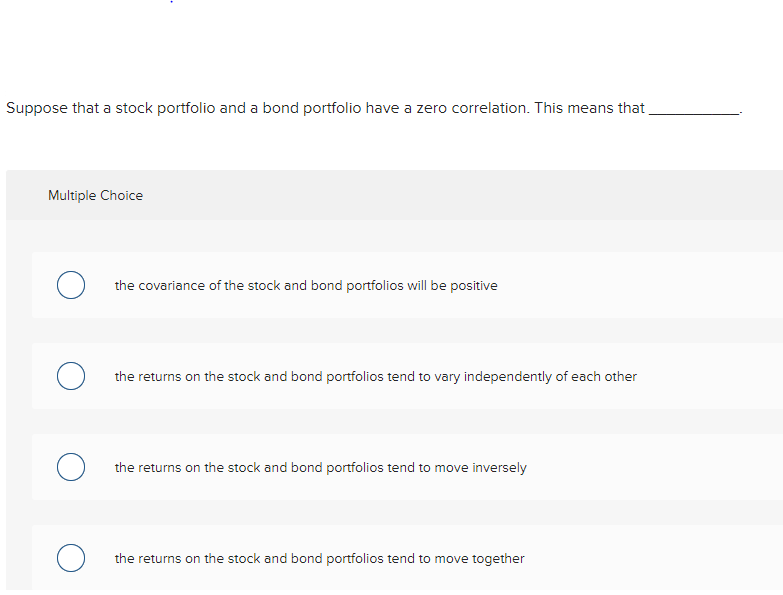

Suppose that a stock portfolio and a bond portfolio have a zero correlation. This means that Multiple Choice the covariance of the stock and bond

Suppose that a stock portfolio and a bond portfolio have a zero correlation. This means that Multiple Choice the covariance of the stock and bond portfolios will be positive the returns on the stock and bond portfolios tend to vary independently of each other the returns on the stock and bond portfolios tend to move inversely the returns on the stock and bond portfolios tend to move together

Suppose that a stock portfolio and a bond portfolio have a zero correlation. This means that Multiple Choice the covariance of the stock and bond portfolios will be positive the returns on the stock and bond portfolios tend to vary independently of each other the returns on the stock and bond portfolios tend to move inversely the returns on the stock and bond portfolios tend to move together Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Unlock The Potential Of Forex An Essential Guide To Forex Trading

Authors: Enoch Grennan

1st Edition

979-8388679659