Question

Suppose that exactly 2 years ago you entered into a 10-year payer swap with a notional of $100,000,000 at a swap rate of 4.75%. The

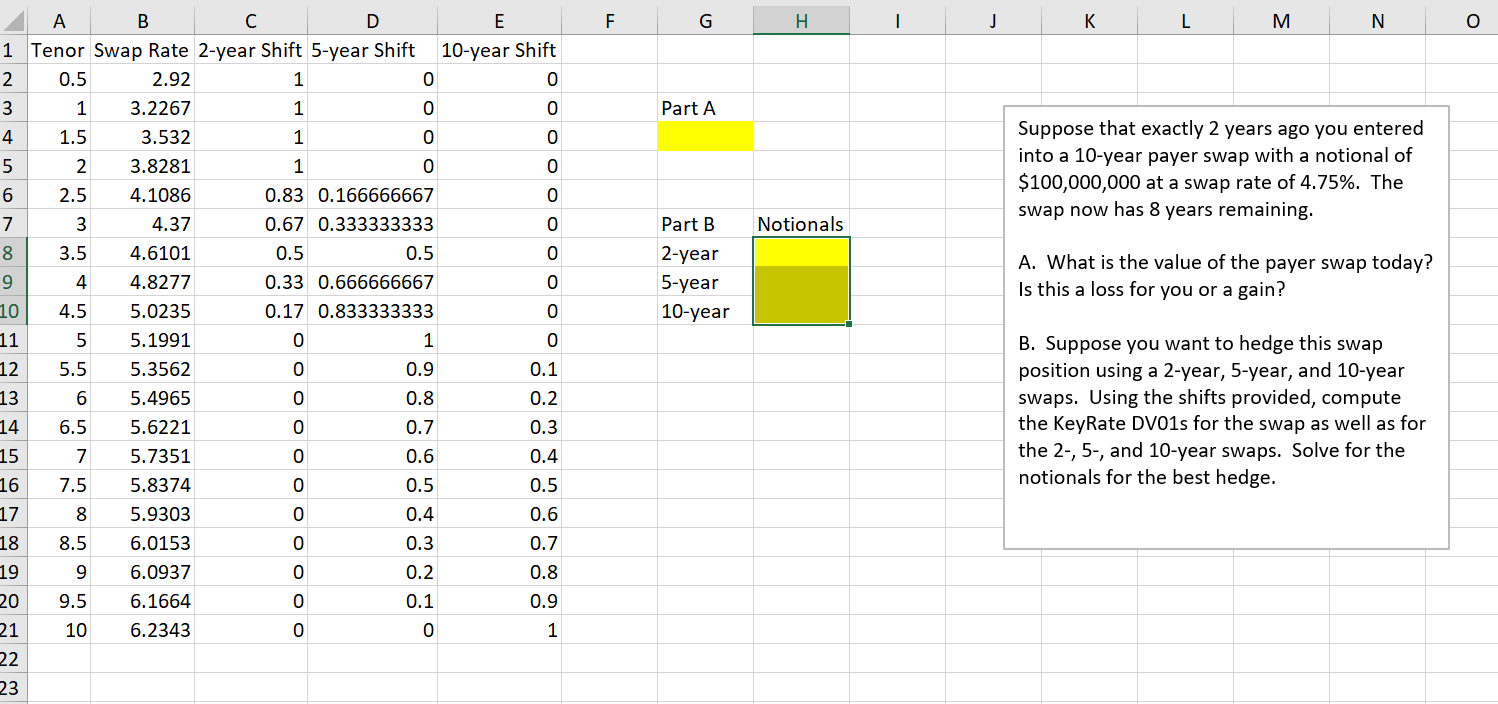

Suppose that exactly 2 years ago you entered into a 10-year payer swap with a notional of $100,000,000 at a swap rate of 4.75%. The swap now has 8 years remaining.

A. What is the value of the payer swap today? Is this a loss for you or a gain?

B. Suppose you want to hedge this swap position using a 2-year, 5-year, and 10-year swaps. Using the shifts provided, compute the KeyRate DV01s for the swap as well as for the 2-, 5-, and 10-year swaps. Solve for the notionals for the best hedge.

Please show the problem solving process, thank you

F H I J K L M N O 10-year Shift Part A Suppose that exactly 2 years ago you entered into a 10-year payer swap with a notional of $100,000,000 at a swap rate of 4.75%. The swap now has 8 years remaining. Notionals Part B 2-year 5-year 10-year A. What is the value of the payer swap today? Is this a loss for you or a gain? A B C D 1 Tenor Swap Rate 2-year Shift 5-year Shift 2 0.5 2.92 3 1 3.2267 4 1.5 3.532 2 3.8281 2.5 4.1086 0.83 0.166666667 3 4.37 0.67 0.333333333 3.5 4.6101 0.5 0.5 4 4.8277 0.33 0.666666667 4.5 5.0235 0.17 0.833333333 5 5.1991 12 5.5 5.3562 0 0.9 5.4965 0 6.5 5.6221 15 5.7351 0.6 7.5 5.8374 8 5.9303 18 8.5 6.0153 0.3 19 96.0937 0.2 20 9.5 6.1664 0.1 10 6.2343 0 o 13 0.8 B. Suppose you want to hedge this swap position using a 2-year, 5-year, and 10-year swaps. Using the shifts provided, compute the KeyRate DV01s for the swap as well as for the 2-,5-, and 10-year swaps. Solve for the notionals for the best hedge. 14 0.7 oooo 16 0.5 17 0.4 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1 21 23 F H I J K L M N O 10-year Shift Part A Suppose that exactly 2 years ago you entered into a 10-year payer swap with a notional of $100,000,000 at a swap rate of 4.75%. The swap now has 8 years remaining. Notionals Part B 2-year 5-year 10-year A. What is the value of the payer swap today? Is this a loss for you or a gain? A B C D 1 Tenor Swap Rate 2-year Shift 5-year Shift 2 0.5 2.92 3 1 3.2267 4 1.5 3.532 2 3.8281 2.5 4.1086 0.83 0.166666667 3 4.37 0.67 0.333333333 3.5 4.6101 0.5 0.5 4 4.8277 0.33 0.666666667 4.5 5.0235 0.17 0.833333333 5 5.1991 12 5.5 5.3562 0 0.9 5.4965 0 6.5 5.6221 15 5.7351 0.6 7.5 5.8374 8 5.9303 18 8.5 6.0153 0.3 19 96.0937 0.2 20 9.5 6.1664 0.1 10 6.2343 0 o 13 0.8 B. Suppose you want to hedge this swap position using a 2-year, 5-year, and 10-year swaps. Using the shifts provided, compute the KeyRate DV01s for the swap as well as for the 2-,5-, and 10-year swaps. Solve for the notionals for the best hedge. 14 0.7 oooo 16 0.5 17 0.4 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1 21 23Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational Finance

Authors: Kirt Butler

2nd Edition

0324004508, 978-0324004502