Answered step by step

Verified Expert Solution

Question

1 Approved Answer

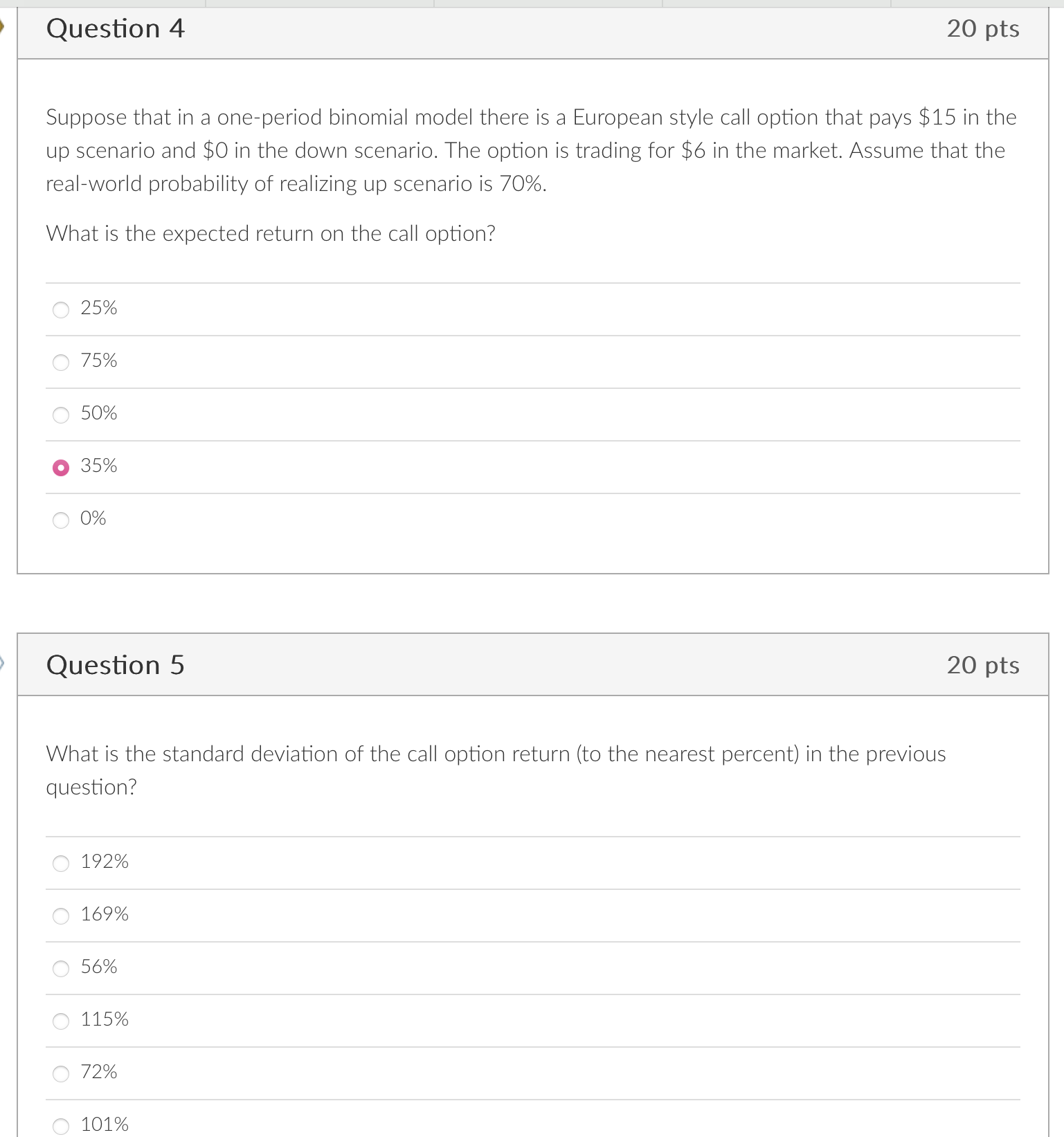

Suppose that in a one-period binomial model there is a European style call option that pays $15 in the up scenario and $0 in the

Suppose that in a one-period binomial model there is a European style call option that pays $15 in the up scenario and $0 in the down scenario. The option is trading for $6 in the market. Assume that the real-world probability of realizing up scenario is 70%. What is the expected return on the call option? \begin{tabular}{l} \hline 25% \\ \hline 75% \\ \hline 50% \\ \hline 35% \\ \hline 0% \end{tabular} Question 5 20 pts What is the standard deviation of the call option return (to the nearest percent) in the previous question? \begin{tabular}{l} \hline 192% \\ \hline 169% \\ \hline 56% \\ \hline 115% \\ \hline 72% \\ \hline 101% \end{tabular}

Suppose that in a one-period binomial model there is a European style call option that pays $15 in the up scenario and $0 in the down scenario. The option is trading for $6 in the market. Assume that the real-world probability of realizing up scenario is 70%. What is the expected return on the call option? \begin{tabular}{l} \hline 25% \\ \hline 75% \\ \hline 50% \\ \hline 35% \\ \hline 0% \end{tabular} Question 5 20 pts What is the standard deviation of the call option return (to the nearest percent) in the previous question? \begin{tabular}{l} \hline 192% \\ \hline 169% \\ \hline 56% \\ \hline 115% \\ \hline 72% \\ \hline 101% \end{tabular} Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Multinational Finance

Authors: Michael H. Moffett, Arthur I. Stonehill, David K. Eiteman

4th Edition

9780132138079