Question

Suppose that the assets of a bank consist of 200 million euros of 1-year loans to BB-rated corporations. The PD is 2% and the LGD

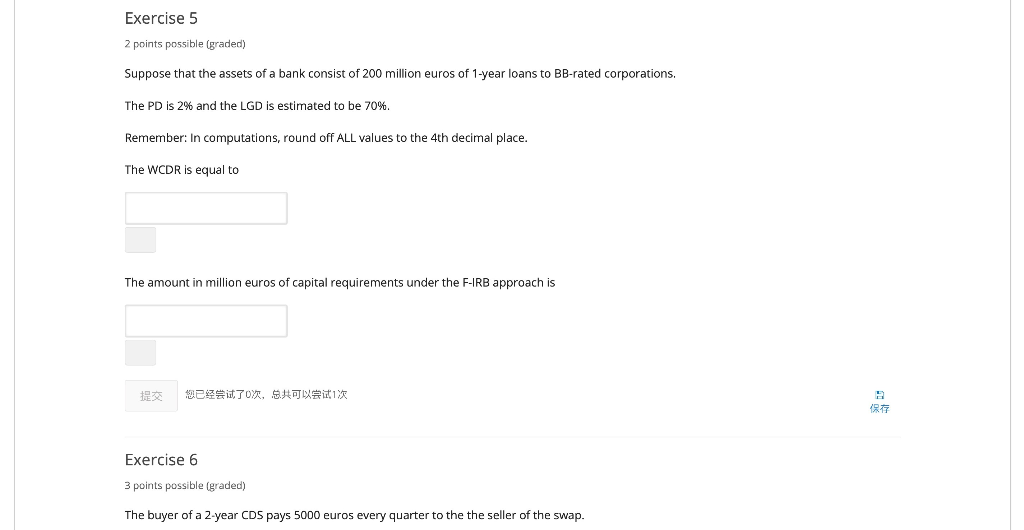

Suppose that the assets of a bank consist of 200 million euros of 1-year loans to BB-rated corporations.

The PD is 2% and the LGD is estimated to be 70%.

Remember: In computations, round off all valurs to the 4th decimal place.

The WCDR is equal to :

The amount in million euros of capital requirements under the F-IRB approach is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Accounting A Practical Approach Chapters 1-25

Authors: Jeffrey Slater

12th Edition

013277206X, 978-0132772068