Question

Suppose that the change in a portfolio value for a one-basis-point shift in the 1-, 2-, 3-, 4-, 5-, 7-, 10-, and 30-year rates are

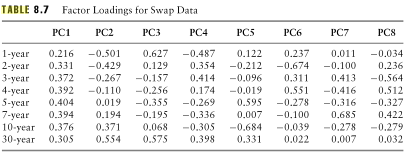

Suppose that the change in a portfolio value for a one-basis-point shift in the 1-, 2-, 3-, 4-, 5-, 7-, 10-, and 30-year rates are (in $ million) +5, -3, -1, +2, +5, +7, +8, and +1, respectively. Estimate the delta of the portfolio with respect to the first three factors in Table 8.7 (below).

Quantify the relative importance of the three factors for this portfolio.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Total Inventors Manual

Authors: Sean Michael Ragan

1st Edition

1681881586, 978-1681881584