Answered step by step

Verified Expert Solution

Question

1 Approved Answer

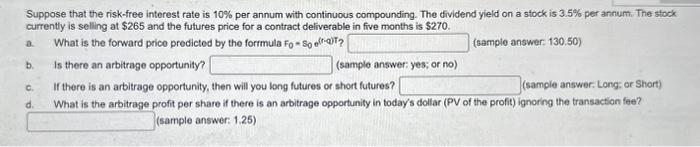

Suppose that the risk-free interest rate is 10% per annum with continuous compounding. The dividend yield on a stock is 3.5% per annum. The

Suppose that the risk-free interest rate is 10% per annum with continuous compounding. The dividend yield on a stock is 3.5% per annum. The stock currently is selling at $265 and the futures price for a contract deliverable in five months is $270. What is the forward price predicted by the formula Fo=Soff-? (sample answer: 130.50) Is there an arbitrage opportunity? If there is an arbitrage opportunity, then will you long futures or short futures? (sample answer: Long; or Short) What is the arbitrage profit per share if there is an arbitrage opportunity in today's dollar (PV of the profit) ignoring the transaction fee? 1.25) (sample answer: 1.3 8. b. C. d. (sample answer: yes; or no)

Step by Step Solution

★★★★★

3.38 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the forward price using the formula FoSolhat we can use the following equation F S er q ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Corporate Finance

Authors: Richard A. Brealey, Stewart C. Myers

7th edition

72869461, 72467665, 9780072467666, 978-0072869460