Answered step by step

Verified Expert Solution

Question

1 Approved Answer

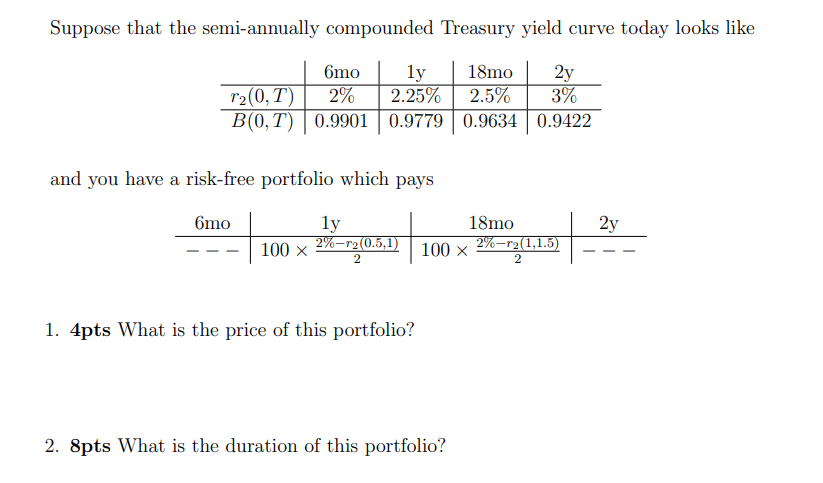

Suppose that the semi-annually compounded Treasury yield curve today looks like 6mo 1y 2% 18mo 2y 3% 2.25% 2.5% r(0, T) B(0,T) 0.9901 0.9779

Suppose that the semi-annually compounded Treasury yield curve today looks like 6mo 1y 2% 18mo 2y 3% 2.25% 2.5% r(0, T) B(0,T) 0.9901 0.9779 0.9634 0.9422 and you have a risk-free portfolio which pays 6mo ly 100 2%-r2(0.5,1) 1. 4pts What is the price of this portfolio? 100 2. 8pts What is the duration of this portfolio? 18mo 2%-r2(1,1.5) 2 2y

Step by Step Solution

There are 3 Steps involved in it

Step: 1

1 To price the portfolio 6mo bond pays 2 at t05 so present ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

MIS Essentials

Authors: David M. Kroenke

4th edition

978-0133546590, 133546594, 978-0133807479