Answered step by step

Verified Expert Solution

Question

1 Approved Answer

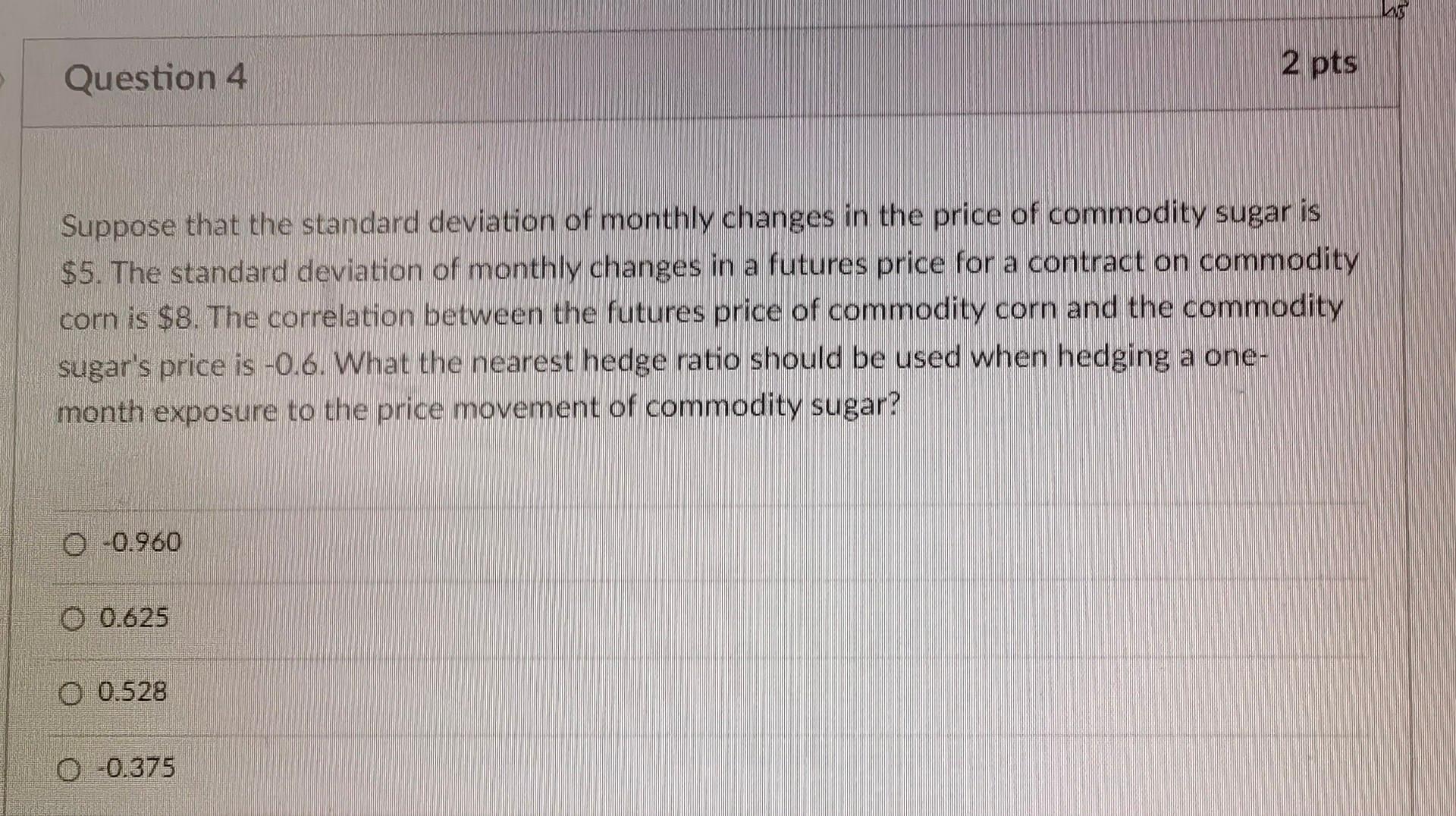

Suppose that the standard deviation of monthly changes in the price of commodity sugar is $5. The standard deviation of monthly changes in a futures

Suppose that the standard deviation of monthly changes in the price of commodity sugar is $5. The standard deviation of monthly changes in a futures price for a contract on commodity corn is $8. The correlation between the futures price of commodity corn and the commodity sugar's price is 0.6. What the nearest hedge ratio should be used when hedging a onemonth exposure to the price movement of commodity sugar? 0.960 0.625 0.528 0.375

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Environmental Finance And Investments

Authors: Marc Chesney, Jonathan Gheyssens, Anca Claudia Pana, Luca Taschini

2nd Edition

366248174X, 978-3662481745