Answered step by step

Verified Expert Solution

Question

1 Approved Answer

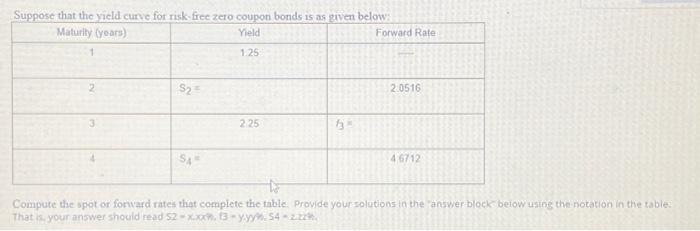

Suppose that the yield curve for risk-free zero coupon bonds is as given below: Maturity (years) Yield 1.25 2 3 S2= S4= 2.25 f3 =

Suppose that the yield curve for risk-free zero coupon bonds is as given below: Maturity (years) Yield 1.25 2 3 S2= S4= 2.25 f3 = Forward Rate 2.0516 4.6712 Compute the spot or forward rates that complete the table. Provide your solutions in the "answer block" below using the notation in the table. That is, your answer should read S2 = x.xx%, f3 = y.yy96, S4= Z.ZZ%.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Household Finance Adrift In A Sea Of Red Ink Palgrave Macmillan Studies In Banking And Financial Institutions

Authors: D. Chorafas

1st Edition

1137299444, 1137299452, 9781137299451