Answered step by step

Verified Expert Solution

Question

1 Approved Answer

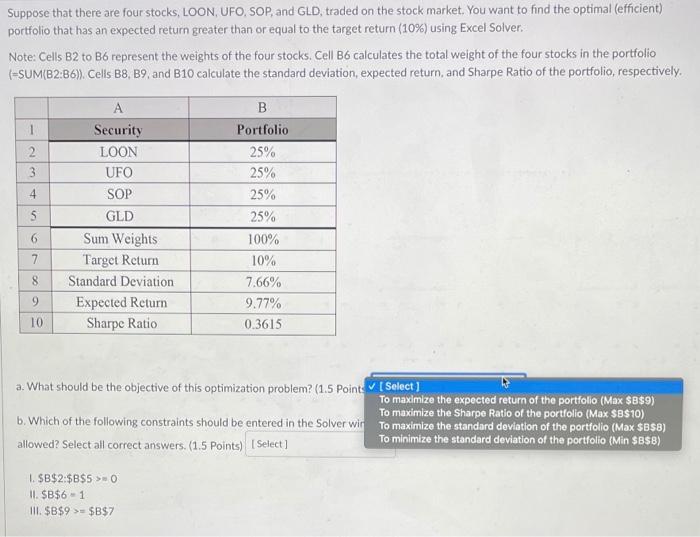

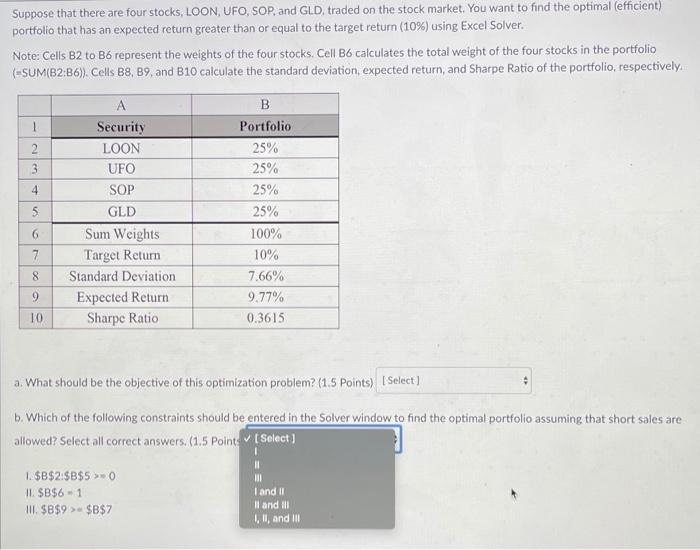

Suppose that there are four stocks, LOON, UFO, SOP, and GLD, traded on the stock market. You want to find the optimal (efficient) portfolio that

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptoassets The Innovative Investors Guide To Bitcoin And Beyond

Authors: Chris Burniske ,Jack Tatar

1st Edition

1260026671, 126002668X, 9781260026672, 9781260026689