Answered step by step

Verified Expert Solution

Question

1 Approved Answer

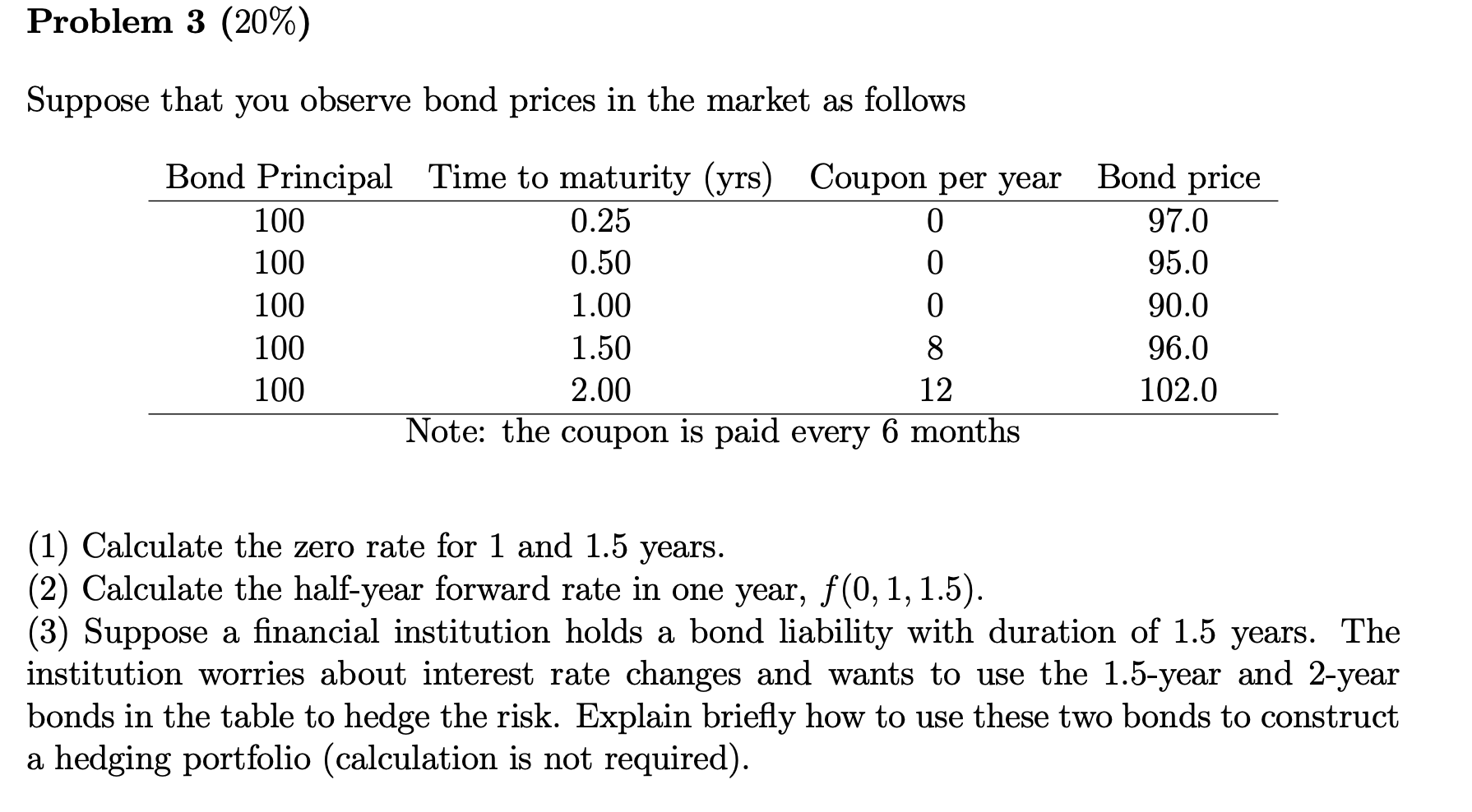

Suppose that you observe bond prices in the market as follows Note: the coupon is pald every 6 months (1) Calculate the zero rate for

Suppose that you observe bond prices in the market as follows Note: the coupon is pald every 6 months (1) Calculate the zero rate for 1 and 1.5 years. (2) Calculate the half-year forward rate in one year, f(0,1,1.5). (3) Suppose a financial institution holds a bond liability with duration of 1.5 years. The institution worries about interest rate changes and wants to use the 1.5-year and 2-year bonds in the table to hedge the risk. Explain briefly how to use these two bonds to construct a hedging portfolio (calculation is not required)

Suppose that you observe bond prices in the market as follows Note: the coupon is pald every 6 months (1) Calculate the zero rate for 1 and 1.5 years. (2) Calculate the half-year forward rate in one year, f(0,1,1.5). (3) Suppose a financial institution holds a bond liability with duration of 1.5 years. The institution worries about interest rate changes and wants to use the 1.5-year and 2-year bonds in the table to hedge the risk. Explain briefly how to use these two bonds to construct a hedging portfolio (calculation is not required) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Truth About Buying Annuities Annuities Can Make Or Break Your Retirement

Authors: Steve Weisman

1st Edition

0132353083,0132701162