Answered step by step

Verified Expert Solution

Question

1 Approved Answer

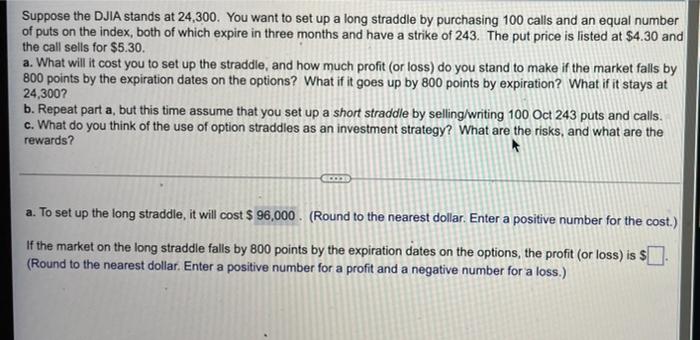

Suppose the DJIA stands at 24,300. You want to set up a long straddle by purchasing 100 calls and an equal number of puts on

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Theory Of Interest

Authors: Friedrich A. Lutz

2nd Edition

1138539074,1351472836