Answered step by step

Verified Expert Solution

Question

1 Approved Answer

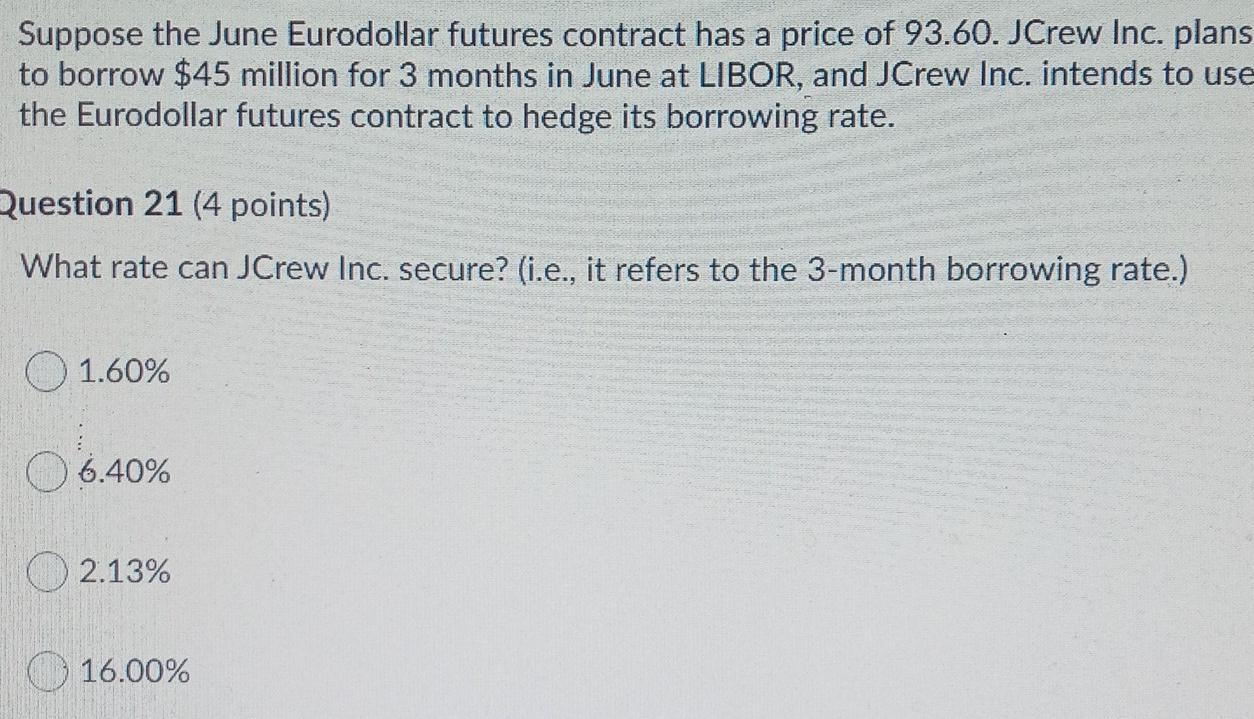

Suppose the June Eurodollar futures contract has a price of 93.60. JCrew Inc. plans to borrow $45 million for 3 months in June at LIBOR,

Suppose the June Eurodollar futures contract has a price of 93.60. JCrew Inc. plans to borrow $45 million for 3 months in June at LIBOR, and JCrew Inc. intends to use the Eurodollar futures contract to hedge its borrowing rate. Question 21 (4 points) What rate can JCrew Inc. secure? (i.e., it refers to the 3-month borrowing rate.) 1.60% 06.40% 2.13% 16.00%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Banking Reforms And Monetary Policy In The Peoples Republic Of China

Authors: Yong Guo

1st Edition

1403900787,1403914540