Answered step by step

Verified Expert Solution

Question

1 Approved Answer

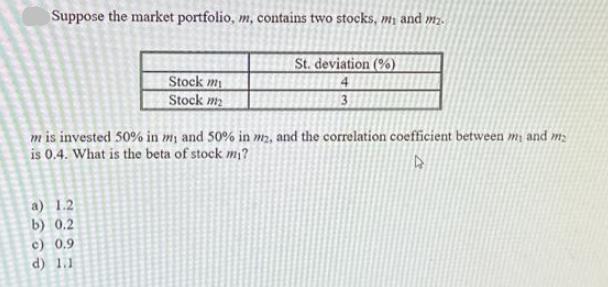

Suppose the market portfolio, m, contains two stocks, my and m. St. deviation (%) 4 3 Stock my Stock m m is invested 50%

Suppose the market portfolio, m, contains two stocks, my and m. St. deviation (%) 4 3 Stock my Stock m m is invested 50% in m and 50% in m, and the correlation coefficient between my and m is 0.4. What is the beta of stock mi? A a) 1.2 b) 0.2 c) 0,9 d) 1.1

Step by Step Solution

★★★★★

3.31 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

The detailed answer for the above question is provided below The answer is b To calculate the beta o...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham

Concise 9th Edition

1305635937, 1305635930, 978-1305635937