Answered step by step

Verified Expert Solution

Question

1 Approved Answer

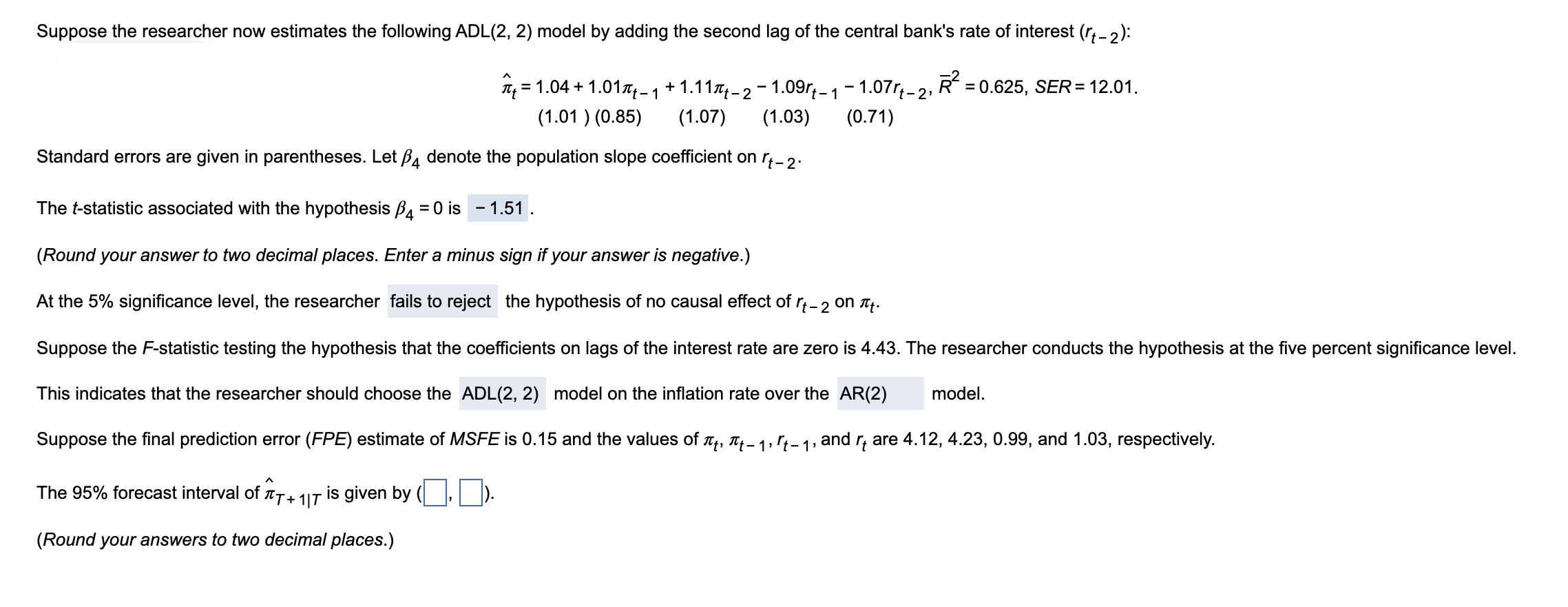

Suppose the researcher now estimates the following ADL(2, 2) model by adding the second lag of the central bank's rate of interest (rt-2): 1.11-2-1.09-1-1.07rt-2,

Suppose the researcher now estimates the following ADL(2, 2) model by adding the second lag of the central bank's rate of interest (rt-2): 1.11-2-1.09-1-1.07rt-2, R = 0.625, SER= 12.01. (1.07) (1.03) (0.71) 1.04 +1.01-1 + (1.01) (0.85) Standard errors are given in parentheses. Let 4 denote the population slope coefficient on rt-2. = The t-statistic associated with the hypothesis B4 = 0 is (Round your answer to two decimal places. Enter a minus sign if your answer is negative.) At the 5% significance level, the researcher fails to reject the hypothesis of no causal effect of rt-2 on it. Suppose the F-statistic testing the hypothesis that the coefficients on lags of the interest rate are zero is 4.43. The researcher conducts the hypothesis at the five percent significance level. This indicates that the researcher should choose the ADL(2, 2) model on the inflation rate over the AR(2) Suppose the final prediction error (FPE) estimate of MSFE is 0.15 and the values of ,-,-1, and rare 4.12, 4.23, 0.99, and 1.03, respectively. ^ The 95% forecast interval of T+117 is given by (Round your answers to two decimal places.) - 1.51. model.

Step by Step Solution

★★★★★

3.34 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Microeconomics An Intuitive Approach with Calculus

Authors: Thomas Nechyba

1st edition

538453257, 978-0538453257