Question

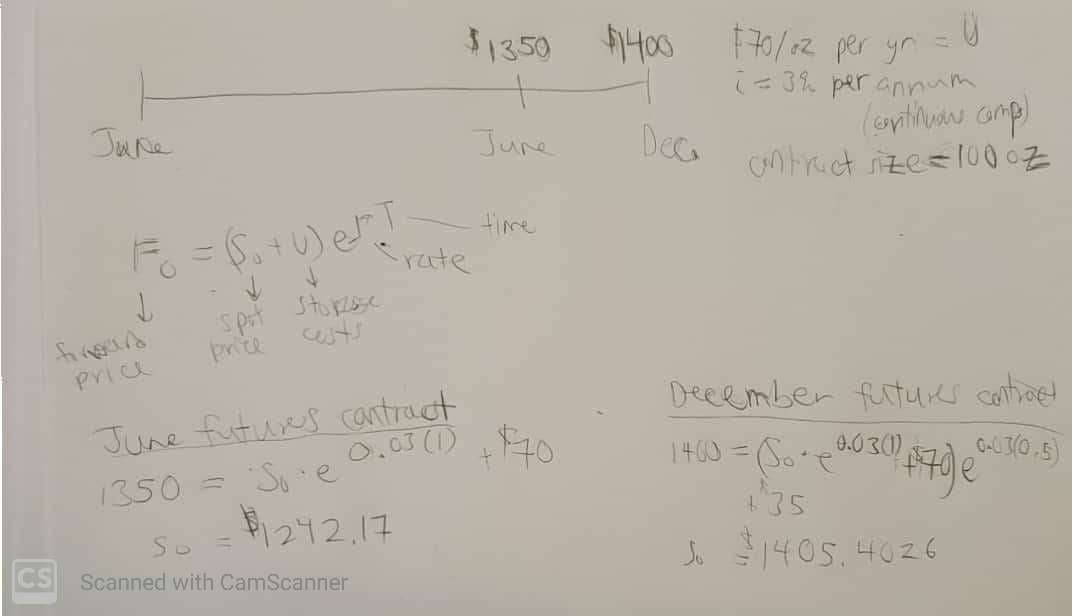

Suppose the storage cost for gold is $70 per ounce per year and the interest rate for borrowing or lending is 3% per annum, compounded

Suppose the storage cost for gold is $70 per ounce per year and the interest rate for borrowing or lending is 3% per annum, compounded continuously. Storage costs are assessed when you take delivery of the gold, but you can pay them at a later date with accumulated interest.

1. Show how you could make an arbitrage profit if the June and December futures contracts for a particular year trade at $1,350 and $1,400 per ounce, respectively.

2. Show how the arbitrage works assuming a contract size of 100 ounces. Ignore daily settlement (marking to market) in answering this question.

3. What storage cost would eliminate this arbitrage opportunity?

This is the only information that I received. Here is the work I have so far.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Trading QuickStart Guide The Simplified Beginners Guide To Options Trading

Authors: Clydebank Finance

2nd Edition

1945051051, 978-1945051050