Answered step by step

Verified Expert Solution

Question

1 Approved Answer

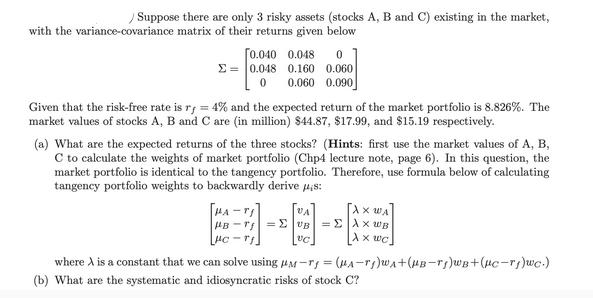

Suppose there are only 3 risky assets (stocks A, B and C) existing in the market, with the variance-covariance matrix of their returns given

Suppose there are only 3 risky assets (stocks A, B and C) existing in the market, with the variance-covariance matrix of their returns given below [0.040 0.048 0 =0.048 0.160 0.060 0 0.060 0.090 Given that the risk-free rate is ry = 4% and the expected return of the market portfolio is 8.826%. The market values of stocks A, B and C are (in million) $44.87, $17.99, and $15.19 respectively. (a) What are the expected returns of the three stocks? (Hints: first use the market values of A, B, C to calculate the weights of market portfolio (Chp4 lecture note, page 6). In this question, the market portfolio is identical to the tangency portfolio. Therefore, use formula below of calculating tangency portfolio weights to backwardly derive s: [HA-TI VA AXWA Ax wc HB TUB =AxwB HC " VC where A is a constant that we can solve using M-r=(A-T1)WA+(B-T)WB+(c-rj)wc.) (b) What are the systematic and idiosyncratic risks of stock C?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance

Authors: Harvey Rosen, Ted Gayer

10th edition

9781259716874, 78021685, 1259716872, 978-0078021688