Answered step by step

Verified Expert Solution

Question

1 Approved Answer

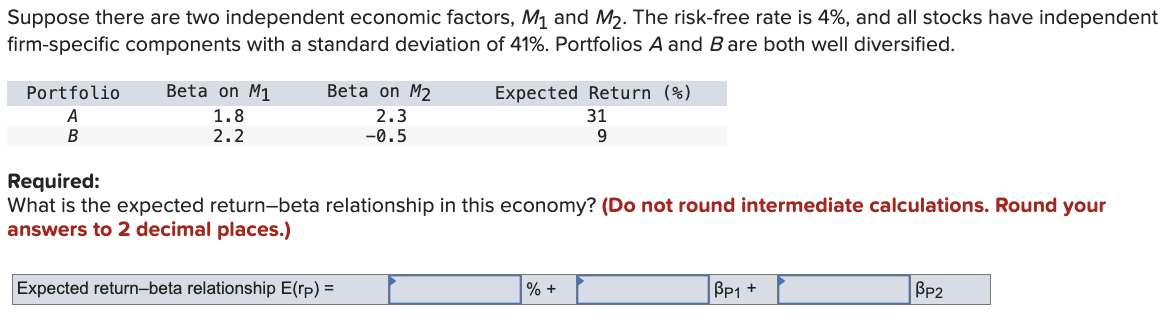

Suppose there are two independent economic factors, M 1 and M 2 . The risk - free rate is 4 % , and all stocks

Suppose there are two independent economic factors, and The riskfree rate is and all stocks have independent

firmspecific components with a standard deviation of Portfolios A and are both well diversified.

Required:

What is the expected returnbeta relationship in this economy? Do not round intermediate calculations. Round your

answers to decimal places.

Expected returnbeta relationship

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Issues In Finance

Authors: Simon Grima, Frank Bezzina, Inna Romanova

1st Edition

1786359073, 978-1786359070