Question

Suppose there is Portfolio D and E. Portfolio D invests 0.8 in security A and 0.2 in security B. Portfolio E invests 0.2 in security

Suppose there is Portfolio D and E.

Portfolio D invests 0.8 in security A and 0.2 in security B. Portfolio E invests 0.2 in security A and 0.8 in security B. Obtain the covariance and correlation between portfolios D and E.

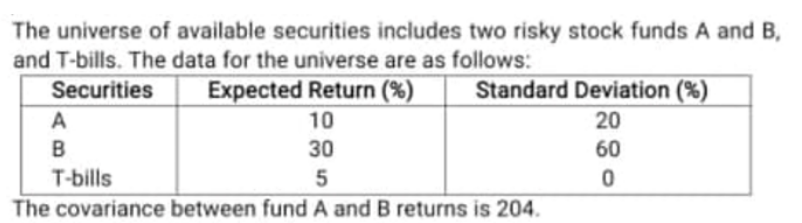

The universe of available securities includes two risky stock funds A and B, and T-bills. The data for the universe are as follows: Securities Expected Return (%) Standard Deviation (%) 10 20 B 30 60 T-bills 5 0 The covariance between fund A and B returns is 204Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptoassets The Innovative Investors Guide To Bitcoin And Beyond

Authors: Chris Burniske ,Jack Tatar

1st Edition

1260026671, 126002668X, 9781260026672, 9781260026689