Answered step by step

Verified Expert Solution

Question

1 Approved Answer

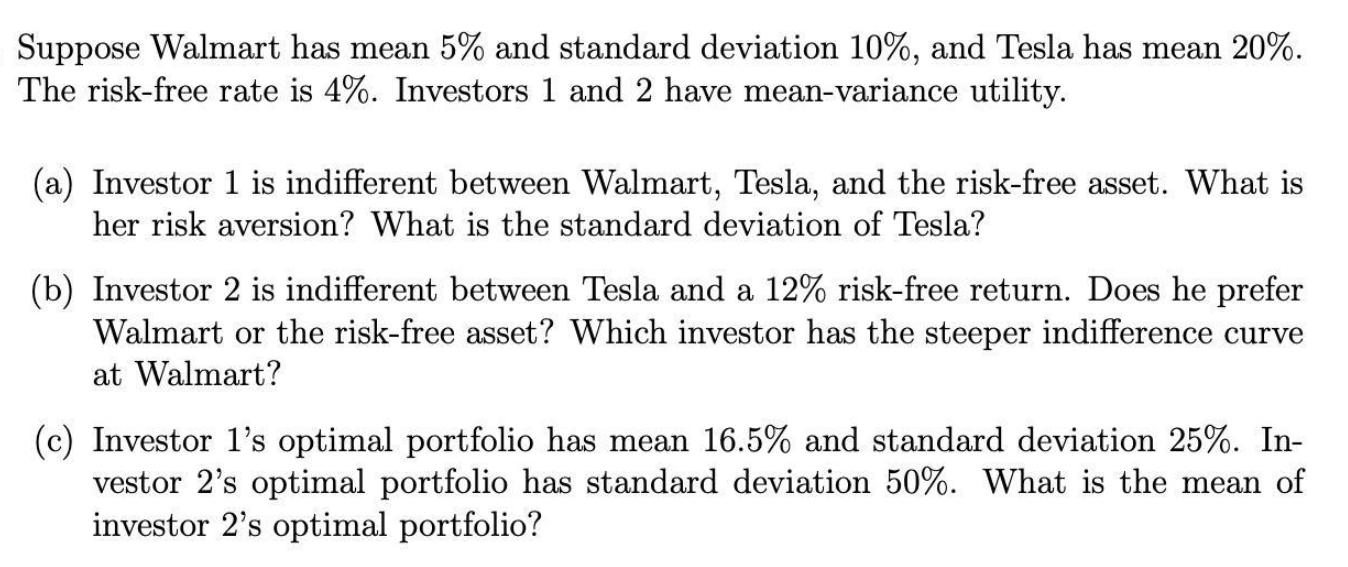

Suppose Walmart has mean 5% and standard deviation 10%, and Tesla has mean 20%. The risk-free rate is 4%. Investors 1 and 2 have

Suppose Walmart has mean 5% and standard deviation 10%, and Tesla has mean 20%. The risk-free rate is 4%. Investors 1 and 2 have mean-variance utility. (a) Investor 1 is indifferent between Walmart, Tesla, and the risk-free asset. What is her risk aversion? What is the standard deviation of Tesla? (b) Investor 2 is indifferent between Tesla and a 12% risk-free return. Does he prefer Walmart or the risk-free asset? Which investor has the steeper indifference curve at Walmart? (c) Investor 1's optimal portfolio has mean 16.5% and standard deviation 25%. In- vestor 2's optimal portfolio has standard deviation 50%. What is the mean of investor 2's optimal portfolio?

Step by Step Solution

★★★★★

3.42 Rating (158 Votes )

There are 3 Steps involved in it

Step: 1

SOLUTION a Investor 1s risk aversion can be calculated by the following formula Risk Aversion Mean S...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics For Engineers And Scientists

Authors: William Navidi

4th Edition

73401331, 978-0073401331