Question

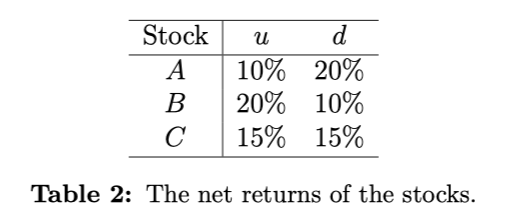

Suppose we are in a world with two equally likely states u and d. And suppose the net returns of the three stocks are given

Suppose we are in a world with two equally likely states u and d. And suppose the net returns of the three stocks are given by table 2.

(a) Let rA and rC be the net returns of stocks A and C respectively. Can you nd a random variable z such that rA = rC + z and E[z] = 0?

(b) Can you nd a risk-averse investor who prefers stock A (or B) to stock C?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments Analysis and Management

Authors: Charles P. Jones

12th edition

978-1118475904, 1118475909, 1118363299, 978-1118363294