Answered step by step

Verified Expert Solution

Question

1 Approved Answer

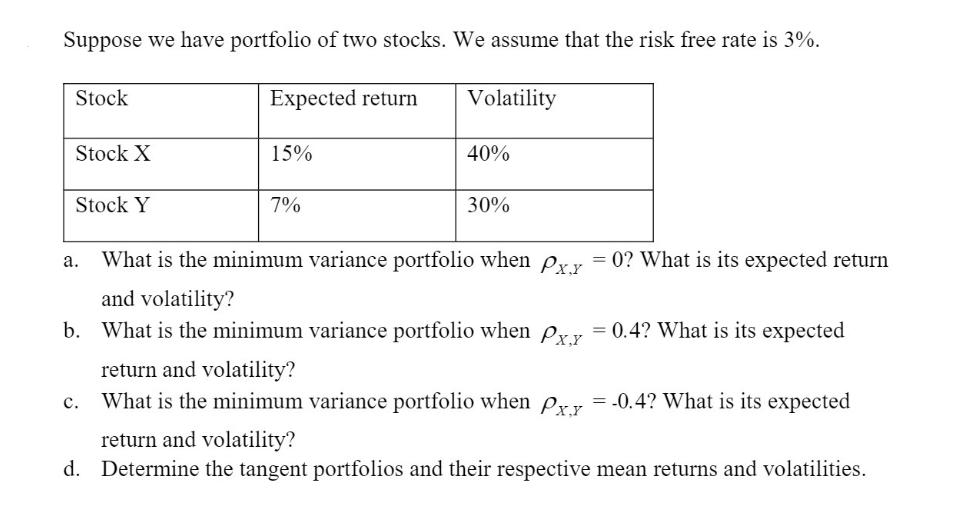

Suppose we have portfolio of two stocks. We assume that the risk free rate is 3%. Volatility Stock Stock X Stock Y a. Expected

Suppose we have portfolio of two stocks. We assume that the risk free rate is 3%. Volatility Stock Stock X Stock Y a. Expected return C. 15% 7% 40% What is the minimum variance portfolio when Px.x = 0? What is its expected return and volatility? b. What is the minimum variance portfolio when Px.x = 0.4? What is its expected return and volatility? What is the minimum variance portfolio when Px.x = -0.4? What is its expected return and volatility? d. Determine the tangent portfolios and their respective mean returns and volatilities. 30%

Step by Step Solution

★★★★★

3.41 Rating (164 Votes )

There are 3 Steps involved in it

Step: 1

To determine the minimum variance portfolio and the tangent portfolios we need to use portfolio theory and the concept of the efficient frontier The efficient frontier represents a set of portfolios t...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Reporting Financial Statement Analysis And Valuation A Strategic Perspective

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

9th Edition

1337614689, 1337614688, 9781337668262, 978-1337614689