Answered step by step

Verified Expert Solution

Question

1 Approved Answer

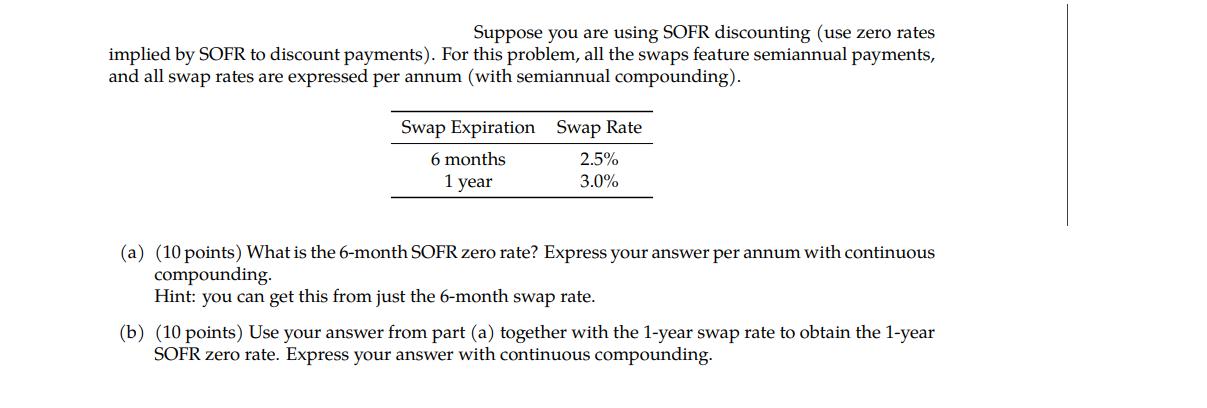

Suppose you are using SOFR discounting (use zero rates implied by SOFR to discount payments). For this problem, all the swaps feature semiannual payments,

Suppose you are using SOFR discounting (use zero rates implied by SOFR to discount payments). For this problem, all the swaps feature semiannual payments, and all swap rates are expressed per annum (with semiannual compounding). Swap Expiration Swap Rate 6 months 2.5% 1 year 3.0% (a) (10 points) What is the 6-month SOFR zero rate? Express your answer per annum with continuous compounding. Hint: you can get this from just the 6-month swap rate. (b) (10 points) Use your answer from part (a) together with the 1-year swap rate to obtain the 1-year SOFR zero rate. Express your answer with continuous compounding.

Step by Step Solution

★★★★★

3.31 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

To solve this problem we need to use the relationship between swap rates and zero rates Given inform...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Social Statistics For A Diverse Society

Authors: Chava Frankfort Nachmias, Anna Leon Guerrero

7th Edition

148333354X, 978-1506352060, 1506352065, 978-1483359687, 1483359689, 978-1483333540