Answered step by step

Verified Expert Solution

Question

1 Approved Answer

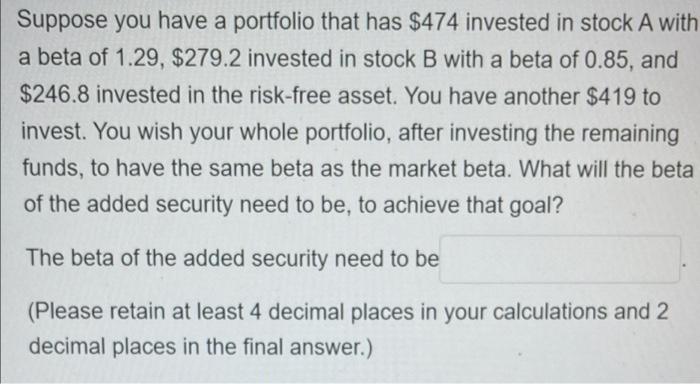

Suppose you have a portfolio that has $474 invested in stock A with a beta of 1.29, $279.2 invested in stock B with a beta

Suppose you have a portfolio that has $474 invested in stock A with a beta of 1.29, $279.2 invested in stock B with a beta of 0.85, and $246.8 invested in the risk-free asset. You have another $419 to invest. You wish your whole portfolio, after investing the remaining funds, to have the same beta as the market beta. What will the beta of the added security need to be, to achieve that goal? The beta of the added security need to be (Please retain at least 4 decimal places in your calculations and 2 decimal places in the final answer.)

Suppose you have a portfolio that has $474 invested in stock A with a beta of 1.29, $279.2 invested in stock B with a beta of 0.85, and $246.8 invested in the risk-free asset. You have another $419 to invest. You wish your whole portfolio, after investing the remaining funds, to have the same beta as the market beta. What will the beta of the added security need to be, to achieve that goal? The beta of the added security need to be (Please retain at least 4 decimal places in your calculations and 2 decimal places in the final answer.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Trade Union Finance

Authors: Marick F. Masters, Raymond Gibney

1st Edition

1032371382, 978-1032371382