Answered step by step

Verified Expert Solution

Question

1 Approved Answer

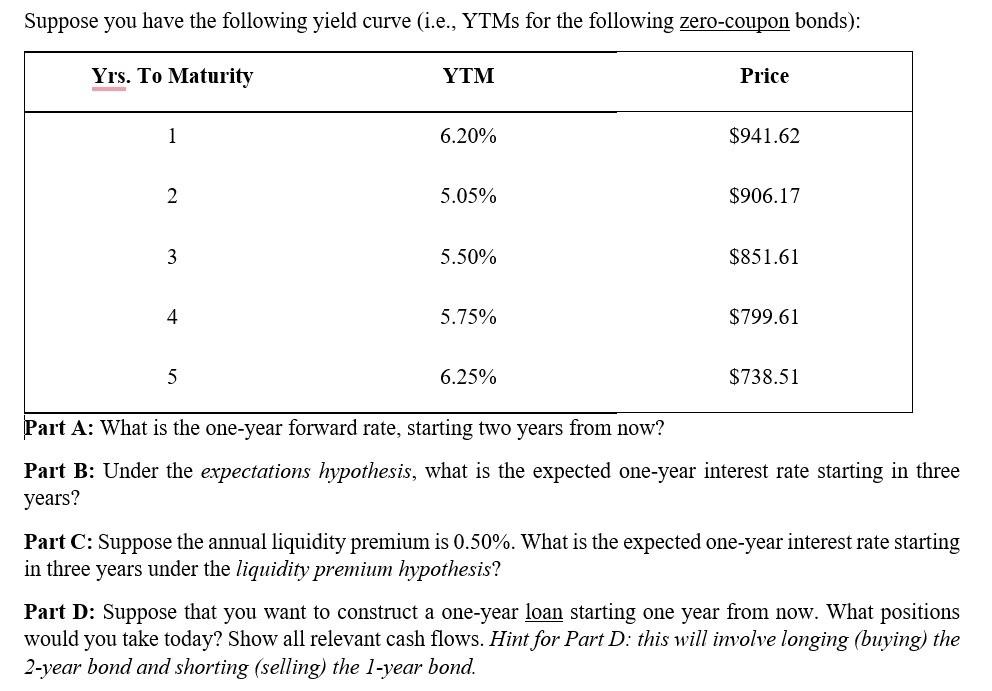

Suppose you have the following yield curve (i.e., YTMs for the following zero-coupon bonds): Part B: Under the expectations hypothesis, what is the expected one-year

Suppose you have the following yield curve (i.e., YTMs for the following zero-coupon bonds): Part B: Under the expectations hypothesis, what is the expected one-year interest rate starting in three years? Part C: Suppose the annual liquidity premium is 0.50%. What is the expected one-year interest rate starting in three years under the liquidity premium hypothesis? Part D: Suppose that you want to construct a one-year loan starting one year from now. What positions would you take today? Show all relevant cash flows. Hint for Part D: this will involve longing (buying) the 2-year bond and shorting (selling) the 1-year bond. Suppose you have the following yield curve (i.e., YTMs for the following zero-coupon bonds): Part B: Under the expectations hypothesis, what is the expected one-year interest rate starting in three years? Part C: Suppose the annual liquidity premium is 0.50%. What is the expected one-year interest rate starting in three years under the liquidity premium hypothesis? Part D: Suppose that you want to construct a one-year loan starting one year from now. What positions would you take today? Show all relevant cash flows. Hint for Part D: this will involve longing (buying) the 2-year bond and shorting (selling) the 1-year bond

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The New Reality Of Wall Street An Investors Survival Guide To Triple Waterfalls And Other Stock Market Perils

Authors: Donald Coxe

1st Edition

0071417532